In yesterday’s post, I began to tell the tale of how the USA planned and implemented a Global Plan for the world economy, placing the US administration at the heart of a global Surplus Recycling Mechanism. Today, I have two offerings: One is a brilliant paper by George Krimpas which states the case for such a Surplus Recycling Mechanism, as expounded by Keynes during the Bretton Woods conference in 1944. It is called The Recycling Problem in a Currency Union. Secondly, I am continuing today my own story of how the postwar Global Plan unravelled, giving rise to a brand new, terriblyunruly, yet puzzlingly effective Surplus Recycling Mechanism which I call the Global Minotaur (1971-2008). It comes from Chapter 4 of my forthcoming book (also entitled THE GLOBAL MINOTAUR). Enjoy. (As I am about to board a plane for Australia, and then Korea, my postings will be intermittent for a while.)The Global Plan’s Achilles HeelThe Global Plan unravelled because of a major design flaw in its original architecture. John Maynard Keynes had spotted the flaw during the 1944 Bretton Woods conference but was overruled by the Americans. What was it? It was the lack of any automated Global Surplus Recycling Mechanism (GSRM) that would keep systematic trade imbalances constantly in check.

The American side vetoed Keynes’ proposed mechanism, the International Currency Union (ICU), thinking that the US could, and should, manage the global flow of trade and capital itself; without committing to some formal, automated GSRM. The new hegemon, blinded by its newfangled superpower status, failed to recognise the wisdom of Ulysses’ strategy; of binding itself voluntarily to some Homeric mast.

Less cryptically, Washington thought that global trade imbalances would favour America in perpetuity, casting in stone the its economy’s status as the world’s surplus nation. Then, the power bestowed upon the United States by the surpluses it extracted from all over the world would be utilised benevolently and efficiently in order to manage the world economy along the lines of an enlightened hegemony. Indeed, this is exactly what the United States did: They recycled graciously the American surpluses in the form of capital injections into Japan, Germany and other deserving regions.

Alas, US policy makers failed to foresee that global imbalances could undergo a drastic inversion, leaving the United States in the unfamiliar position of a deficit country. During the heady days of the late 1940s, the Global Plan‘s architects ostensibly neglected to take seriously the possibility that the lack of self-restraint would lead Washington to codes of behaviour that would undermine their brilliant grand design.

The Global Plan unravels

The Global Plan‘s path was not laid with roses. A series of mishaps marked its evolution, with Chairman Mao’s triumph delivering the first blow. Quite impressively, it reacted creatively to adversity, often as a result of unintended consequences. We have already seen how the Korean War was exploited to shore up the GlobalPlan‘s far eastern flank. So, when the United States dragged itself into the Vietnam War, a similar wave of ‘creative destruction’ was on the cards.

Though it is a gross understatement to suggest that its persecution did not go according to the original plan, the Vietnam War‘s silver lining is visible to anyone who has ever visited South East Asia. Korea, Thailand, Malaysia and Singapore grew fast and in a manner that frustrated the pessimism of those who predicted that underdeveloped nations would find it hard to embark upon the road of capital accumulation necessary to drive them out of abject poverty. In the process, they provided Japan with valuable trade and investment opportunities which lessened the burden on the US authorities which, before the mid-1960s, had shouldered alone the burden of generating enough demand for Japanese factories in Europe and in the US itself. Years later, the same model was copied by Deng Xiao Ping and delivered the China we know today.

The problem with unintended consequences is that they are not reliably advantageous. Ho Chi Minh’s stubborn refusal to lose the war, and Lyndon Johnson’s almost manic commitment to do all it takes to win it, were crucial not only in creating a new capitalist region in the Far East, but also in derailing the Global Plan. The escalation of the financial costs of that war that were to be a key factor in its demise.

