Summary

Investment-grade corporate bonds have been a major tailwind to the economic cycle as yields continue to drop.

Treasury bond yields are falling faster than IG spreads are widening, resulting in lower borrowing costs, but a major increase in late 2018 may have triggered a change in employment.

A rise in corporate bond yields impacts cash flows, margins and, eventually, employment decisions.

Corporate bond prices (yields) are a long leading indicator that impacts the economic cycle through changes in corporate capital spending and employment.

The corporate sector is more leveraged than previous economic cycles. A recession can be triggered if the Coronavirus outbreak causes corporate rates to rise, accelerating the decline in employment growth.

I do much more than just articles at EPB Macro Research: Members get access to model portfolios, regular updates, a chat room, and more. Get started today »

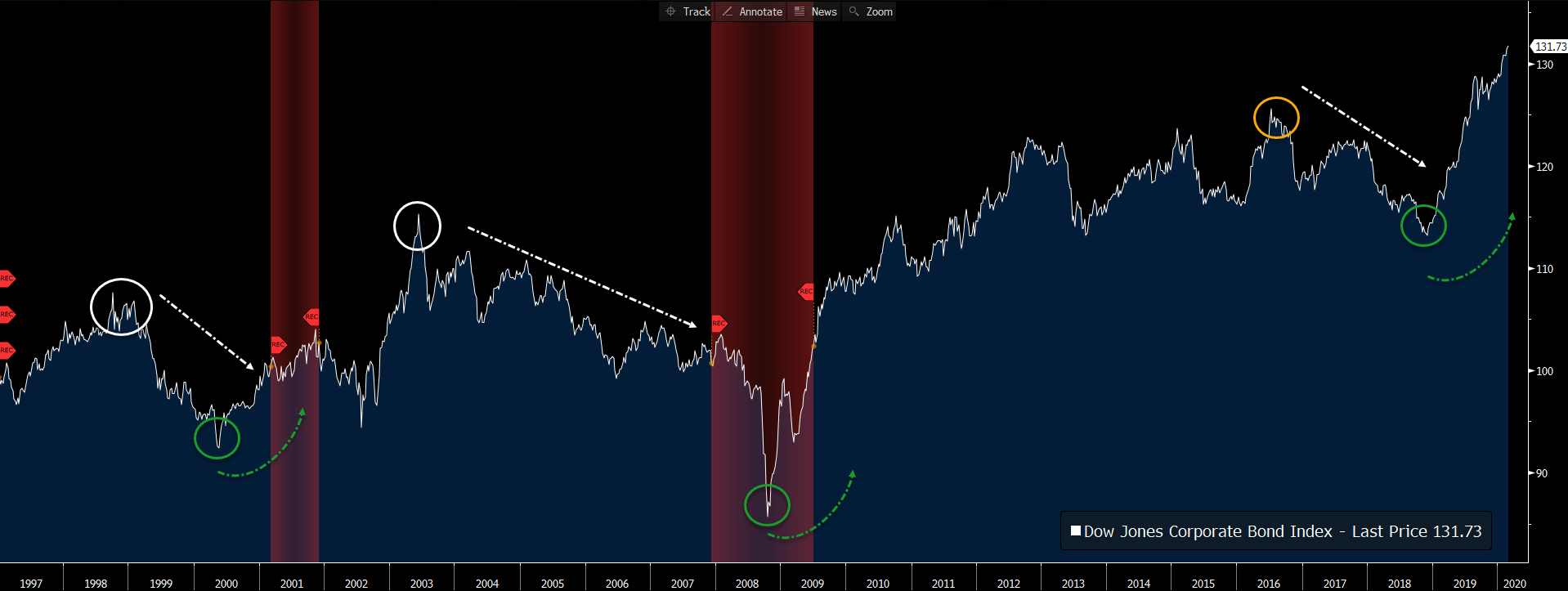

Along with money supply, building permits and corporate margins, corporate bond prices or corporate bond yields fall into the “long leading” indicator bucket, according to “the father of leading indicators,” Geoffrey Moore. Geoffrey Moore’s work found value in using the Dow Jones Corporate Bond Price Index (graphed below), but any measure of corporate bond yields will likely yield similar results. If using bond yields rather than bond prices, the indicator should be inverted as higher corporate bond yields usually translate to lower profit margins and slowing employment growth.

Dow Jones Corporate Bond Price Index:

Source: Bloomberg, EPB Macro Research

As the chart clearly shows, lead times before a recession can be quite long while lead times for recovery are more abrupt. The recovery (or suddenly lower corporate bond yields) has historically been quite helpful in restarting the hiring process and capital spending process.

From an economic cycle sequence perspective, lower bond prices or higher corporate bond yields reduce margins/profitability and have a resulting impact on the rate of capital spending and employment plans. The drop in capex and reduction in employment growth is what ultimately leads to lower income growth, consumption growth, and, eventually, a recession.

In Lacy Hunt’s most recent Quarterly Review and Outlook, he outlined Milton Friedman’s work, which explains that monetary changes (interest rates) and economic cycle impacts typically cluster around two years.

As the research of Nobel Laureate Milton Friedman documented, the typical lags between monetary change and economic fluctuations cluster around two years, confirming the importance of the two-year time frame.

A change in interest rates today may impact future projects. Still, existing investments will likely continue, resulting in a lag between the change in interest rates and the impact on more coincident economic data such as employment.

As a result of this finding, when studying interest rates, it can be valuable to use a 24-month change formula rather than a year-over-year method to more closely capture the two-year cluster.

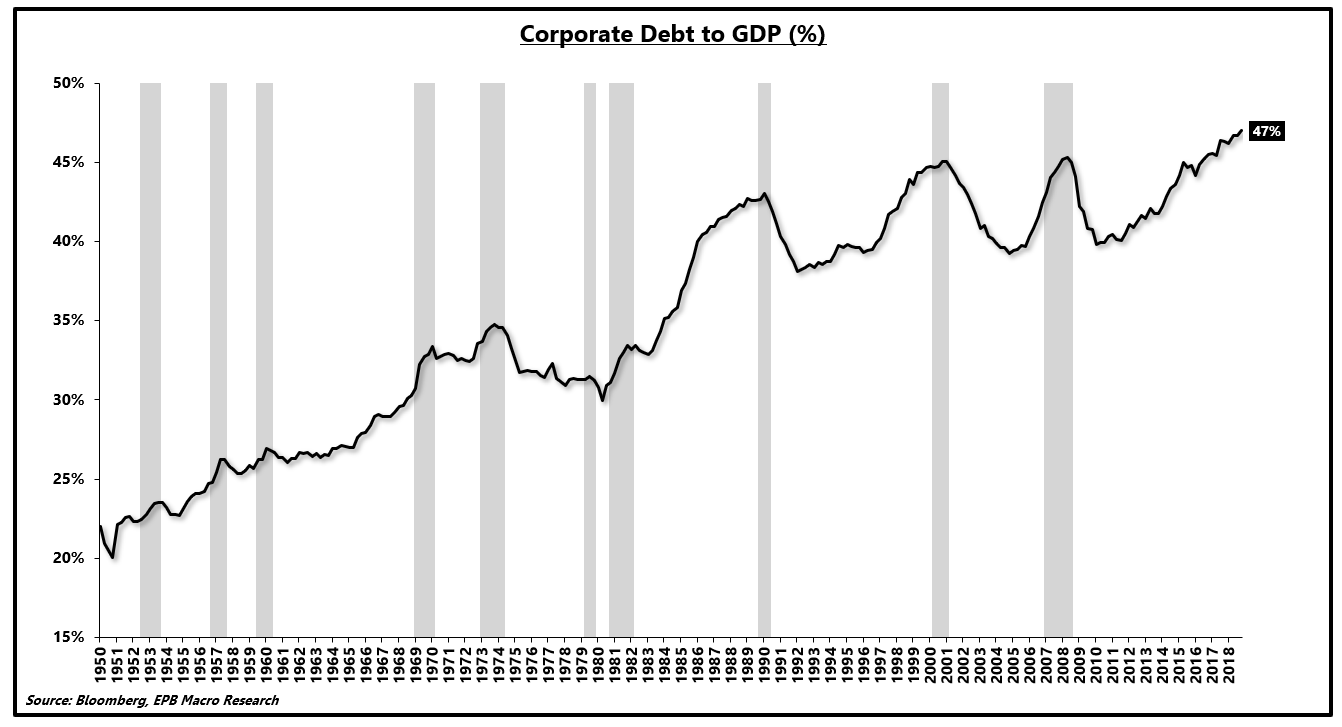

The last point to stress before highlighting some of the more recent trends is that the level of corporate debt is at a record high relative to GDP.

Corporate Debt to GDP Ratio:

Source: Bloomberg, EPB Macro Research

Thus, similar to federal debt, there are diminishing marginal returns or reduced efficacy of each new dollar of debt. More importantly, however, smaller changes in interest rates (corporate bond prices) can have a similar or larger impact on corporate health and the resulting repercussions on overall employment.

