The virus can’t be bluffed or bullied and will soon become his greatest adversary.

The coronavirus pandemic is the greatest challenge Donald Trump has ever faced. As stock markets fall and patient numbers rise, the epidemic threatens the lives of some Americans and the prosperity of all—and it has already begun to disrupt the political methods that brought Mr. Trump to the White House.

As he has done in other crises, the president is stalling for time as he processes the nature of the threat and tests rhetorical and policy responses to it. But unlike human political adversaries, the coronavirus isn’t something he can bluff, threaten or placate. If the epidemic follows the course medical experts believe to be largely inevitable, both the disease and its economic consequences will be immune to Mr. Trump’s standard tactics. He can’t

spin them away,

divert public attention by creating another drama, or

blame them on President Obama.

In the near future the mass rallies that have been critical to Mr. Trump’s political success may be banned on public-health grounds. If he is especially unlucky, one of his rallies could be implicated in a major outbreak.

Many of the key points in Mr. Trump’s case for re-election are also at risk. A recession would deprive him of the argument that, whatever you think of his character, he puts money in your pocket. A pandemic also undercuts his contention that a “wrecking ball” presidency is needed to destroy a rotten establishment. That reasoning works better when it comes to university administrators overreaching on Title IX and ultraliberal journalists than with the medical establishment and public-health professionals. Voters tend to like stability in a crisis.

Meanwhile, the media multitudes who loathe Mr. Trump will do everything they can to turn the epidemic into a Hurricane Katrina event. That would be easy to do even if the government’s response is near-flawless; epidemics are messy. There will almost certainly be heartbreaking tragedies that can plausibly be blamed on administration policies. There will be shortages of medical supplies. Some hospitals will be stretched past the breaking point. The bureaucracy and its leadership will inevitably fall short in many ways. In an election year when health care is a major political issue, every failure and problem in the coronavirus response will be politicized and publicized, putting the administration on the defensive as the economy falters and the virus spreads.

The administration’s response, one may confidently assume, won’t be flawless. This isn’t only because the epidemic is a challenge that would test any president. Mr. Trump’s improvisational and chaotic approach to governance, rooted in his reliance on intuition and impulse as well as his use of conflict as a management method, will combine with the deep lack of trust between political and career officials across the government to produce highly public missteps and policy errors. Critics will have an abundance of ammunition.

The president’s basic political method is theatrical. Many Americans have come to believe that what happens in Washington is mostly fake news, more like professional wrestling than a serious ideological and political struggle with major consequences for their lives. Mr. Trump, from the vantage point of a long career in casinos and reality television, understands this better than his rivals. He approaches politics as entertainment and has repeatedly foiled opponents by turning potentially disastrous developments—impeachment, for example—into thrilling new episodes of “The Trump Show.” But a pandemic will affect voters more than scandals and pratfalls in the faraway capital. If a recession comes as well, will voters lose patience with Mr. Trump’s sizzle and spin?

None of this means that the coronavirus will necessarily succeed where Russiagate failed in bringing the Trump Show to an inglorious end. The president is an extraordinary political talent and has some advantages that shouldn’t be discounted. Unconstrained as he is by worries about debt and deficits, he can propose massive relief packages. The incompetence of China’s early responses to the disease gives Mr. Trump a convenient scapegoat and will reinforce public doubts about globalization. The shortcomings of national health systems in Italy, France, Britain and elsewhere will at least partly blunt attempts to blame a U.S. epidemic on the absence of such a system here. The impact of the disease on Iran, China and North Korea could help Mr. Trump score foreign-policy wins.

And then there are his critics. Their loathing of the 45th president is so intense that their rhetoric can turn voters off. Mr. Trump is a master at exploiting these sorts of missteps, and he will be looking for targets of opportunity.

Despite all that, the coronavirus, if it continues on its present course, will soon become the most powerful adversary the Trump administration has yet faced. Mr. Trump’s other opponents, from Nancy Pelosi and Chuck Schumer to the Iranian mullahs and Kim Jong Un, have nothing on a disease that can threaten the lives of Americans and bring the economy to a grinding halt.

Policymakers and too many economic commentators fail to grasp how the next global recession may be unlike the last two. In contrast to recessions driven mainly by a demand shortfall, the challenge posed by a supply-side-driven downturn is that it can result in sharp drops in production, generalized shortages, and rapidly rising prices.

CAMBRIDGE – It is too soon to predict the long-run arc of the coronavirus outbreak. But it is not too soon to recognize that the next global recession could be around the corner – and that it may look a lot different from those that began in 2001 and 2008.

For starters, the next recession is likely to emanate from China, and indeed may already be underway. China is a highly leveraged economy, it cannot afford a sustained pause today anymore than fast-growing 1980s Japan could. People, businesses, and municipalities need funds to pay back their out-size debts. Sharply adverse demographics, narrowing scope for technological catch-up, and a huge glut of housing from recurrent stimulus programs – not to mention an increasingly centralized decision-making process – already presage significantly slower growth for China in the next decade.

Moreover, unlike the two previous global recessions this century, the new coronavirus, COVID-19, implies a supply shock as well as a demand shock. Indeed, one has to go back to the oil-supply shocks of the mid-1970s to find one as large. Yes, fear of contagion will hit demand for airlines and global tourism, and precautionary savings will rise. But when tens of millions of people can’t go to work (either because of a lockdown or out of fear), global value chains break down, borders are blocked, and world trade shrinks because countries distrust of one another’s health statistics, the supply side suffers at least as much.

Affected countries will, and should, engage in massive deficit spending to shore up their health systems and prop up their economies. The point of saving for a rainy day is to spend when it rains, and preparing for pandemics, wars, climate crises, and other out-of-the-box events is precisely why open-ended deficit spending during booms is dangerous.

But policymakers and altogether too many economic commentators fail to grasp how the supply component may make the next global recession unlike the last two. In contrast to recessions driven mainly by a demand shortfall, the challenge posed by a supply-side-driven downturn is that it can result in sharp declines in production and widespread bottlenecks. In that case, generalized shortages – something that some countries have not seen since the gas lines of 1970s – could ultimately push inflation up, not down.

Admittedly, the initial conditions for containing generalized inflation today are extraordinarily favorable. But, given that four decades of globalization has almost certainly been the main factor underlying low inflation, a sustained retreat behind national borders, owing to a COVID-19 pandemic (or even lasting fear of pandemic), on top of rising trade frictions, is a recipe for the return of upward price pressures. In this scenario, rising inflation could prop up interest rates and challenge both monetary and fiscal policymakers.

It is also noteworthy that the COVID-19 crisis is hitting the world economy when growth is already soft and many countries are wildly overleveraged.Global growth in 2019 was only 2.9%, not so far from the 2.5% level that has historically constituted a global recession. Italy’s economy was barely starting to recover before the virus hit. Japan’s was already tipping into recession after an ill-timed hike in the value-added tax, and Germany’s has been teetering amidst political disarray. The United States is in the best shape, but what once seemed like a 15% chance of a recession starting before the presidential and congressional elections in November now seems much higher.

It might seem strange that the new coronavirus could cause so much economic damage even to countries that seemingly have the resources and technology to fight back. A key reason is that earlier generations were much poorer than today, so many more people had to risk going to work. Unlike today, radical economic pullbacks in response to epidemics that did not kill most people were not an option.