Setting aside the appalling human cost,[1] the war cost the US government around $113 billion and the US economy another $220 billion. Real US corporate profits declined by 17% while, during the period 1965-1970, the war-induced increases in average prices forced the real average income of American blue collar workers to fall by about 2%.[2] The war was taking its toll not only ethically and politically, as a whole generation of American youngsters were marked by the fear and loathing of Vietnam, but also in terms of tangible loss of working class income which fuelled social tensions. Arguably, President Johnson’s Great Society social programs were aimed, largely, at relieving these strains.

As the combined costs of the Vietnam War and the Great Society began to mount, the government was forced to generate mountains of US government debt. By the end of the 1960s, many governments began to worry that their own position, which was interlocked with the dollar in the context of the Bretton Woods system, was being undermined. By early 1971, liabilities in dollars exceeded $70 billion when the US government possessed only $12 billion of gold with which to back them up.

The increasing quantity of dollars was flooding world markets, giving rise to inflationary pressures in places like France and Britain. European governments were forced to increase the quantity of their own currencies in order to keep their exchange rate with the dollar constant, as stipulated by the Bretton Woods system. This is the basis for the European charge against the United States that, by pursuing the Vietnam War, it was exporting inflation to the rest of the world.

Beyond mere inflationary concerns, the Europeans and the Japanese feared that the build-up of dollars, against the backdrop of a constant US gold stock, might spark off a run on the dollar which might then force the United States to drop its standing commitment to swapping an ounce of gold for $35, in which case their stored dollars would devalue, eating into their national ‘savings’.

The flaw in the Global Plan was intimately connected to what Valery Giscard d’Estaing, President de Gaulle’s finance minister at the time, called the dollar’s exorbitant privilege: The United States’ unique privilege to print money at will without any global institutionalised constraints. De Gaulle and other European allies (plus various governments of oil producing countries whose oil exports were denominated in dollars) accused the Unites States of building its imperial reach on borrowed money that undermined their countries’ prospects. What they failed to add was that the whole point of the Global Plan was to revolve around a surplus generating United States. When America turned into a deficit nation, the Global Plan could not avoid going into a vicious tail spin.

On 29th November 1967, the British government devalued the pound sterling by 14%, well outside the Bretton Woods 1% limit, triggering a crisis and forcing the United States government to use up to 20% of its entire gold reserves to defend the $35 per ounce of gold peg. On 16th March 1968, representatives of the G7’s Central Banks met to hammer out a compromise. They came to a curious agreement which, on the one hand, retained the official peg of $35 an ounce while, on the other hand, left room for speculators to trade gold at market prices.

When Richard Nixon won the US Presidency in 1970, he appointed Paul Volcker as Undersecretary of the Treasury for International Monetary Affairs. His brief was to report to the National Security Council, headed by Henry Kissinger, who was to become a most influential Secretary of State in 1973. In May of 1971, the taskforce headed by Volcker at the Treasury presented Kissinger with a contingency plan which toyed with the idea of “suspension of gold convertibility”. It is now clear that, on both sides of the Atlantic, policy makers were jostling for position anticipating a major change in the Global Plan.

In August of 1971 the French government decided to make a very public statement of its annoyance at the United States’ policies: President George Pompidou ordered a destroyer to sail to New Jersey to redeem US dollars for gold held at Fort Knox, as was his right under Bretton Woods! A few days later, the British government of Edward Heath issued a similar request, though without employing the Royal Navy, demanding gold equivalent to $3 billion held by the Bank of England. Poor, luckless Pompidou and Heath: They had rushed in where angels fear to tread!

President Nixon was absolutely livid. Four days later, on 15th August 1971, he announced the effective end of Bretton Woods: the dollar would no longer be convertible to gold. Thus, the Global Plan unravelled.