Throughout the rest of this note, we will look at the impact of changes in corporate bond prices (yields) and the lagged relationship to employment, as well as some considerations when making a recession forecast.

Currently, corporate bond yields are still falling because Treasury rates are declining faster than spreads are widening. Lower corporate bond yields are helpful on the margin, but the late 2018 spike (two-year cluster) may have been enough to start the process of reduced employment, something very evident in recent data. If the Coronavirus outbreak causes corporate bond yields to rise and accelerates the existing decline in employment growth, a recession is very much in the cards.

Today’s rate of employment growth is insufficient to trigger a recession based on past samples. Still, when an existing downward trend is coupled with a negative shock, recession risk must remain firmly on the table.

US Corporate Sector Health Heading Into 2018

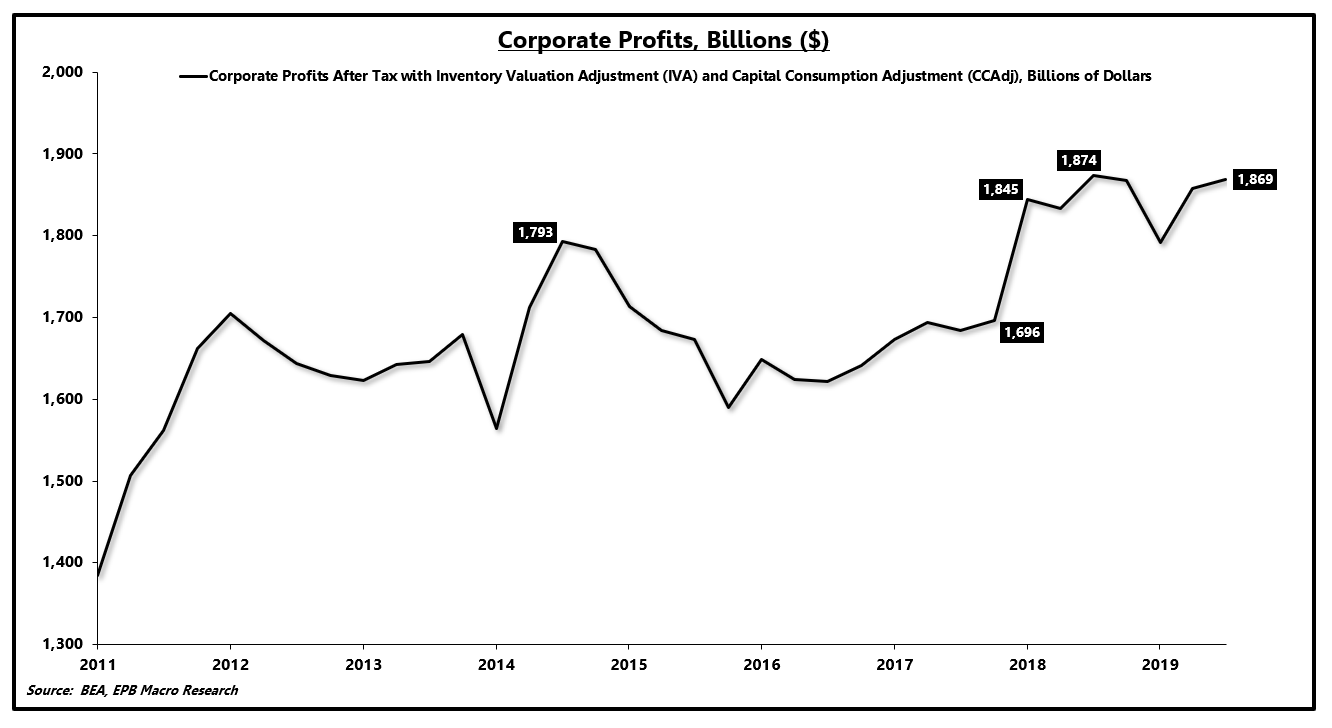

Corporate America has been plagued by anemic economic growth in this economic cycle. Masked by the rising share price of roughly 500 companies, thousands of corporations that aren’t publicly traded have been forced to operate in a low-profit growth regime.

Financial engineering has allowed publicly-traded companies to report strong earnings growth. Total corporate profits reported in the GDP report is a far more accurate, albeit delayed, data source on the real (non-adjusted) profits generated by the corporate sector.

From 2014 through the start of 2018, corporate profits declined. The one-time spike in profits after 2018 was due to the corporate tax cut. Essentially, without the corporate tax cut, the corporate sector has seen virtually no profit growth since 2014.

Corporate Profits:

Source: Bloomberg, EPB Macro Research

On a five-year annualized basis, corporate profits have increased by just 2.2% with the latest year-over-year reading falling 0.3%.

Amazingly, corporate debt has increased, and share prices have soared with very little profit growth, a phenomenon exposed by persistently lower Treasury rates.

Corporate Profits Growth:

Source: Bloomberg, EPB Macro Research

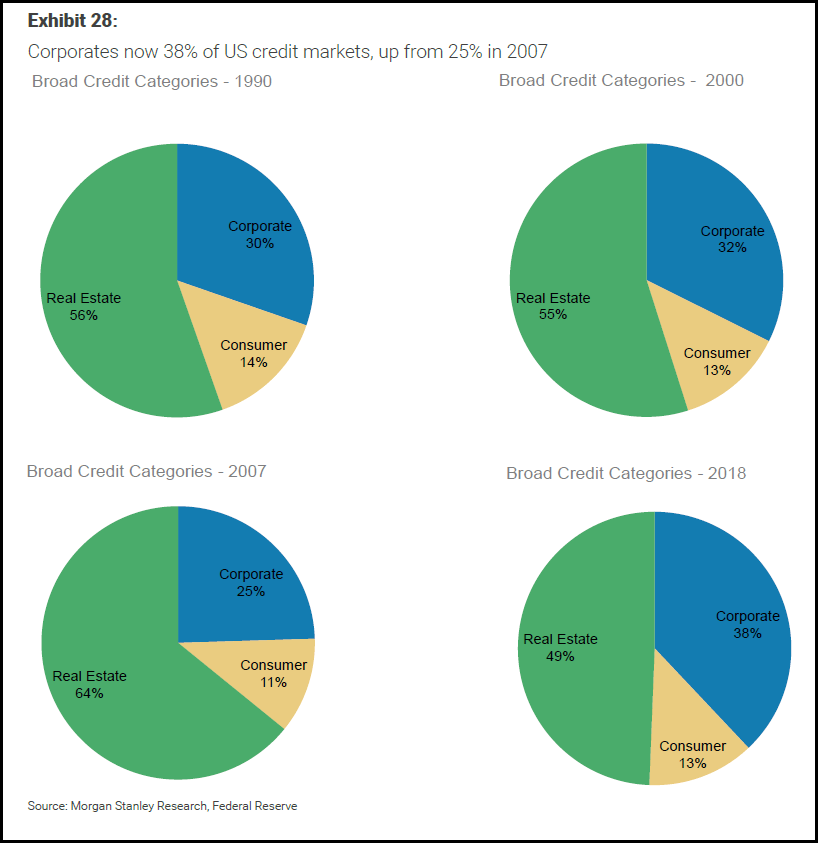

Stacking together real estate debt, corporate debt, and consumer debt shows that the largest increase across economic cycles is coming from the corporate sector.

In the last economic cycle, corporate debt was only 25% of the credit market. In 2018, corporate credit increased to 38% of the total.

Corporate Sector Debt As A % of Total:

Source: Morgan Stanley, EPB Macro Research

As a result of lower profits and more debt, the leverage ratio in corporate America has surged to recessionary levels.

Importantly, the leverage ratio usually increases during a recession as profits (the denominator) fall. Morgan Stanley’s research from 2018 calls out that leverage is at an all-time high in a “healthy economy,” which highlights just how leveraged and sensitive to changes in interest rates the corporate sector has become.

Corporate Sector Leverage:

Source: Morgan Stanley, EPB Macro Research

When corporate borrowing costs rise, employment typically suffers as the increase in interest expense compresses margins.