What has happened in Wuhan, China, the current outbreak’s epicenter, is extreme but illustrative. The Chinese government has essentially locked down Hubei province, putting its 58 million people under martial law, with ordinary citizens unable to leave their houses except under very specific circumstances. At the same time, the government apparently has been able to deliver food and water to Hubei’s citizens for roughly six weeks now, something a poor country could not imagine doing.

Elsewhere in China, a great many people in major cities such as Shanghai and Beijing have remained indoors most of the time in order to reduce their exposure. Governments in countries such as South Korea and Italy may not be taking the extreme measures that China has, but many people are staying home, implying a significant adverse impact on economic activity.

The odds of a global recession have risen dramatically, much more than conventional forecasts by investors and international institutions care to acknowledge. Policymakers need to recognize that, besides interest rate cuts and fiscal stimulus, the huge shock to global supply chains also needs to be addressed. The most immediate relief could come from the US sharply scaling back its trade-war tariffs, thereby calming markets, exhibiting statesmanship with China, and putting money in the pockets of US consumers. A global recession is a time for cooperation, not isolation.

Investment-grade corporate bonds have been a major tailwind to the economic cycle as yields continue to drop.

Treasury bond yields are falling faster than IG spreads are widening, resulting in lower borrowing costs, but a major increase in late 2018 may have triggered a change in employment.

A rise in corporate bond yields impacts cash flows, margins and, eventually, employment decisions.

Corporate bond prices (yields) are a long leading indicator that impacts the economic cycle through changes in corporate capital spending and employment.

The corporate sector is more leveraged than previous economic cycles. A recession can be triggered if the Coronavirus outbreak causes corporate rates to rise, accelerating the decline in employment growth.

I do much more than just articles at EPB Macro Research: Members get access to model portfolios, regular updates, a chat room, and more. Get started today »