Interregnum: The 1970s oil crises, stagflation and the rise of interest rates

Soon after, Nixon dispatched his Secretary of the Treasury (a no non-sense Texan called John Connally) to Europe with a sharp message. Connally’s account of what he said to the Europeans was mild and affable:

“We told them”, he told reporters, “that we were here as a nation that had given much of our resources and our material resources and otherwise to the World to the point where frankly we were now running a deficit and have been for twenty years and it had drained our reserves and drained our resources to the point where we could no longer do it and frankly we were in trouble and we were coming to our friends to ask for help as they have so many times in the past come to us to ask for help when they were in trouble. That is in essence what we told them.”

His real message is still ringing in European ears: It’s our currency but it’s your problem! What Connally meant was that, as the dollar was the reserve currency, i.e.the only truly global means of exchange, the end of Bretton Woods was not America’s problem. The Global Plan was, of course, designed and implemented to be in the interest of the United States. But once the pressures on it (caused by Vietnam and internal US tensions that required an increase in domestic government spending) became such that the system reached breaking point, the greatest loser would not be the United States itself but Europe and Japan; the two economic zones that had benefited mostly from the Global Plan.

It was not a message either the Europeans or Japan wanted to hear. Lacking an alternative to the dollar, they knew that their economies would hit a major bump as soon as the dollar would start devaluing. Not only would their dollar assets lose value but, additionally, their exports would become dearer. The only alternative was for them to devalue their currencies too but that would then cause their energy costs to skyrocket (given that oil was denominated in dollars). In short, Japan and the Europeans found themselves between a rock and a hard place.

Toward the end of 1971, in December, Presidents Nixon and Pompidou met in the Azores. Pompidou, eating humble pie over his destroyer antics, pleaded with Nixon to reconstitute the Bretton Woods system, on the basis of fresh fixed exchange rates that would reflect the new ‘realities’. Nixon was unmoved. The Global Plan was dead and buried and a new unruly beast, the Global Minotaur, was to fill its place.

Once the fixed exchange rates of the Bretton Woods system collapsed, all prices and rates broke loose. Gold was the first commodity discretely to jump from $35 to $38 per ounce, soon to $42 and then to float unbounded into the ether. By May 1973 it was trading at more than $90 and before the decade was out, in 1979, it had reached a fabulous $455 per ounce; a twelvefold increase in less than a decade.

Meanwhile, within two years of Nixon’s August 1971 bold move, the dollar had lost 30% of its valuevis-à-vis the Deutschmark and 20% against the Yen and Frank. Oil producers suddenly found that their black gold, when denominated in yellow gold, was worth a fraction of what it used to be. Members of the Organisation of Petroleum Exporting Countries (OPEC), which regulated the price of oil through agreed cutbacks on aggregate oil output, were soon clamouring for coordinated action (i.e. reductions in production) to boost the black liquid’s gold value.

At the time of Nixon’s announcement, the price of oil was less than $3 per barrel. In 1973, with the Yom Kippur war between Israel and its Arab neighbours apace, the price jumped to between $8 and $9, thereafter hovering in the $12 to $15 range until 1979. In 1979 a new upward surge began that saw oil trade above $30 well into the 1980s. And it was not just the price of oil that scaled unprecedented heights. All primary commodities shot up in price simultaneously: Bauxite (165%), lead (170%), silver (1065%) and tin (220%) are just a few examples. In short, the termination of the Global Plan signalled a mighty rise in the costs of production across the world. Inflation soared as did unemployment: a rare combination of stagnation with inflation that came to be known as stagflation.

The conventional wisdom of what caused the 1970s stagflation is that the OPEC countries pushed the dollar price of oil sky high against the will of the United States. It is an explanation that runs against logic and evidence. For if the Nixon administration had truly opposed the oil hikes, how are we to explain the fact that its closest allies, the Shah of Iran, President Suharto of Indonesia and the Venezuelan government, not only backed the increases but led the campaign to bring them about? How are we to account for the administration’s scuttling of the Tehran negotiations between the oil companies (the so-called Seven Sisters) and OPEC just before an agreement was reached that would have depressed prices?