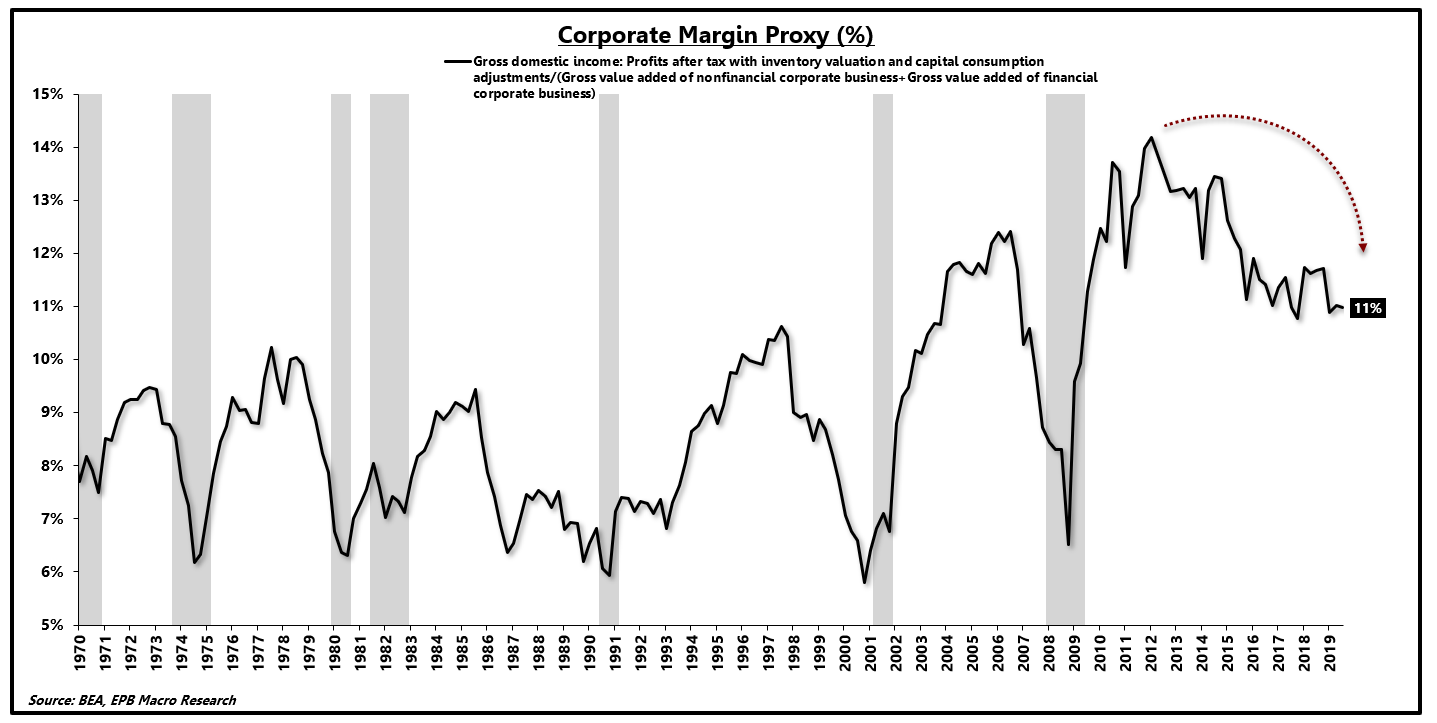

Again, due to weak economic growth and lackluster profit growth across the entire corporate sector, margins (proxied below) have been compressing since the early stages of this economic cycle.

Lower margins foreshadow weaker employment growth and capital spending growth.

Corporate Margins:

Source: Bloomberg, EPB Macro Research

With corporate leverage at extreme levels and corporate margins already in decline, the corporate sector was particularly vulnerable to any spike in corporate borrowing costs as a result of an economic slowdown.

When the Federal Reserve embarked on a monetary tightening cycle, economic conditions globally started to deteriorate with a lag, hitting most economies in 2018 and 2019.

US corporate borrowing costs surged in late 2018 and early 2019, which triggered a more aggressive decline in employment growth and persistent weakness in capital spending growth.

Late 2018 Credit Event – Enough To Trigger A Recession?

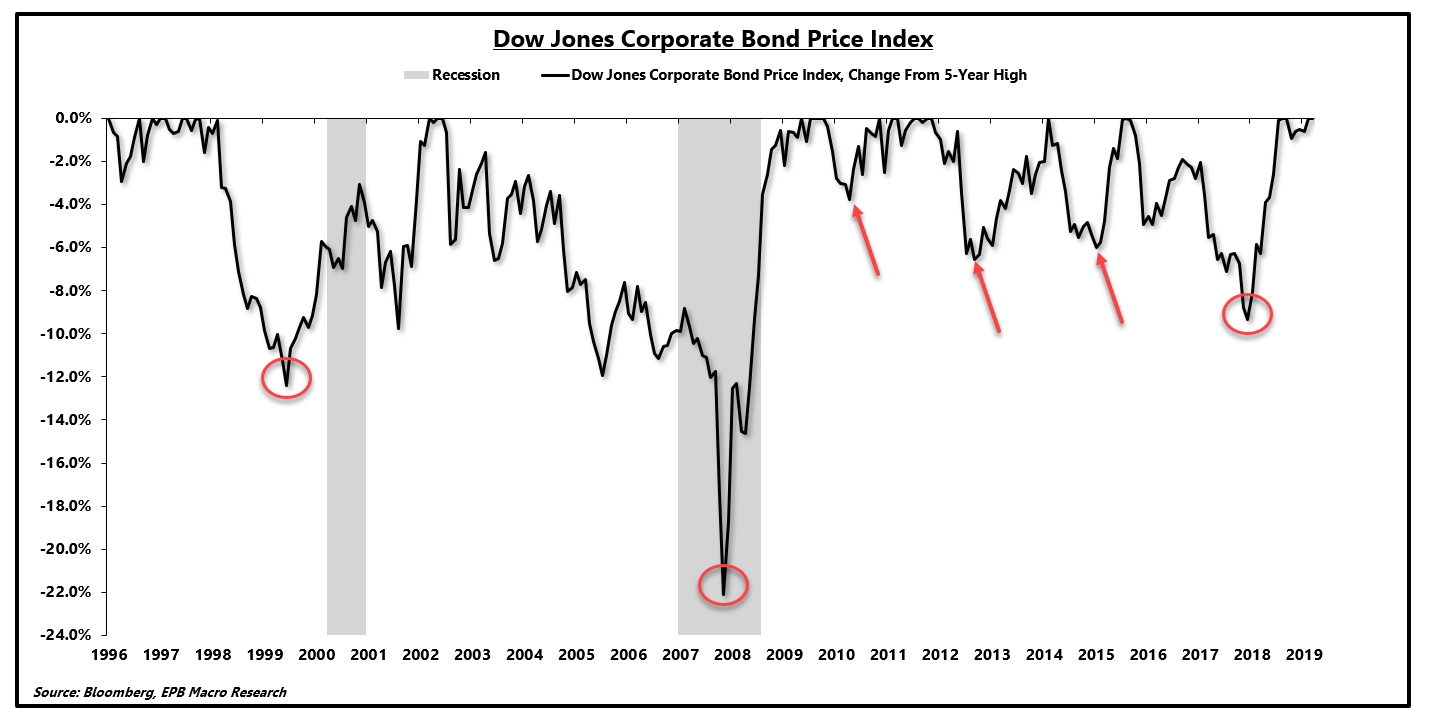

Typically, before recessions, corporate bond prices decline (yields increase) as the Federal Reserve is raising interest rates, and the tighter monetary conditions eventually slow the economy, leading to wider corporate bond spreads.

Corporate bond prices declined three other times this economic cycle, coinciding with the three economic slowdowns before the current downturn.

The 2018 decline in corporate bond prices was larger than the previous three, a sign that economic conditions would weaken. When comparing to the past two recessionary samples, the decline in 2018 was marginally weaker than in 1999. Still, given the leverage ratio and decline in margins, a smaller decline could have a similar impact.

Corporate Bond Prices Tumble:

Source: Bloomberg, EPB Macro Research

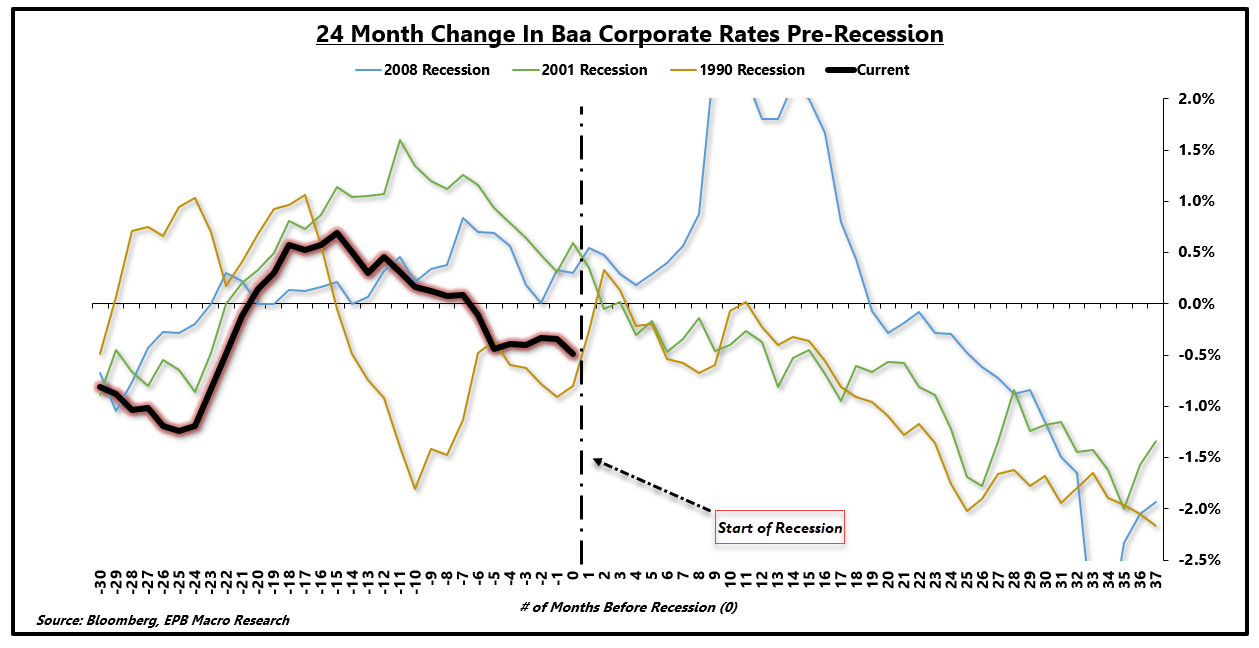

Graphed another way, the chart below shows the 24-month change in Baa corporate bond yields.