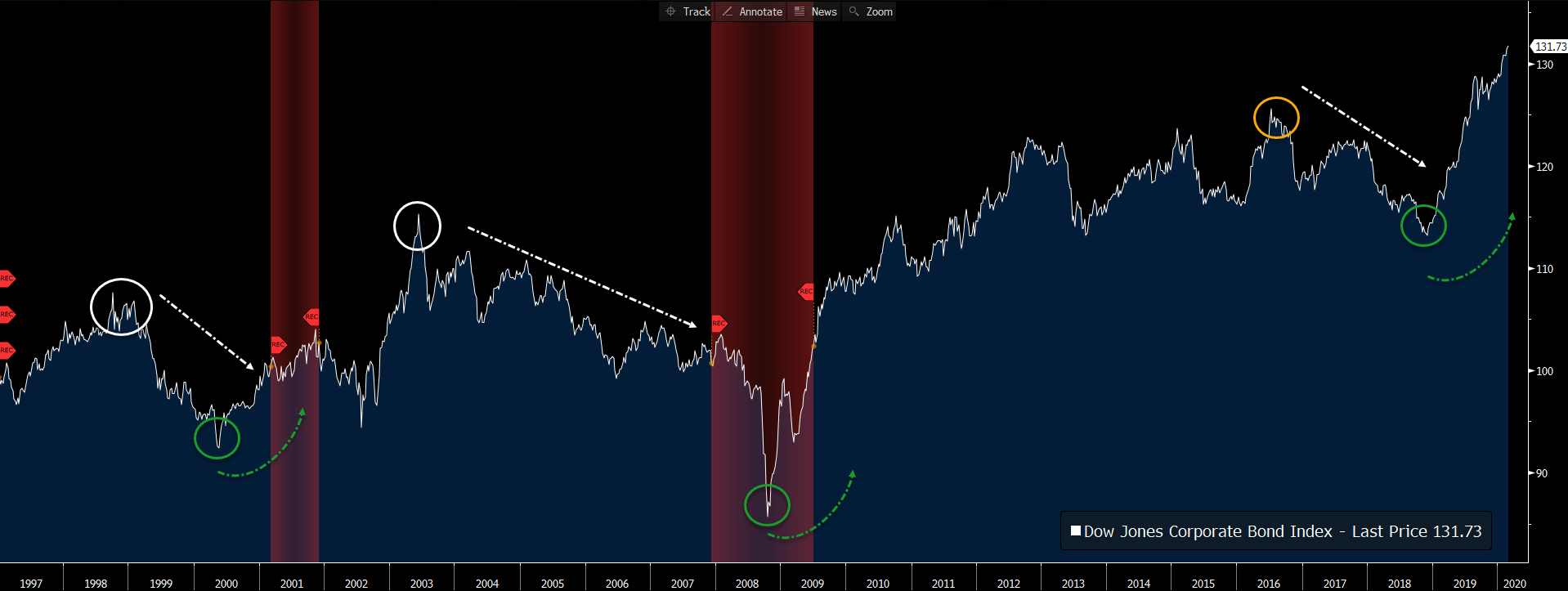

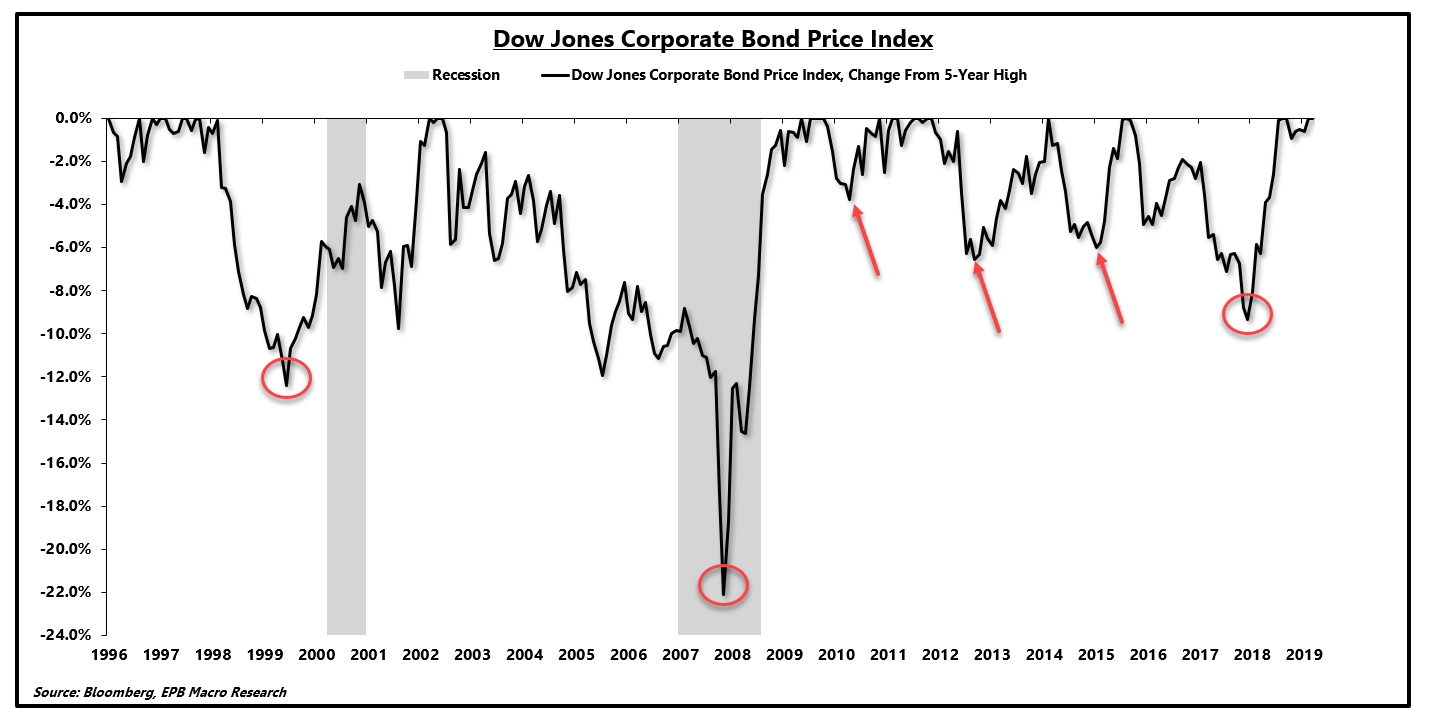

Along with money supply, building permits and corporate margins, corporate bond prices or corporate bond yields fall into the “long leading” indicator bucket, according to “the father of leading indicators,” Geoffrey Moore. Geoffrey Moore’s work found value in using the Dow Jones Corporate Bond Price Index (graphed below), but any measure of corporate bond yields will likely yield similar results. If using bond yields rather than bond prices, the indicator should be inverted as higher corporate bond yields usually translate to lower profit margins and slowing employment growth.

Dow Jones Corporate Bond Price Index:

Source: Bloomberg, EPB Macro Research

As the chart clearly shows, lead times before a recession can be quite long while lead times for recovery are more abrupt. The recovery (or suddenly lower corporate bond yields) has historically been quite helpful in restarting the hiring process and capital spending process.

From an economic cycle sequence perspective, lower bond prices or higher corporate bond yields reduce margins/profitability and have a resulting impact on the rate of capital spending and employment plans. The drop in capex and reduction in employment growth is what ultimately leads to lower income growth, consumption growth, and, eventually, a recession.

In Lacy Hunt’s most recent Quarterly Review and Outlook, he outlined Milton Friedman’s work, which explains that monetary changes (interest rates) and economic cycle impacts typically cluster around two years.

As the research of Nobel Laureate Milton Friedman documented, the typical lags between monetary change and economic fluctuations cluster around two years, confirming the importance of the two-year time frame.

A change in interest rates today may impact future projects. Still, existing investments will likely continue, resulting in a lag between the change in interest rates and the impact on more coincident economic data such as employment.

As a result of this finding, when studying interest rates, it can be valuable to use a 24-month change formula rather than a year-over-year method to more closely capture the two-year cluster.

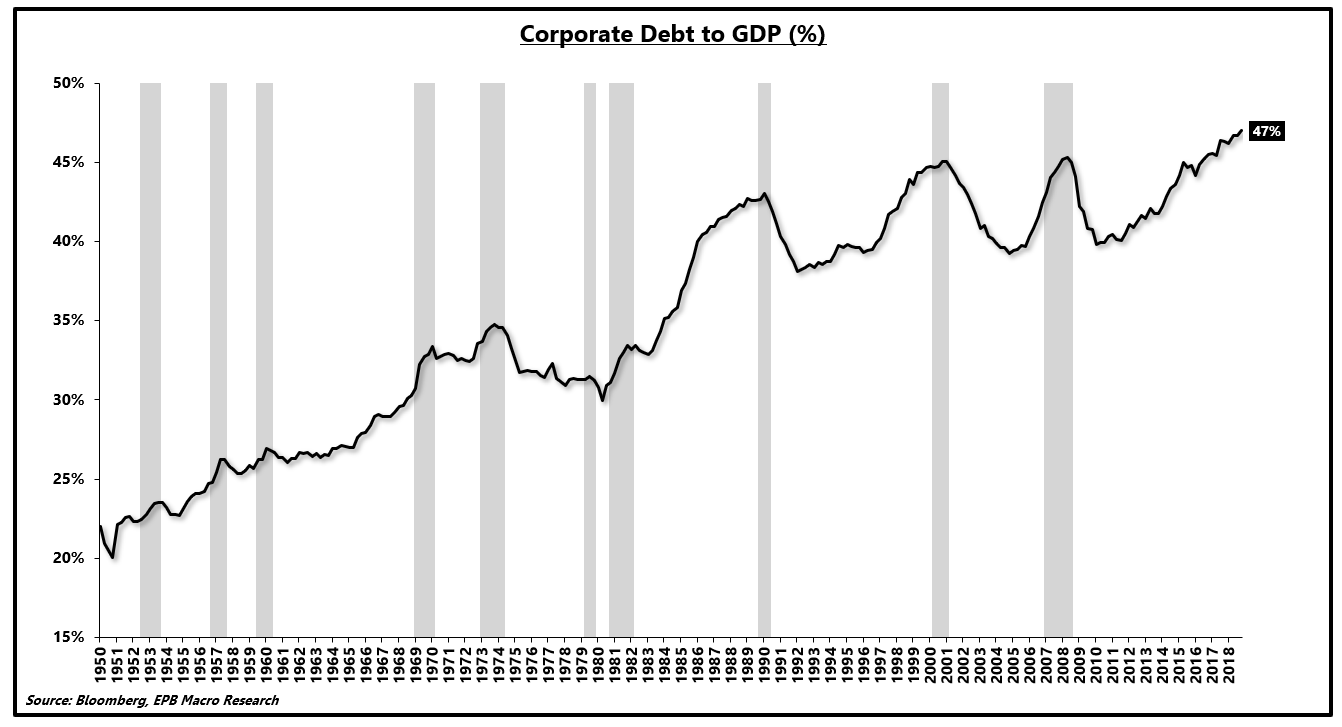

The last point to stress before highlighting some of the more recent trends is that the level of corporate debt is at a record high relative to GDP.

Corporate Debt to GDP Ratio:

Source: Bloomberg, EPB Macro Research

Thus, similar to federal debt, there are diminishing marginal returns or reduced efficacy of each new dollar of debt. More importantly, however, smaller changes in interest rates (corporate bond prices) can have a similar or larger impact on corporate health and the resulting repercussions on overall employment.

Throughout the rest of this note, we will look at the impact of changes in corporate bond prices (yields) and the lagged relationship to employment, as well as some considerations when making a recession forecast.

Currently, corporate bond yields are still falling because Treasury rates are declining faster than spreads are widening. Lower corporate bond yields are helpful on the margin, but the late 2018 spike (two-year cluster) may have been enough to start the process of reduced employment, something very evident in recent data. If the Coronavirus outbreak causes corporate bond yields to rise and accelerates the existing decline in employment growth, a recession is very much in the cards.

Today’s rate of employment growth is insufficient to trigger a recession based on past samples. Still, when an existing downward trend is coupled with a negative shock, recession risk must remain firmly on the table.