Quoting an influential American observer of these crucial discussions, “…a split was announced in the talks in Tehran by a special US envoy, then-Under Secretary of State John Irwin, accompanied there by James Akins, a key State Department man on oil….[T]he real lesson of the split in negotiations with OPEC was that higher prices were not terribly worrisome to representatives of the State Department… the whole subject of what the negotiations were about began to focus not on holding the price line but on ensuring security of supply.”[3]

The question is thus begged: Why did the United States not oppose with any degree of real commitment the large increases in oil prices? The simple reason is that the Nixon administration, just like it did not regret the end of Bretton Woods, did not care to prevent OPEC from pushing the price of oil higher. For these hikes were not inconsistent with the administration’s very own plans for a substantial increase in the global prices of energy and primary commodities!

Recalling that the new aim was to find ways of financing the US twin deficits without cutting US government spending, or increasing taxes, or reducing US world dominance, American policymakers understood that they had a simple task: To entice the rest of the world to finance its deficits. But this meant a redistribution of global surpluses in favour of the United States and at the expense of the two economic zones they had built around Germany and Japan. Two were the prerequisites of the planned reversal of global capital flows which would see the world’s capital stream into Wall Street for the purposes of financing the expanding US twin deficits:

A. Improved competitiveness of US firms in relation to their German and Japanese competitors; and

B. Interest rates that attracted large capital flows into the Unites States

Prerequisite A could be achieved in one of two ways: Either by boosting productivity in the United States or by boosting the relative unit costs of the competition. The US administration decided to aim for both, for good measure. Labour costs were squeezed with enthusiasm and, at the same time, oil prices were ‘encouraged’ to rise. The drop in US labour costs not only boosted the competitiveness of American companies but, also, acted as a magnet for foreign capital that was searching for profitable ventures. Meanwhile, as oil prices rose, every part of the capitalist world was affected adversely. However, Japan and Western Europe (lacking their own oil) were burdened much more than the United States.

Meanwhile, the rise in oil prices led to mountainous rents piling up in bank accounts from Saudi Arabia to Indonesia, as well as huge receipts by US oil companies. All these petro-dollars soon found their way into Wall Street’s hospitable bosom. The Fed’s interest rate policy was to prove particularly helpful in this respect.

Turning to Prerequisite B, money (or nominal) interest rates jumped from 6%, were the Global Plan‘s final years had left them, to 6.44% in 1973 and to 7.83% the following year. By 1979 President Carter’s administration began to attack US inflation with panache. It appointed Paul Volcker as Fed Chairman with instructions to deal decisively with inflation. His first move was to push average interest rates to 11%.

In the following year, June of 1981 to be precise, Volcker raised interest rates to a lofty 20%, and then further up again to 21.5%. While his brutal monetary policy did tame inflation (pushing it down from 13.5% in 1981 to 3.2% two years later), its harmful effects on employment and capital accumulation were profound, both domestically and internationally. Nevertheless, Prerequisites A&B had been met even before Ronald Reagan had settled in properly at the White House.

A new phase thus began. The United States could now run an increasing trade deficit with impunity while the new Reagan administration could also finance its tremendously expanded defence budget and its gigantic tax cuts for the richest Americans. The 1980s ideology of supply-side economics, the fabled trickle-down effect, the reckless tax cuts, the dominance of greed as a form of virtue etc. were just manifestations of America’s new exorbitant privilege: the opportunity to expand its twin deficits almost without limit, courtesy of the capital inflows from the rest of the world. American hegemony had taken a new turn. The reign of the Global Minotaur had dawned.

The Global Minotaur

The United States had neither wanted nor resigned easily to the collapse of the Global Plan. However, once America lost its surplus position, US policymakers were quick to read the writing on the wall: the Global Plan‘s Achilles’ Heel had been pierced and its downfall was a matter of time. They then moved on very rapidly, unwilling to countenance the prospect of jeopardising global hegemony in a futile attempt to mend a broken design.