The chart is graphed by the number of months before/after a recession with 0 on the x-axis indicating the start of a recession.

The 2018 rise in corporate bond yields was undoubtedly less than the previous three samples, only spending 14 months above 0% on a 24-month change.

Corporate Bond Yield 24-Month Change:

Source: Bloomberg, EPB Macro Research

The corporate sector is far more levered today, with weaker margins and lower trend growth as compared to the prior three recessions.

Thus it remains possible that the decline in corporate bond prices was enough to trigger a downshift in employment growth, an effort to preserve margins.

Impact On The Real Economy

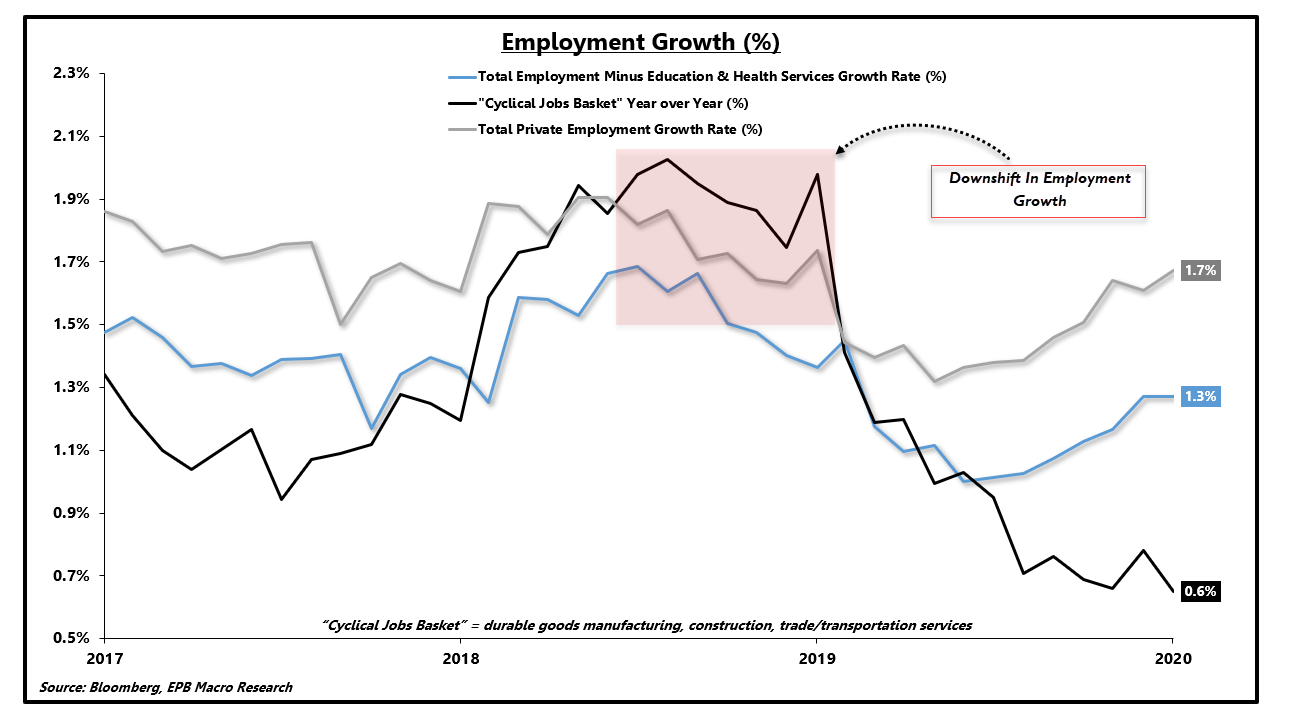

Cycles in employment can be monitored separately from cycles in growth. Geoffrey Moore tracked cycles in growth, inflation, and jobs independently.

Leading indicators of economic growth turned lower very early in 2018, some in late 2017. Inflation indicators did not plunge until September 2018, and jobs growth did not inflect lower until corporate bond yields spiked in late 2018.