US Corporate Sector Health Heading Into 2018

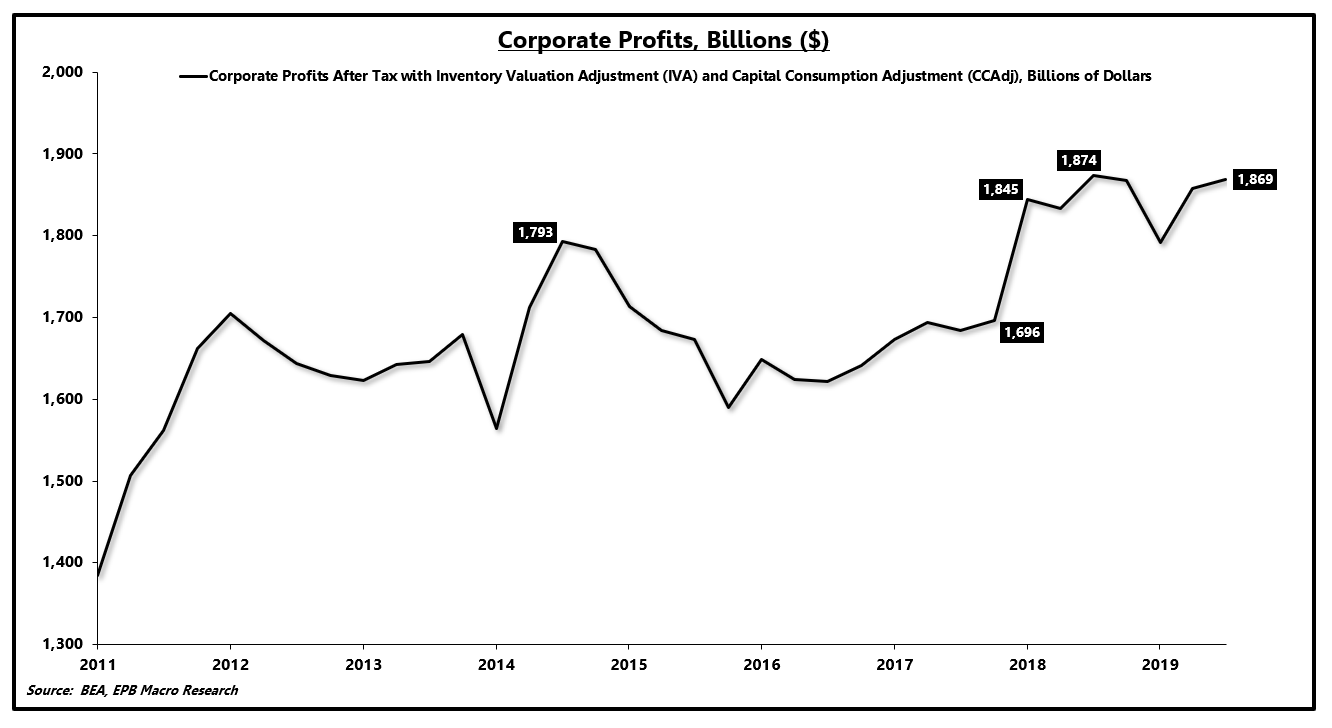

Corporate America has been plagued by anemic economic growth in this economic cycle. Masked by the rising share price of roughly 500 companies, thousands of corporations that aren’t publicly traded have been forced to operate in a low-profit growth regime.

Financial engineering has allowed publicly-traded companies to report strong earnings growth. Total corporate profits reported in the GDP report is a far more accurate, albeit delayed, data source on the real (non-adjusted) profits generated by the corporate sector.

From 2014 through the start of 2018, corporate profits declined. The one-time spike in profits after 2018 was due to the corporate tax cut. Essentially, without the corporate tax cut, the corporate sector has seen virtually no profit growth since 2014.

Corporate Profits:

Source: Bloomberg, EPB Macro Research

On a five-year annualized basis, corporate profits have increased by just 2.2% with the latest year-over-year reading falling 0.3%.

Amazingly, corporate debt has increased, and share prices have soared with very little profit growth, a phenomenon exposed by persistently lower Treasury rates.

Corporate Profits Growth:

Source: Bloomberg, EPB Macro Research

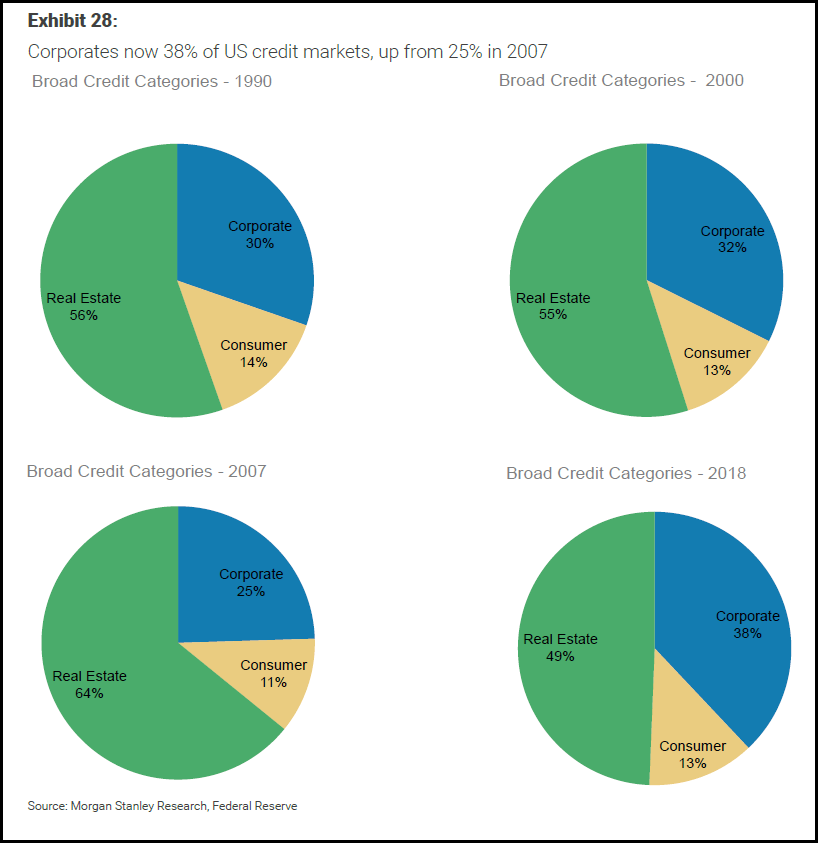

Stacking together real estate debt, corporate debt, and consumer debt shows that the largest increase across economic cycles is coming from the corporate sector.

In the last economic cycle, corporate debt was only 25% of the credit market. In 2018, corporate credit increased to 38% of the total.

Corporate Sector Debt As A % of Total:

Source: Morgan Stanley, EPB Macro Research

As a result of lower profits and more debt, the leverage ratio in corporate America has surged to recessionary levels.

Importantly, the leverage ratio usually increases during a recession as profits (the denominator) fall. Morgan Stanley’s research from 2018 calls out that leverage is at an all-time high in a “healthy economy,” which highlights just how leveraged and sensitive to changes in interest rates the corporate sector has become.