Perhaps the best narrative on the violent abandonment of the Global Plan comes from the horse’s mouth. In 1978 Paul Volcker, the man who was among the first to recommend that Bretton Woods be discarded, addressed an audience of students and staff at Warwick University. Not long after that speech, President Carter appointed him to the Chair of the Fed. One wonders if his audience grasped the significance of his words:

“It is tempting to look at the market as an impartial arbiter… But balancing the requirements of a stable international system against the desirability of retaining freedom of action for national policy, a number of countries, including the US, opted for the latter …”

And as if this were not sufficiently loud and clear, Volcker added the following:

“[A] controlled disintegration in the world economy is a legitimate objective for the 1980s.” (the emphasis is mine)

It was the Global Plan‘s best epitaph and the clearest exposition of the second post-war phase that was dawning. Volcker’s speech was a blunt proclamation of the future that US authorities envisaged: Unable to maintain reasonably well balanced international financial and trade flows any longer, America was planning for a world of rapidly accelerating asymmetrical financial and trade flows. The aim? To afford America the exorbitant privilege of running up boundless deficits and, thus, to entrench further US hegemony (not despite, but) courtesy of its deficit position. And how would such a feat be accomplished? The answer Volcker gave, with his usual bluntness, was: By choosing to fling the world economy into a chaotic, yet strangely controlled, flux; into the labyrinth of the Global Minotaur.

In the decades that followed, the days when the United States would be financing (directly, through war financing, or by the exercise of political power) Germany and Japan became a distant memory. America began importing like there was no tomorrow and its government splurged out unhindered by the fear of increasing deficits. As long as foreign investors sent billions of dollars every day to Wall Street, quite voluntarily and for reasons completely related to their bottom line, the United States’ twin deficits were financed and the world kept revolving haphazardly around its axis.

The Athenians’ gruesome tributes to the Cretan Minotaur were imposed by King Minos’ military might. In contrast, the tributes of capital that fed the Global Minotaur flooded into the United States voluntarily. Why? How did US policy makers persuade capitalists from all over the world to fund the superpower’s twin deficits? What was in it for them? The answer turns on four factors. To stick to the mythological narrative, let’s call them the Minotaur‘s charismas.

I shall be returning to these four charismas in my next posting.

[1] 2.3 million dead, 3.5 million seriously wounded, 14.5 million refugees.

[2] These estimates are due to New Deal economist Robert Eisner, Professor at Northwestern University and a one-time President of the American Economic Association.

[3] V.H. Oppenheim, V.H. (1976-77), ‘Why Oil Prices Go Up: We Pushed Them’, Foreign Policy, 25, 32-33

Amidst renewed calls for replacing the post-war Bretton Woods order, we take the opinion this has already occurred with the creation of bitcoin. Today’s HODLR’s might be tomorrow’s (de)central bankers.

Any escalation of political instability in the US would threaten the status of the US dollar as the global reserve currency. This hypothetical scenario would be an absolute disaster.

We are considering buying the dip here. Bitcoin’s critical mass should enable it to overcome its technical inferiority to less popular cryptocurrencies. It’s not going away.

Photo by peterschreiber.media/iStock via Getty Images

From Bretton Woods to Bitcoin

Crypto is decentralizing AI is centralizing… or if you want to frame it,you know, more ideologically… You could say that crypto is libertarian and AI is communist.