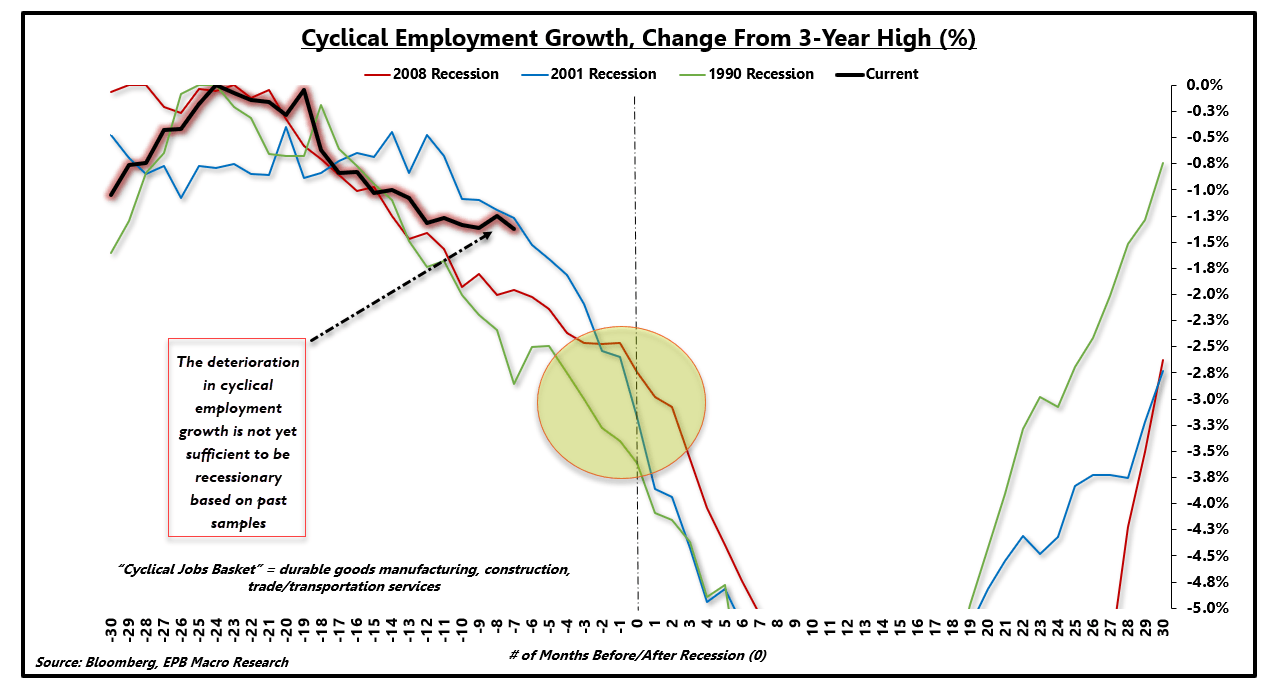

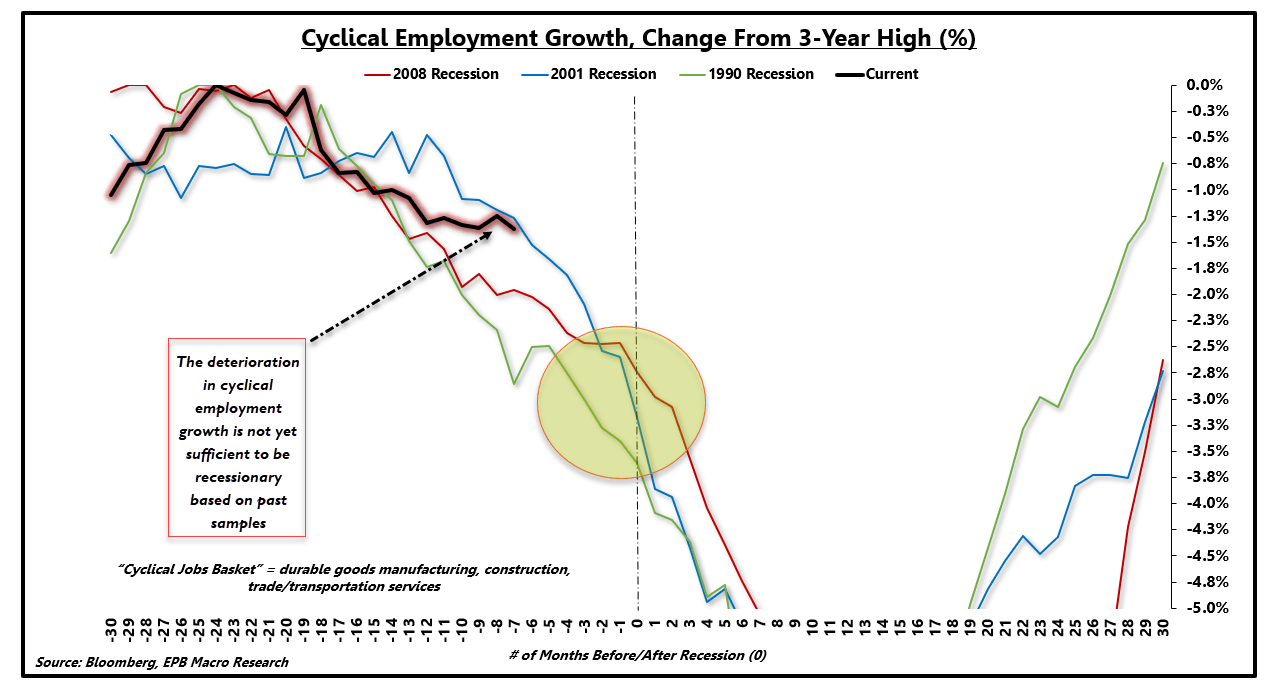

Cyclical employment, defined in the chart below as durable goods manufacturing, construction, and trade/transportation services, started to show rapidly-declining rates of growth.

Employment Growth Changed:

Source: Bloomberg, EPB Macro Research

If we track the change in cyclical employment growth before the three previous recessions, we can see recessionary periods begin with similar declines in cyclical employment.

Today’s current track of cyclical employment growth is currently insufficient to be recessionary based on past samples. However, if the trajectory does not flatten or inflect higher, history suggests that income and consumption growth will follow, leading to recessionary conditions.

Employment Growth Trend Relative To Past Samples:

Source: Bloomberg, EPB Macro Research

Employment growth over the next six months remains critical. If corporations continue to post weaker rates of employment growth or accelerate layoffs as a result of the Coronavirus outbreak, a recession is still firmly in play.

An existing trend of weaker growth and employment, originated by the Federal Reserve tightening cycle and deleveraging in China, exposed the economy to a negative shock.

It’s clear using the chart above how a negative shock (COVID-2019) coupled with an existing downturn in growth/employment can create a recession.

The Current Shock

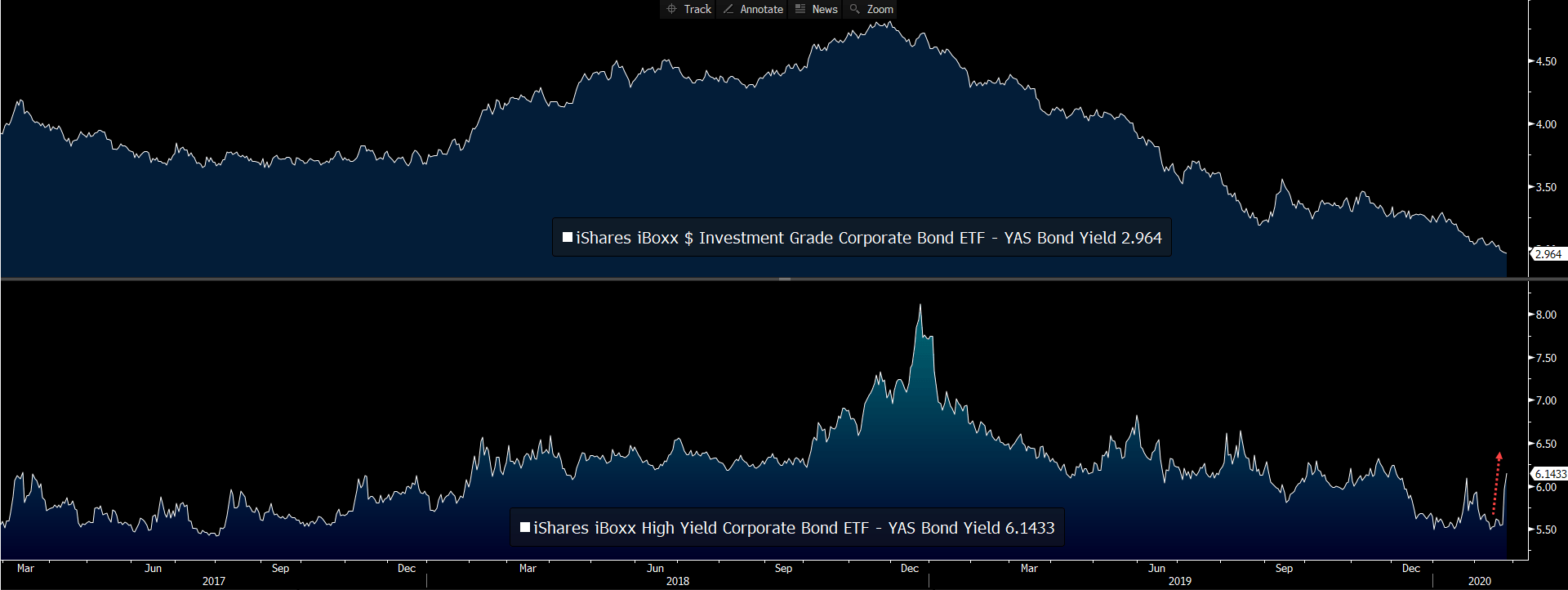

The current economic shock has resulted in a widening of corporate bond spreads. Using popular credit ETFs (LQD) and (HYG), we can track the implied spread above Treasury bonds. Both investment-grade and high-yield credit spreads, particularly high yield, have been widening materially in the past several weeks.

Investment-Grade / High-Yield Corporate Spreads:

Source: Bloomberg, EPB Macro Research

Luckily, however, corporate yields are a function of Treasury rates plus a spread.

For investment-grade bonds, Treasury rates are still declining faster than spreads are increasing, resulting in lower investment-grade bond yields.

High-yield bonds, however, are starting to see higher yields, a firm negative for corporate margins and future employment.

Investment-Grade / High-Yield Corporate Bond Yields:

Source: Bloomberg, EPB Macro Research

The current slowdown in employment growth, specifically cyclical employment growth, is severe and can be seen in many economic data points. If leading indicators of economic growth were turning higher, however, and cyclical employment growth started to increase, the economy may very well avoid a recession.

The negative shock of the Coronavirus has likely caused employment plans to freeze, irrespective of any increase in borrowing costs.

If the Coronavirus continues to cause a sell-off in risk assets and spreads start to widen faster than Treasury rates decline, corporations will be faced with higher borrowing costs at a time when economic growth was on shaky ground to being with.

Employment Growth Trend Relative To Past Samples:

Source: Bloomberg, EPB Macro Research

Should an increase in borrowing costs accelerate the decline in employment growth, and the black line in the chart above drifts into the yellow circle, a recession will be tough to avoid.

Clearly, a call for a recession is premature, and my economic outlook has zero forecasts concerning the virus or any predictions regarding a conclusion.

Rather, when constructing an allocation to weather a shock, we must be mindful of the current state of the economy and the susceptibility to a recession from a negative event.

Currently, a recession is not imminent based on the data above. Still, the situation can evolve quickly, and the economy is far from immune to a shock in its current state.

Keys To Watch and Outlook

The increase in corporate bond yields late in 2018 was small in relation to other recessionary periods. Still, given

- the level of corporate leverage,

- anemic profit growth, and

- weak economic conditions,

a smaller increase can have a more significant impact.

Employment growth has been in a downtrend since that late 2018 period, contributing to weaker rates of consumption growth seen in recent reports.

The economy is not imminently vulnerable to a recession, but that can change in a matter of weeks. The impact on employment is the key to watch when judging lasting recession risk.

Moving forward, if the current shock causes employment growth to suffer, already in a fragile state, recessionary conditions will be tough to avoid.

An acceleration in corporate layoffs will be exacerbated by higher borrowing costs, making credit spreads and bond prices a vital signal.

Given the susceptibility to a recession pending a worsening of conditions, investors should consider an added layer of protection should this negative shock take a turn for the worse.

If conditions worsen or simply do not improve for several weeks, a recession may be difficult to avoid, mainly due to the initial conditions before the shock began.

If the economy does tumble into a recession, risk assets are highly exposed, and a continued overweight allocation to Treasury bonds and gold will likely offer the best protection.

The model portfolio at EPB Macro Research continues to have an overweight exposure to Treasury bonds and gold.