Corporate Sector Leverage:

Source: Morgan Stanley, EPB Macro Research

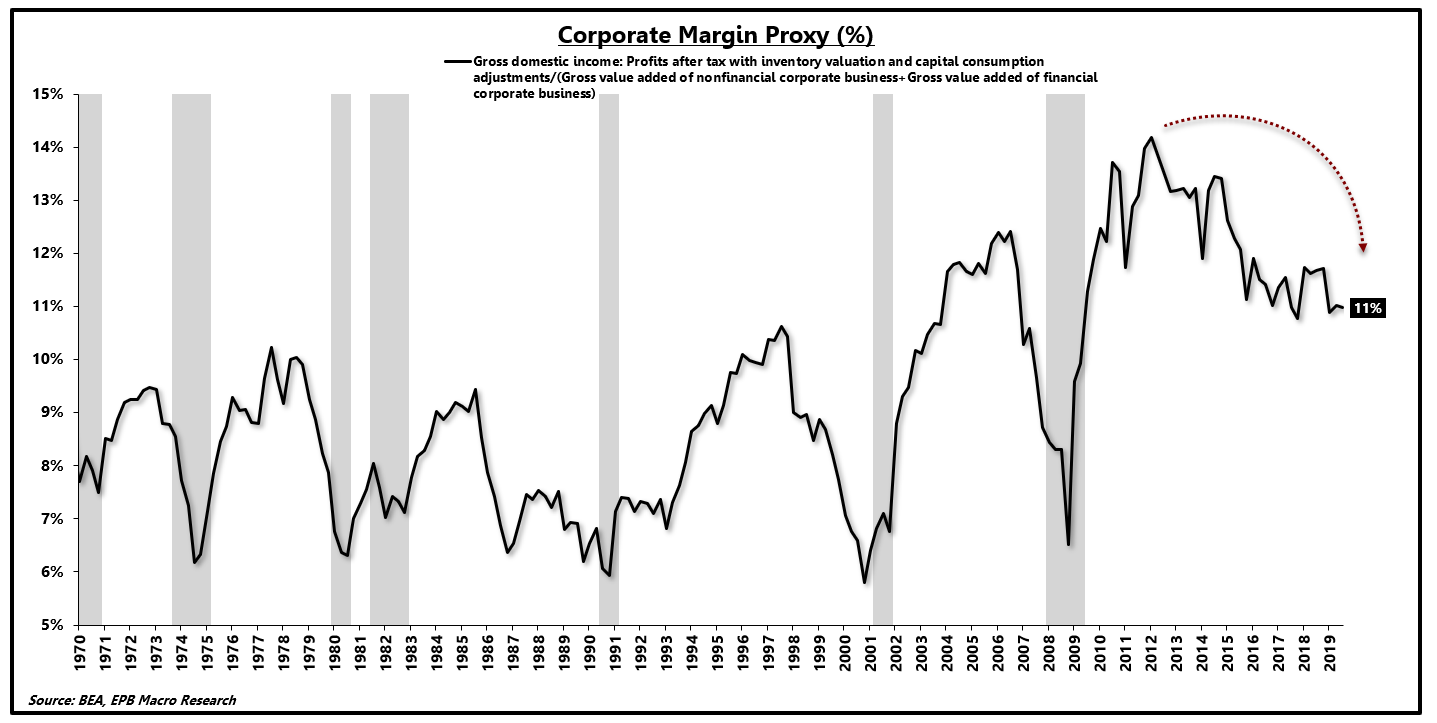

When corporate borrowing costs rise, employment typically suffers as the increase in interest expense compresses margins.

Again, due to weak economic growth and lackluster profit growth across the entire corporate sector, margins (proxied below) have been compressing since the early stages of this economic cycle.

Lower margins foreshadow weaker employment growth and capital spending growth.

Corporate Margins:

Source: Bloomberg, EPB Macro Research

With corporate leverage at extreme levels and corporate margins already in decline, the corporate sector was particularly vulnerable to any spike in corporate borrowing costs as a result of an economic slowdown.

When the Federal Reserve embarked on a monetary tightening cycle, economic conditions globally started to deteriorate with a lag, hitting most economies in 2018 and 2019.

US corporate borrowing costs surged in late 2018 and early 2019, which triggered a more aggressive decline in employment growth and persistent weakness in capital spending growth.

Late 2018 Credit Event – Enough To Trigger A Recession?

Typically, before recessions, corporate bond prices decline (yields increase) as the Federal Reserve is raising interest rates, and the tighter monetary conditions eventually slow the economy, leading to wider corporate bond spreads.

Corporate bond prices declined three other times this economic cycle, coinciding with the three economic slowdowns before the current downturn.

The 2018 decline in corporate bond prices was larger than the previous three, a sign that economic conditions would weaken. When comparing to the past two recessionary samples, the decline in 2018 was marginally weaker than in 1999. Still, given the leverage ratio and decline in margins, a smaller decline could have a similar impact.

Corporate Bond Prices Tumble:

Source: Bloomberg, EPB Macro Research

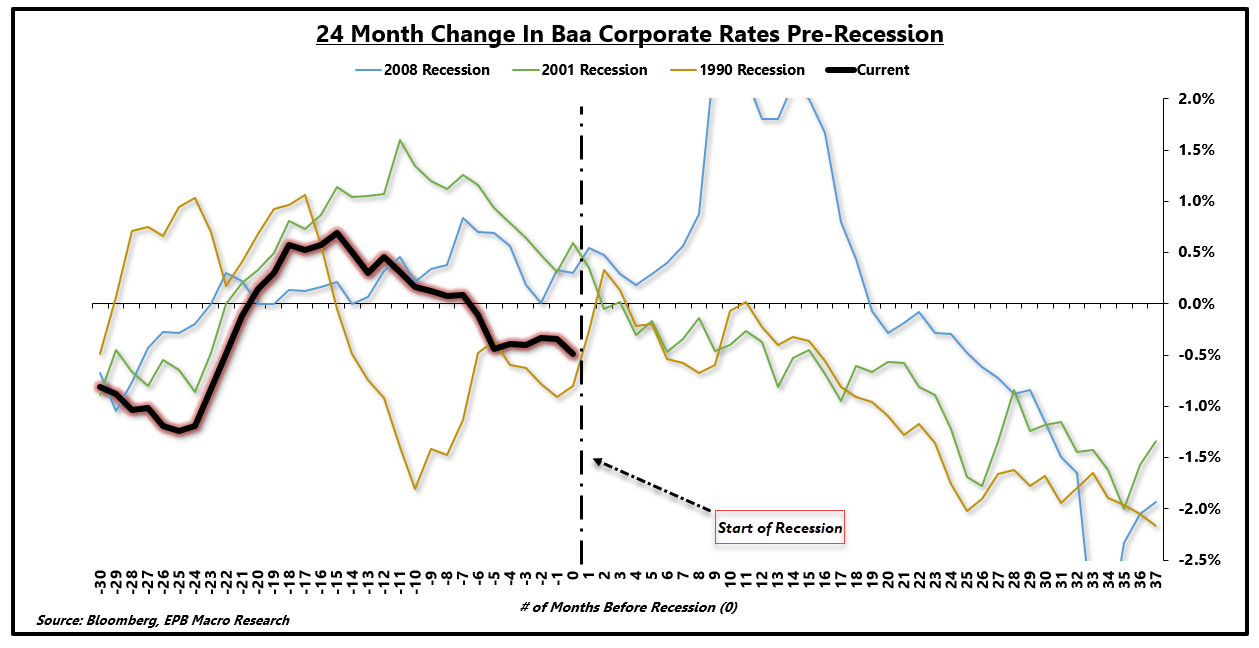

Graphed another way, the chart below shows the 24-month change in Baa corporate bond yields.

The chart is graphed by the number of months before/after a recession with 0 on the x-axis indicating the start of a recession.

The 2018 rise in corporate bond yields was undoubtedly less than the previous three samples, only spending 14 months above 0% on a 24-month change.

Corporate Bond Yield 24-Month Change:

Source: Bloomberg, EPB Macro Research

The corporate sector is far more levered today, with weaker margins and lower trend growth as compared to the prior three recessions.

Thus it remains possible that the decline in corporate bond prices was enough to trigger a downshift in employment growth, an effort to preserve margins.

Impact On The Real Economy

Cycles in employment can be monitored separately from cycles in growth. Geoffrey Moore tracked cycles in growth, inflation, and jobs independently.

Leading indicators of economic growth turned lower very early in 2018, some in late 2017. Inflation indicators did not plunge until September 2018, and jobs growth did not inflect lower until corporate bond yields spiked in late 2018.

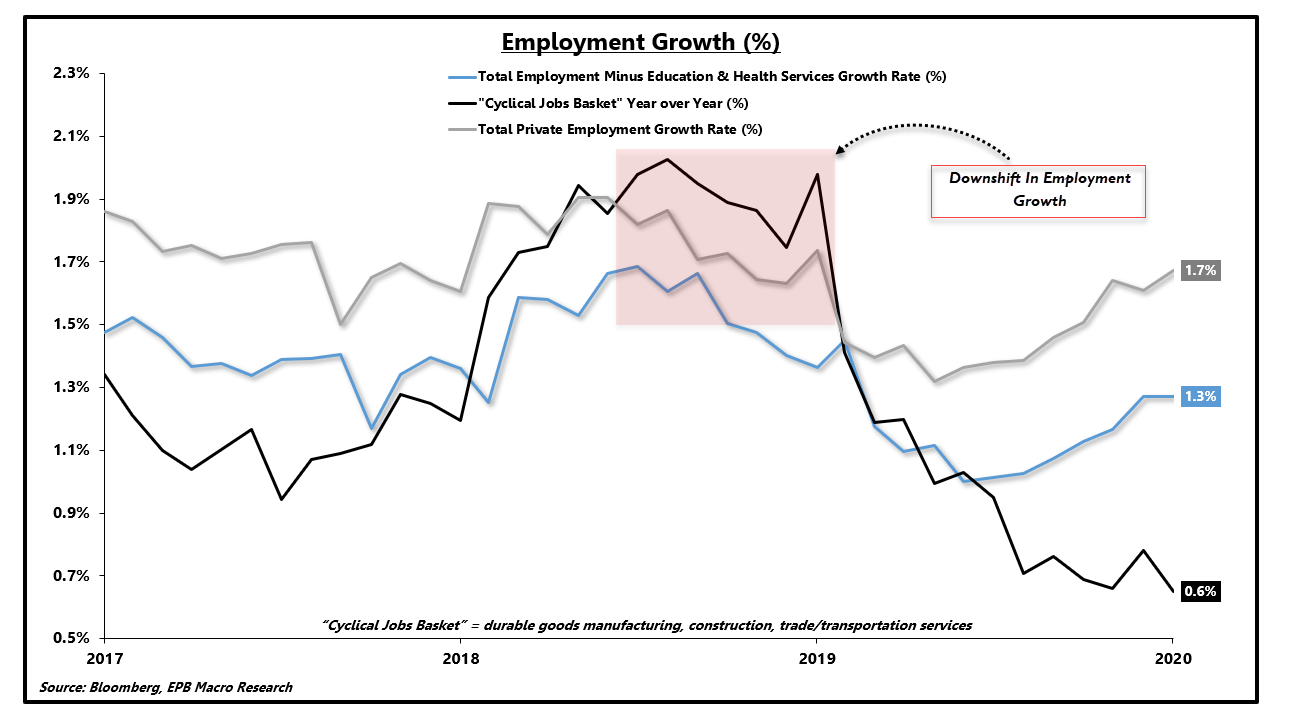

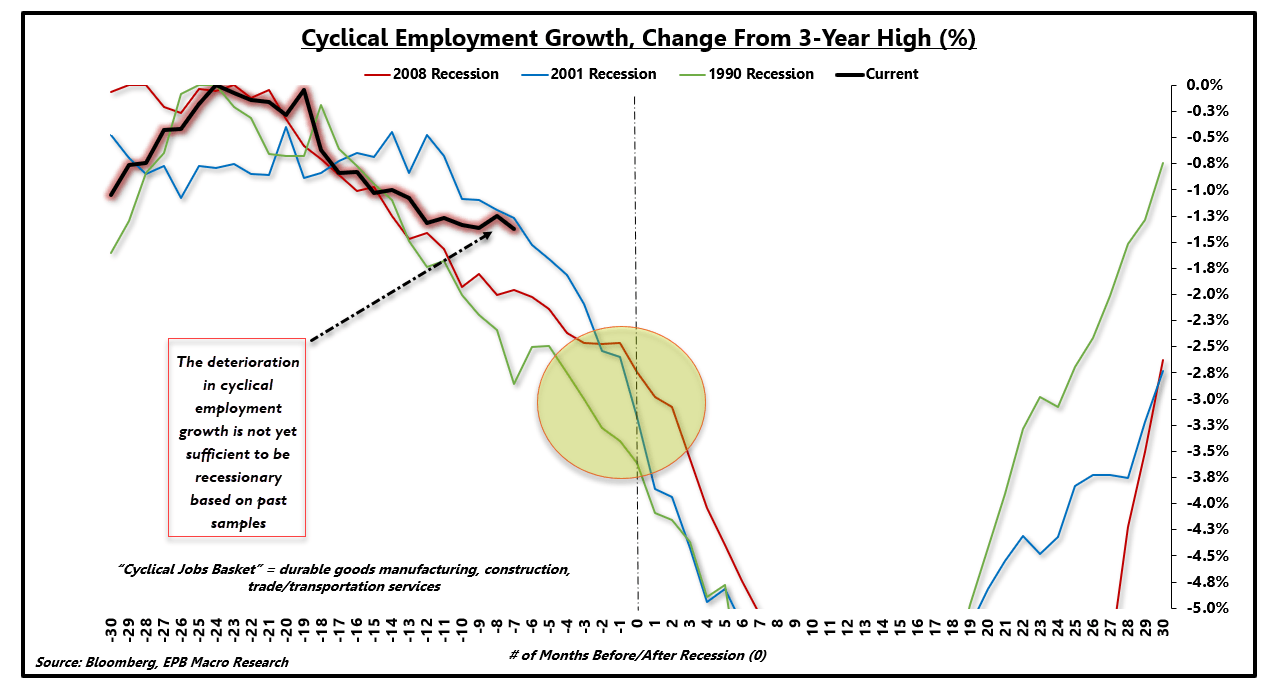

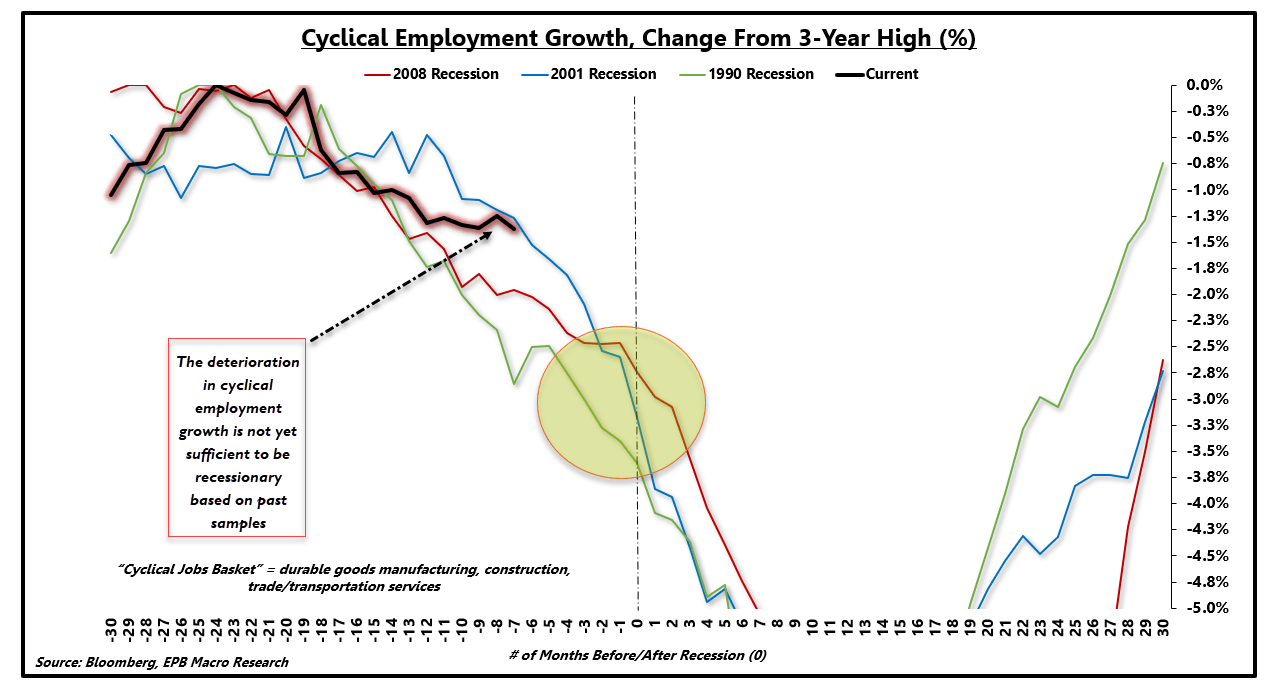

Cyclical employment, defined in the chart below as durable goods manufacturing, construction, and trade/transportation services, started to show rapidly-declining rates of growth.

Employment Growth Changed:

Source: Bloomberg, EPB Macro Research

If we track the change in cyclical employment growth before the three previous recessions, we can see recessionary periods begin with similar declines in cyclical employment.