Living In The Greatest Financial Bubble Of All Time

The US continues to defy all rational valuation metrics as it continues to make new highs. I contend this is the result of the huge amount of liquidity being provided to the markets by the FED. This bubble now appears to be entering its blow off phase. As I have said before, just because a market is overvalued does not earn it cannot become more overvalued.

Nevertheless, at some point the music will stop and a massive decline in the stock market will occur.Will the reduced economic activity caused by the coronavirus be the needle that pricks this bubble. So far the markets, with the exception of commodity markets, are shrugging off the news that China is basically on lockdown.

The German energy transition continues to fail as the country considers building more coal generation as energy rates soar and CO2 emission targets are not being met. A lesson for policy makers in the US to take into consideration.

Transcript

00:00hey guys John Paula me here actionable00:03intelligence00:04today is Sunday February 16 2020 this is00:09the weekly market update00:11so before right before I get into the00:14charts I just want to make some comments00:16on the continuing coronavirus situation00:20as it relates to what we’re doing when00:23it relates to in the markets and I’m a00:28little bit I don’t know00:31shocked not shocked but what’s the right00:34word confused we’re seeing all-time00:38highs last week and in many stocks in00:42the stock market and so you know it00:49makes you wonder what’s going on is the00:51market so efficient that its pricing and00:54the fact that this isn’t going to be a00:56big deal or is it more that I what I01:00think it is which is a liquidity bubble01:03plus all kinds of money coming into the01:06US for various reasons safe haven flows01:10if you will I think that’s probably an01:14explanation for why stocks are going up01:15there’s some stocks that are01:17inexplicably not going down which should01:20I’ll give some examples as we go and get01:23into the discussion what I want to say01:25though is is that I’m getting very very01:27concerned about the bubblicious01:29conditions we are at some of the highest01:31bubble levels that I’ve ever seen01:34now we’ve been talking about that for a01:36while and we’ve said that liquidity01:39flows matter you know the stock market01:42isn’t necessarily correlated with the01:44economy in the longer term it seems to01:47be but you know it’s liquidity matters01:50and with the QE for that that the Fed is01:55doing that the QE for non QE for01:58whatever they want to call it the repos02:00that’s high-powered money that’s t-bills02:03they’re buying this is the first time02:04they’ve done that in many years and that02:06money is going directly into the markets02:09couple that with the fact that you02:11already had dollar flows into the u.s.02:13prior to the coronavirus and now the02:16u.s. still being a safe haven that’s02:19where the money’s going so I would02:22caution you it what’s what’s fascinating02:25is is the the only thing that’s really02:27bad are commodities so the commodities02:30are showing us that you know demand is02:34obviously gonna have a knock-on effect02:36from this you know when you shut down02:39the Chinese economy basically you’re02:41gonna in some largest consumer of things02:43like oil largest importer of oil copper02:46aluminum cement things like this you’re02:51going to have a knock-on effect as China02:54basically everybody’s in quarantine and02:56Industry slows down we’ve also seen that02:58in the supply chains we’ve seen more03:01announcement this week we saw one03:03announcement where the company went back03:06to work and there was like a thousand or03:092,000 employees and what the employees03:11had coronavirus now everybody’s03:13quarantined to the factory they can’t03:14even go home so I don’t know I’m back to03:18what I’ve said before I don’t really03:20know what’s going on here do you trust03:23the data in China no if you look at the03:24John Hopkins tracker coronavirus tracker03:28they take in they don’t just take in one03:30bit of information they gather03:32information from several sources it03:33seems like things may be starting to03:36peak in China if you believe the data03:38which I want I don’t believe the data I03:41would say though that I think the rest03:46of the world cases are still going up03:48slightly they’re still under a thousand03:49cases it’s like 750 outside of China03:54most of them concentrated in the areas03:56directly around China so there’s 1504:00cases in the US for example so we’re not04:03seeing this big epidemic now there are04:06many commentators or people that I’ve04:08listened to that said that the next wave04:10is coming and this thing is going to04:11explode outwards I don’t really know04:13what I’m I’m not a you know happened04:15epithelium ologist04:17I don’t have not an expert on academics04:20epidemics outside my circle of04:22confidence we still have to look at04:23those it’s affecting the markets that04:25were involved with which is resource04:27markets04:27for in a large part so I would be very04:34cautious if I was basically one of the04:38things I’m recommending is you know I04:39mean I think we’re going to see some04:42interest rate cuts from the Federal04:43Reserve as the economic numbers have to04:47be affected by this they have to be I04:50mean you’re just not going to have this04:52kind of slowdown in China and not have04:54it have a have an effect on the rest of04:55the world so I expect that that means05:00higher bond prices probably especially05:02in the Treasury market that’s a good05:03place play to put money in a short term05:06cash is always good I have a lot of cash05:09I like gold still Gold’s in a bull05:12market I think with the accelerating05:14monetary malfeasance that continues05:16around the world especially in the US05:18and I think you know what’s gonna happen05:20in China I think gold is poised to go a05:23lot higher especially with the debt05:26levels in the US we’re gonna be hitting05:28trillion dollar deficits I wrote an05:30article this week that kind of pointed05:33out the fact that I believe this is the05:35first year when the Social Security05:37trust fund now goes into the red and is05:40now going to become an on budget item so05:42you’re gonna have to pay out of the05:46federal budget there’s the two hundred05:48billion dollars that you don’t have in05:50the Social Security trust fund and I’ve05:52written articles about that people can05:54go my my site and look at that so there05:57is no lockbox there is no thing nothing06:00to dip into it’s just a bunch of IOU use06:01that now come do so things are not06:05getting better they’re getting worse but06:08yet the markets move higher and higher06:10and higher because it’s all about06:11liquidity so you know if you look at the06:16Venezuelan and Zimbabwe stock markets06:19when they went into hyperinflations06:21that’s not what I’m suggesting is gonna06:22happen in the US I’m not suggesting the06:24hyperinflation but if you look at their06:25stock markets they crashed upwards06:27there’s people piled in the stocks who06:30tried to hold some type of value so like06:35I said all these bubbles and we’ve06:37talked about bubbles even since I’ve had06:38this channel we’ve went through two06:40bubbles the Bitcoin06:41bubble that was one of the first videos06:42I did was about Bitcoin being a bubble06:44it was it crashed people a lot of people06:47lost a lot of money06:48same thing with cannabis stocks we06:50talked about that that’s now crashed06:52people have lost a lot of money so you06:56know we’ve seen bubbles before here’s a07:02chart shows various bubbles what happens07:04they crash they don’t usually come back07:07for a while you see the this particular07:10person chose excuse us what as07:11disruptors it’s just the post great07:14financial crisis that induced bubble but07:17this is the greatest one of all and it’s07:19now gonna go it’s I now believe it’s07:21accelerating too far it’s blow off top07:22and this is something we suggested in07:24previous videos what happened I’ve07:25talked about this I’ve got a Cassandra07:29but I suggested that even though the07:33stock market was overvalued and it’s07:34been overvalued from a long time it can07:37get way more it can get way overvalued07:39you can get much more overvalued and it07:42probably will another chart here you can07:47see going back to 1991 this is the07:51build-up to y2k that was going to be the07:53you know computers were gonna lock up07:55the world was gonna end the Greenspan07:58Fed printed a bunch of money it led to08:01the tech bubble it blew off but what08:04happened this is the Nasdaq he crashed08:0690% then you had your great financial08:09crisis in here we’ve had nothing but08:11money printing since and now QE 4 if you08:14will and we are now accelerating to what08:16I think is the blow-off top in this US08:19stock market so you need to be you need08:24to be concerned you need to be08:26understand what’s happening now I don’tknow what’s gonna prick the bubble someI’m looking at my my indicators as Ilook at the high-yield debt market whichI think will be the first thing thatrolls over and it’s not there’s no feverthere there’s no issues there right now08:42that can change you know as we start you08:45know one of the things like forecasts08:47are thought what could happen was that08:50if we did go into a recession there’s a08:52lot of zombie companies about 25 to 3008:55percent08:55the companies out there that have junk08:57debt are zombie companies and they08:59cannot afford to have rates go up rates09:05won’t go up unless we have some huge09:07breakout inflation so what could happen09:10though is that the economy slows09:11massively because of this China thing09:13cash flows can be constricted and that09:16could force companies into a situation09:18where they do not have sufficient cash09:21flow to service their debt and then you09:23begin a cascading flow of waterfall09:27effect if you will of debt explosions09:32and and you know reorganizations so I09:35think that’s a possibility but my09:39original thesis was that this thing was09:41gonna rip and roar we were gonna have an09:43energy was going to drag the inflation09:45rate up I we were on that track and then09:48the coronavirus had you remember we had09:50WT I was over it was sixty two dollars a09:52barrel at the beginning of January and I09:56was forecasting higher oil prices09:58because of the lack of investment and10:00the slowdown in shale and I thought that10:02that might be what kicks inflation into10:05gear and forces the Fed to raise rates10:08but now with the coronavirus and the10:11collapse