Today’s current track of cyclical employment growth is currently insufficient to be recessionary based on past samples. However, if the trajectory does not flatten or inflect higher, history suggests that income and consumption growth will follow, leading to recessionary conditions.

Employment Growth Trend Relative To Past Samples:

Source: Bloomberg, EPB Macro Research

Employment growth over the next six months remains critical. If corporations continue to post weaker rates of employment growth or accelerate layoffs as a result of the Coronavirus outbreak, a recession is still firmly in play.

An existing trend of weaker growth and employment, originated by the Federal Reserve tightening cycle and deleveraging in China, exposed the economy to a negative shock.

It’s clear using the chart above how a negative shock (COVID-2019) coupled with an existing downturn in growth/employment can create a recession.

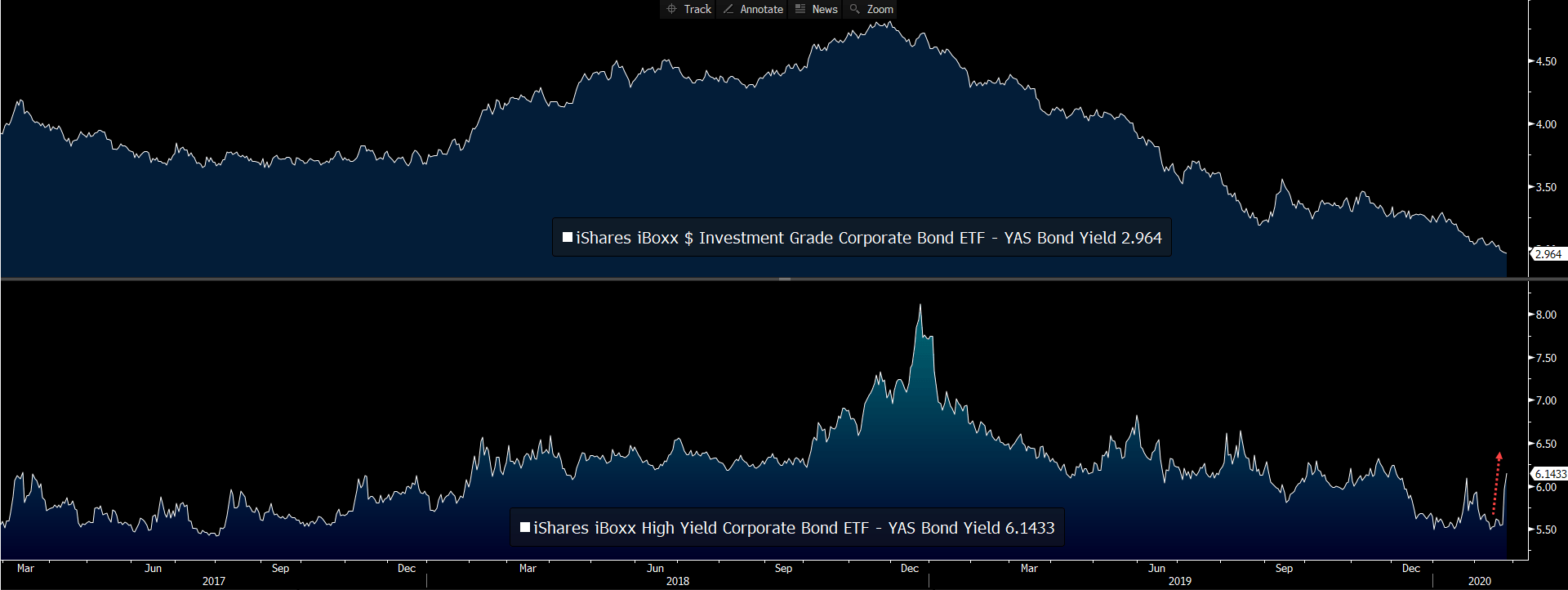

The Current Shock

The current economic shock has resulted in a widening of corporate bond spreads. Using popular credit ETFs (LQD) and (HYG), we can track the implied spread above Treasury bonds. Both investment-grade and high-yield credit spreads, particularly high yield, have been widening materially in the past several weeks.

Investment-Grade / High-Yield Corporate Spreads:

Source: Bloomberg, EPB Macro Research

Luckily, however, corporate yields are a function of Treasury rates plus a spread.