and commodity prices that’s10:14happened that particular pin has been10:17put back into the into the drawer so10:21this is really amazing though because if10:23you look here at what’s happening in our10:25stock market I mean you could this just10:27correlates perfectly with what happened10:29with that we whole repo QE for non QE10:33for is what I call it so liquidity10:36really does drive these markets whether10:39people can then me you know you10:40supercharge this what the fund flows10:42into the US as because of it being a10:45safe haven or considered a safe haven or10:47the least dirty shirt in the HAMP or10:50however you want to characterize it but10:52this is what we are seen and this is not10:55healthy this is not going to end well10:57folks this is not good we’re gonna see10:59this blow off and then we’re gonna see11:01and I don’t know what’s gonna happen on11:03the downside so let’s go back talk about11:07some China stuff11:08for a while here her the resource11:10markets you know so the Baltic Dry Index11:12you know 415 it’s been a decline since11:18mid-2009 teen as the world economy was11:20slowing down but then we’ve got this you11:23know really what’s happened since the11:25beginning of the year and this11:26coronavirus took off and this things11:28crashed by you know three quarters or11:33two-thirds this is that lows we haven’t11:36seen in a decade so or almost of the11:41lows of 2016 so anyway this is not good11:44this is an indication that you know iron11:47or various ore concentrates they’re not11:52flowing you know because China is11:55basically shut down you know we’ve11:57already seen China declare a force11:58majeure on some energy deliveries like12:00LNG deliveries not good but what I’m12:08showing you this for is because I’m not12:09seeing the knock-on effect the market so12:11really don’t seem to be pricing any of12:12this in and it’s kind of it’s very weird12:15the signal is not good there’s China12:19travel collapse this was the passenger12:21transport volumes in China during the12:23Lunar New Year you see that we are12:25downed on rail roadway and air travel12:30anywhere from sixty to eighty percent12:33almost it’s a complete collapse the12:35whole country’s in lockdown basically12:39what I want to talk about why is this12:41relevant I just picked this one company12:43because I’ve heard other people talking12:45about it and kind of piqued my interest12:46this is wind resorts that’s a casino12:48operator they have properties in Las12:52Vegas but they also have two casinos I12:54believe in Macau which is a another12:56small island off the coast of China12:59where they allow gambling a lot of13:01Chinese well ninety five percent I’m13:04sure 99 percent of the traffic there is13:06is to these casinos is from China13:13mainland China what I find fascinating13:16here is is that the two casinos I look13:19at some of the financials real quickly13:20for Wynn Resorts13:22and the casinos the two casinos in Macau13:29are shut down now they’re still making13:30payroll basically they’re not to just13:34keep the casinos in the current state13:37they are paying payroll the 12,00013:39employees is about 2.5 million a day13:41they have no revenue coming in I believe13:43these two casinos if I read it correctly13:45contribute 300 million dollars of EBIT13:48da to the two Wynn Resorts bottom line13:52last year I think a billion dollars in13:54sales if I’m not mistaken regardless13:58when you shut down a large portion I13:59mean you had a bit of a drop off14:00obviously I mean actually if you look at14:05the beginning of 2020 when this virus14:06took off this thing made all new time14:07highs and then it it kind of did pull14:09back but not like you would think I mean14:12it pulled back about you know 20 percent14:15and now it’s rallying again why is this14:17thing rallying when there’s you know two14:20of their major properties and their14:21major revenue generators I mean are not14:24you know in business they’re just14:27sitting there we have no idea when14:28they’re gonna reopen so well I like I14:31said there’s two things going on here14:33either the market is efficient and its14:35pricing and the information and the14:36coronavirus is gonna blow over in the14:38next you know a few weeks or month or14:41two and then we’re gonna be back to14:42business as usual that’s one option of14:45another option as the market is just not14:47getting this I mean the same thing14:48you’re seeing like some of these cruise14:49ship companies these things should be14:51crashing who is taking a cruise with you14:54know to cruise ships go around like you14:56know Typhoid ships that can’t even get14:58into various ports I know I’m15:00overdramatizing that one of the ships15:02can’t but one of the one of the ships I15:04think that’s in Japan they’re finally15:05taking off British and American15:07passengers the governments of the UK and15:10the United States are dealing with this15:12but you know this news is not good this15:16thing’s supposed supposedly is so very15:17early and yet people are still taking15:21cruises and the you know it’s not really15:24being reflected you think any stock15:25prices only stock prices it’s reading15:27reflected as the resource markets you15:30know gold and copper down you know15:33anywhere from 15 or that gold but what15:36copper or down anywhere from 15 to 2015:38percent the stocks are down 30% which is15:42what you would expect get priced in15:45because of the you know like I showed15:47you earlier China’s basically shut down15:48so I don’t know this is not making a lot15:51of sense this thing is either gonna blow15:53over or it’s just going to we don’t know15:55what’s gonna happen and I just think15:57that some of the reactions in this15:58market are just ridiculous and they16:01don’t make any sense it’s just I think16:04like I said liquidity driven and no16:08fundamentals are even being considered16:09so you got to be careful out there guys16:11this is not this is really not textbook16:15what’s going on here well like I said16:17I’m still I still like gold I think you16:20can’t go wrong at gold sir we already16:22knows was in a bull market if we’re16:24gonna see increased money or increased16:27currency units being put into16:29circulation then I think that that’s16:33going to manifest itself in a higher16:34gold price at some point continued16:37higher gold price we’re starting to see16:38earnings come out excuse me16:41cup sum up some of the gold companies16:43ones that I follow I’ll just give you16:47one that I like that I follow I don’t16:48have it in the portfolio but I like it16:50it’s a company called Caledonia mining16:52they have a mine a very very profitable16:55mine in Zimbabwe and yeah I know people16:59kind of scoff at that but the company17:00really is a performer and they really up17:02their guidance for this year next year17:06because just of the gold price and how17:10that leverage is translating with their17:12low costs and their increase in17:13production so you really you know with17:17lower fuel costs with the oil price down17:19that’s a major component of a lot of the17:20miners and that’s going to have a17:23knock-on effect also so it also depends17:26where you’re operate if you’re operating17:27in a country like Zimbabwe and your17:29costs are in Zimbabwe dollars which are17:31being depreciated by the government and17:33yet you’re selling your commodity for US17:35dollars that also helps quite a bit I17:40want to give some other things here17:42quickly us to create a uranium reserve17:46we saw the news it was all over the17:47tortoise Twittersphere you17:49twit it looks like that starting next17:55year the Trump administration put into17:58the budget to create a uranium reserve18:04if you will 150 million dollars a year18:06for the next ten years do I think that’s18:09a major market mover no but I think it’s18:13it’s part of the commitment the Trump18:14administration is making to uranium and18:17to nuclear power in the US I mean we are18:19totally behind everyone else I mean it’s18:22just ridiculous18:22I mean somewhere close to 20 percent of18:28our our power in the United States is18:32from nuclear power and we don’t even18:34mind 1% of our fuel and process it here18:37I mean that’s just a national security18:38issue not only that just based on our18:40nuclear Navy fleet so I think that if18:44the if Trump gets reelected he is18:48pro-nuclear I’m Pro nuclear I think this18:50is good for the country18:52we shouldn’t be relying on Russia and18:56causality z’ and for our uranium it’s19:02just not in our interest to do that we19:05also need to get you know I’ve always19:06been an advocate for this I’m gonna say19:08it again19:08you know if you really are into stem19:10which is science technology engineering19:11and math and you really want high wages19:14and you really want to deal with climate19:16change if you if you think that co2 is19:19the control knob for climate then why19:22not do something like build 100 nuclear19:25power plants in the next 10 years or 2019:27in 10 years or something like that19:28because these are high paying jobs and19:30long life construction projects very19:32technical even for the operations19:34personnel that work there you have to19:36have be very highly educated19:38these are high-paying jobs it would19:41create a infrastructure manufacturing19:45infrastructure based here in the US that19:46we could export and we’ve just left this19:49to the Chinese and Russians and that’s19:51just stupid because the Chinese and19:53Russians use their nuclear industry to19:58gain political footholds and countries20:00and to cozy up with him and they20:02run the thing fullcycle they’ll come in20:04engineering procure and construct then20:06operate then deal with the fuel supply20:09and the waste you just sit there and you20:11know charge for the electricity while20:13they run everything so that helps their20:16home industries that are involved in20:18this it helps them politically as they20:21go around the world and try to woo20:24various countries to their block so the20:31u.s. from any perspective you look at if20:34you are look at it from wages climate20:36change energy supply energy diversity20:40national security it just makes sense20:42and I think that you know a lot of20:46people make fun of Trump but I think he20:48does he spot-on on this so this isn’t a20:52game changer but it’s more you know more20:54wind in the sails and it certainly isn’t20:56going to hurt things now I want to bring20:59up some things this is gonna get me some21:01bad mail people don’t like this wanted21:04to talk about read some good articles21:06this week about the energy transition in21:09Germany’s fleet joke it’s it’s