For investment-grade bonds, Treasury rates are still declining faster than spreads are increasing, resulting in lower investment-grade bond yields.

High-yield bonds, however, are starting to see higher yields, a firm negative for corporate margins and future employment.

Investment-Grade / High-Yield Corporate Bond Yields:

Source: Bloomberg, EPB Macro Research

The current slowdown in employment growth, specifically cyclical employment growth, is severe and can be seen in many economic data points. If leading indicators of economic growth were turning higher, however, and cyclical employment growth started to increase, the economy may very well avoid a recession.

The negative shock of the Coronavirus has likely caused employment plans to freeze, irrespective of any increase in borrowing costs.

If the Coronavirus continues to cause a sell-off in risk assets and spreads start to widen faster than Treasury rates decline, corporations will be faced with higher borrowing costs at a time when economic growth was on shaky ground to being with.

Employment Growth Trend Relative To Past Samples:

Source: Bloomberg, EPB Macro Research

Should an increase in borrowing costs accelerate the decline in employment growth, and the black line in the chart above drifts into the yellow circle, a recession will be tough to avoid.

Clearly, a call for a recession is premature, and my economic outlook has zero forecasts concerning the virus or any predictions regarding a conclusion.

Rather, when constructing an allocation to weather a shock, we must be mindful of the current state of the economy and the susceptibility to a recession from a negative event.

Currently, a recession is not imminent based on the data above. Still, the situation can evolve quickly, and the economy is far from immune to a shock in its current state.

Keys To Watch and Outlook

The increase in corporate bond yields late in 2018 was small in relation to other recessionary periods. Still, given

the level of corporate leverage,

anemic profit growth, and

weak economic conditions,

a smaller increase can have a more significant impact.

Employment growth has been in a downtrend since that late 2018 period, contributing to weaker rates of consumption growth seen in recent reports.

The economy is not imminently vulnerable to a recession, but that can change in a matter of weeks. The impact on employment is the key to watch when judging lasting recession risk.

Moving forward, if the current shock causes employment growth to suffer, already in a fragile state, recessionary conditions will be tough to avoid.

An acceleration in corporate layoffs will be exacerbated by higher borrowing costs, making credit spreads and bond prices a vital signal.

Given the susceptibility to a recession pending a worsening of conditions, investors should consider an added layer of protection should this negative shock take a turn for the worse.

If conditions worsen or simply do not improve for several weeks, a recession may be difficult to avoid, mainly due to the initial conditions before the shock began.

If the economy does tumble into a recession, risk assets are highly exposed, and a continued overweight allocation to Treasury bonds and gold will likely offer the best protection.

The model portfolio at EPB Macro Research continues to have an overweight exposure to Treasury bonds and gold.

Source: Bloomberg, EPB Macro Research

Source: Bloomberg, EPB Macro Research

Source: Morgan Stanley, EPB Macro Research

Source: Morgan Stanley, EPB Macro Research

Source: Bloomberg, EPB Macro Research

Source: Bloomberg, EPB Macro Research

Source: Bloomberg, EPB Macro Research

Source: Bloomberg, EPB Macro Research

Source: Bloomberg, EPB Macro Research

CAMBRIDGE – It is too soon to predict the long-run arc of the coronavirus outbreak. But it is not too soon to recognize that the next global recession could be around the corner – and that it may look a lot different from those that began in 2001 and 2008.

For starters, the next recession is likely to emanate from China, and indeed may already be underway. China is a highly leveraged economy, it cannot afford a sustained pause today anymore than fast-growing 1980s Japan could. People, businesses, and municipalities need funds to pay back their out-size debts. Sharply adverse demographics, narrowing scope for technological catch-up, and a huge glut of housing from recurrent stimulus programs – not to mention an increasingly centralized decision-making process – already presage significantly slower growth for China in the next decade.

Moreover, unlike the two previous global recessions this century, the new coronavirus, COVID-19, implies a supply shock as well as a demand shock. Indeed, one has to go back to the oil-supply shocks of the mid-1970s to find one as large. Yes, fear of contagion will hit demand for airlines and global tourism, and precautionary savings will rise. But when tens of millions of people can’t go to work (either because of a lockdown or out of fear), global value chains break down, borders are blocked, and world trade shrinks because countries distrust of one another’s health statistics, the supply side suffers at least as much.

Affected countries will, and should, engage in massive deficit spending to shore up their health systems and prop up their economies. The point of saving for a rainy day is to spend when it rains, and preparing for pandemics, wars, climate crises, and other out-of-the-box events is precisely why open-ended deficit spending during booms is dangerous.

But policymakers and altogether too many economic commentators fail to grasp how the supply component may make the next global recession unlike the last two. In contrast to recessions driven mainly by a demand shortfall, the challenge posed by a supply-side-driven downturn is that it can result in sharp declines in production and widespread bottlenecks. In that case, generalized shortages – something that some countries have not seen since the gas lines of 1970s – could ultimately push inflation up, not down.

Admittedly, the initial conditions for containing generalized inflation today are extraordinarily favorable. But, given that four decades of globalization has almost certainly been the main factor underlying low inflation, a sustained retreat behind national borders, owing to a COVID-19 pandemic (or even lasting fear of pandemic), on top of rising trade frictions, is a recipe for the return of upward price pressures. In this scenario, rising inflation could prop up interest rates and challenge both monetary and fiscal policymakers.

It is also noteworthy that the COVID-19 crisis is hitting the world economy when growth is already soft and many countries are wildly overleveraged. Global growth in 2019 was only 2.9%, not so far from the 2.5% level that has historically constituted a global recession. Italy’s economy was barely starting to recover before the virus hit. Japan’s was already tipping into recession after an ill-timed hike in the value-added tax, and Germany’s has been teetering amidst political disarray. The United States is in the best shape, but what once seemed like a 15% chance of a recession starting before the presidential and congressional elections in November now seems much higher.

It might seem strange that the new coronavirus could cause so much economic damage even to countries that seemingly have the resources and technology to fight back. A key reason is that earlier generations were much poorer than today, so many more people had to risk going to work. Unlike today, radical economic pullbacks in response to epidemics that did not kill most people were not an option.

What has happened in Wuhan, China, the current outbreak’s epicenter, is extreme but illustrative. The Chinese government has essentially locked down Hubei province, putting its 58 million people under martial law, with ordinary citizens unable to leave their houses except under very specific circumstances. At the same time, the government apparently has been able to deliver food and water to Hubei’s citizens for roughly six weeks now, something a poor country could not imagine doing.

Elsewhere in China, a great many people in major cities such as Shanghai and Beijing have remained indoors most of the time in order to reduce their exposure. Governments in countries such as South Korea and Italy may not be taking the extreme measures that China has, but many people are staying home, implying a significant adverse impact on economic activity.

The odds of a global recession have risen dramatically, much more than conventional forecasts by investors and international institutions care to acknowledge. Policymakers need to recognize that, besides interest rate cuts and fiscal stimulus, the huge shock to global supply chains also needs to be addressed. The most immediate relief could come from the US sharply scaling back its trade-war tariffs, thereby calming markets, exhibiting statesmanship with China, and putting money in the pockets of US consumers. A global recession is a time for cooperation, not isolation.