it’s big21:13problems I’ll put an article up had it21:17really pretty good vignettes in there I21:19mean basically you know here’s that21:20here’s a slide from the article this is21:22green Germany’s proposed coal plant21:25expansions you know you’ve got your yeah21:28just in the yellow that you’ve got for21:30these late-night mines21:31that’s that surface mining with that21:33cheap dirty coal of course you got the21:35other plant sees that these are plants21:37that are going to be built because solar21:41and wind are not getting that the energy21:43transitions not happening and the Merkel21:46regime there which is not going to be in21:48power much longer I don’t think well is21:52you know did a snap judgment on shutting21:56down or phasing out and shutting down21:59the German nuclear fleet which is in22:02progress so you have to get power from22:04somewhere so now you have a situation22:06where Germany is now suffering power22:08rates are some of the highest in the in22:10Europe German industry is suffering22:14people are suffering because they don’t22:16have there’s poor people there that22:17don’t have enough money to pay there’s a22:20link to an article in the article that22:23I’m going to link to where people are22:24shifting to wood stoves and they’re22:26sneaking out into the woods and chopping22:28down wood illegally I mean it’s it’s not22:32working it’s not gonna work and I think22:34that you know just in the article the22:36one article there’s linked to and22:38they’re you know it gave it vignette of22:40you know Merkel just as just does things22:43on a snap judgment she’s a consummate22:45grubby politician and with her finger in22:49the wind so you know with the Greens22:51party making inroads in Germany she’s22:55counting to it but the problem is is22:57that you know it’s hurting business and22:59industry and jobs and most people23:02there’s a lot of people that don’t care23:04about that that green a lot of people in23:07the green movement could care less they23:09want deindustrialization they want you23:12know they tie everything into socialism23:14and equality and to you know however23:17they define it rights of different23:20indigenous peoples all this thing is23:22just tied into one big goulash that they23:24create and they’re in their philosophy23:26and they could care less23:27but the majority of people do care the23:30majority of people do not want to see23:33their standard of living go down the23:34majority of people want a better you23:39know standard of living and I believe23:41that you’re going to see a big upheaval23:43in German politics culminating with a23:45reversal I think of the nuclear band and23:50I think Germany may even start building23:52nuclear plants23:53I mean I’ve put up article after article23:55you can’t even build a new wind farms in23:57Germany the opposition out in the23:59hinterlands and farms and rural areas is24:03just too high they will not allow it and24:05especially the East Germans East Germans24:07have had enough of this they they see24:10right through it and that’s why you’re24:13seeing AF D alternative for Deutschland24:16make inroads in some of the recent24:18elections and you’ve also seen you know24:21this this has led to the Christian24:24Democratic Union Merkel’s24:27Hera parents she actually resigned24:29because of something that just happened24:31in one of the states German states in24:34East Germany one of the CDU person that24:38was elected got elected with the support24:40of the AFD in a coalition and that was24:44determined to be racist and all that24:45stuff to say FD supposedly is right-wing24:47and so this governor resigned and that24:51reflected back on the Hera parents so24:53there’s a lot of upheaval coming in24:55Europe that’s a whole nother video just24:59about you know the EU is on its way out25:02this is not sustainable25:04there’s too many competing agendas and25:07it’s just not going to last and breaks25:11it is the beginning the populist revolt25:13whether it’s populism coming from the25:14left or the right25:15it will continue around the world the25:20other thing to point out and the article25:22which I thought was interesting or I got25:24this from somebody else I can’t remember25:26here are the emissions of co2 in Germany25:29I believe 2009 was the year they started25:32the energy transition and I somewhere25:35around here I can’t remember I have to25:36look it up the energy and I can’t25:40pronounce it so they long german word25:41that means energy transition basically25:43the solar and wind but you see there’s25:46really not been no decline and that25:48emissions of co2 in germany you know if25:51you wanted to get this down you get your25:54nuclear fleet back and you get rid of25:56all those coal plants and why are you25:58going to build more coal plants that26:02does say in the article though that26:03because these are supercritical boilers26:06supercritical blowers are boilers that26:07run at like 3000 psi coal-fired they26:11actually have 30% reduced emissions of26:14co2 but you’re still going to be pumping26:16out a lot of co2 and this number is not26:19gonna get better so something to watch26:23you know like I said I’ve said this26:25before you know Germany is a real-life26:26Laboratory of a major industrial country26:29that has attempted and we can argue in26:33state if actually that is still trying26:36to attempt to do an energy transition26:38from fossil fuels to26:40it’s simply you see what happens it’s26:43not working it cost a lot of money power26:46rates go up and you know what your net26:48co2 doesn’t go down26:49that’s like I’ve said before there’s a26:51reason why we use Coal Fired there’s a26:53reason why we use nuclear power because26:55large base load generation is cheap and26:58reliable that’s why we use it you’re not27:01going to play solar panels into Baltic a27:04lot of the Baltic Sea where you know and27:06it does the Sun doesn’t shine that often27:08that’s just I mean the certain areas27:10it’s not Arizona or Texas where the Sun27:14shines all the time or Florida or27:15Southern California this is Germany for27:17heaven’s sakes northern Europe but you27:20can’t explain to some people I want to27:23point out another thing saw an article27:26shale pioneer John Hass heading off27:28Shores Hess production Hess oil from the27:35article production of the Eagle Ford27:37Shale in South Texas is starting to27:39plateau while the bat Bakken field North27:41Dakota where Hess as a major producer27:43will hit its peak production levels27:45within the next two years this is a27:47speech that our presentation has gave at27:50a recent oil conference the Permian27:53Basin the top US shale field in Texas27:55and New Mexico will plateau plateau in27:58mid decade and is already facing well28:00interference issues has said so has John28:05Hess plans to use cash flow their Hess28:07company it’s a big very big oil company28:10plans to use cash flow from the Bakken28:11to invest in longer-term offshore28:13investments the company is relied on28:15offshore Guiana one of the world’s most28:18important oil and gas discoveries in the28:19last decade so just another piece of28:23information piece of the puzzle you know28:27I really about shale peaking and shale28:32accounted for 98 percent of the oil that28:37met the demand increases over the last28:39you know five six years in the world you28:43know oil demand goes up a million28:45barrels to a million point one point28:47five million barrels a day every year28:49increases by one to 11.5% every year28:53and that increase has been met by the28:55increases in shale production it’s been28:58huge28:58so non-opec conventional oil has not29:03been invested in it’s not been a29:05contributor and OPEC is just sitting29:08there we don’t you know it’s it’s the29:10call on OPEC has not been to increased29:12production so I think what’s going to29:15happen if things stay correct and we see29:18this decline in growth and shale which29:23is happening if it stays consistent if29:27in fact we are at the top and this29:29thing’s rolling over which I believe it29:31is that being shale the cup there’s not29:38that enough investment main offshore29:39that’s been my thesis and that’s where29:41people that’s where the money’s gonna go29:42now the problem is is with this29:44coronavirus it kind of short-circuited29:46the recovery in oil prices we don’t29:49really know we have to watch inventory29:51levels things are very chaotic right now29:53we don’t have enough information we29:55don’t know where this is going to end29:57but you know looking out three to five30:00years I hate to say that because you30:02know it’s like you just keep saying that30:04every year another three years and30:05people just aren’t going to wait that30:07long I get it but you know if you look30:10at the Reserve life indexes of major oil30:12companies if you look at the investment30:15dollars that have went into oil30:17exploration it’s not been enough to30:19sustain production and the penetration30:22of electric vehicles is not going to be30:24sufficient in the timeframe that’s30:25necessary to create demand destruction30:30and oil I mean in fact electric vehicle30:33sales were down last year they weren’t30:35up so that should tell people something30:39I think oils gonna be around for a lot30:41longer and once we get to this30:43coronavirus which has really been a30:45septic shock to the oil and commodity30:49markets we’ll have to see what happens30:50as we come out of this but I think as30:54this thing gets back on plane and we can30:55see real data it’s gonna become more and30:57more obvious what’s happening that the31:00call on non-opec a conventional supplies31:04will not be able to be met because the31:06lack of investment31:07and then we’ll see if OPEC has the31:09weather with all or has the ability to31:11increase production regardless these are31:15extractive industries and if you don’t31:17invest enough money in replacing your31:20reserves you eventually go out of31:21business I mean I’ve said that over and31:23over and over and that’s really where31:24we’re at so a lot of information there31:28guys that’s it for this week31:31appreciate the support appreciate the31:32viewership you guys are the inspiration31:36to why I do this more people keep31:38subscribing I thank you a lot it means a31:42lot to me and keep on sharing keep on31:46liking the videos it really helps out31:48enjoy the comments switching to a less31:52stressful career so I probably should31:54have more time and I’m hoping to make31:57some changes get some more interviews31:58but we’ll see how things happen over the32:00next coming months that’s it for this32:02week guys thanks a lot and we’ll talk to32:04you next week