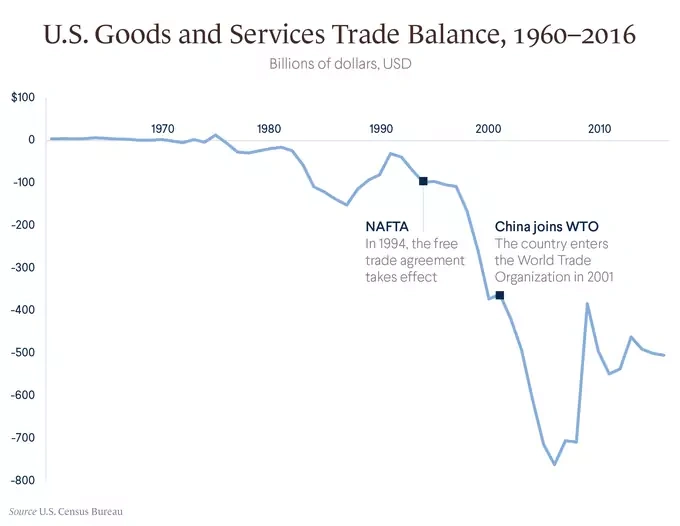

In the Summer of 1944, a group of 730 delegates from 44 nations met at the Mount Washington Hotel in Bretton Woods, New Hampshire. These delegates, which included famous economists such as John Maynard Keynes, created a new post-war financial order known as the Bretton Woods System. This agreement set the course for the system that we have today.

In addition to the creation of the International Bank for Reconstruction and Development (predecessor to the World Bank) and the IMF, one of the outcomes of the Bretton Woods conference was the rise of the US dollar as the global reserve currency. To ensure that countries wouldn’t competitively devalue their currencies and create a race-to-the-bottom, exchange rates of various currencies were pegged to the US dollar. The US Dollar was fixed to gold at $35/ounce, thus making it “as good as gold“.

By the late 1960’s the US spending to fund both the space race and the Vietnam war simultaneously. Demands by foreign governments to convert their US dollars into gold began to rise. This led to the “temporary” suspension of the ability to convert the US Dollar into gold in 1971, an action taken by Richard Nixon. Half a century later, conversion is still suspended. This has led to all sorts of economic consequences that are not really understood, which have been catalogued in the wtfhappenedin1971.com website.

The next big shakeup came in 2008 and 2009. In the aftermath of the financial crisis, two things happened. Countries began suggesting the creation of a new system that would replace the US dollar as the reserve currency. This included Russia, which advocated for “united future world currency” baring the slogan “unity in diversity“. The idea of abandoning the dollar was further backed by a U.N. report.

The second thing that happened was the creation of bitcoin. A group of renegade cryptographers and programmers known as the “cypherpunks” wanted to create an alternative to government-backed fiat currency. Their creation is now being rapidly adopted by a young generation that sees themselves as “global citizens” first and foremost, before that of any particular nationality. For them, the WiFi password was the passport for e-citizenship.

Characteristics of disruptive businesses, at least in their initial stages, can include: lower gross margins, smaller target markets, and simpler products and services that may not appear as attractive as existing solutions when compared against traditional performance metrics. Because these lower tiers of the market offer lower gross margins, they are unattractive to other firms moving upward in the market, creating space at the bottom of the market for new disruptive competitors to emerge.

Though bitcoin and central banks are not necessarily businesses, the dynamic sounds a lot like the cycle of disruptive innovation. Bitcoin started out as a peer-to-peer payment network on the fringe of the internet. A little over a decade later, and bitcoin is moving into the mainstream.

…because the FinTech revolution questions the two forms of money that we just discussed, coins and commercial bank deposit. And it questions the role of the state in providing money.

We are at a historic turning point. You–young or not so young–doesn’t matter. But bold entrepreneurs gathered here today, You are not just inventing new services. You are reinventing the history of money. You drawing a completely new future actually, and we are all in the process of adapting.

A new wind is blowing and it is that of digitalization… …and this is key: Money itself is changing. We expect it to become more convenient, more user friendly. Perhaps even less serious-looking. We expect it to be integrated with social media, readily available for online. And person-to-person use including micro payments. And of course we expect it tobe cheap, safe, protected against criminals and prying eyes.

So what role will remain for cash in this digital world… …even crypto currencies such as bitcoin a theorem and ripple are vying for a spot in the cashless world, constantly reinventing themselves in the hope of offering more stable value and quicker and cheaper settlement.

…. Let me be more specific. Should central banks issue a new digital form of money? A state bank token or perhaps an account held directly at the central bank and available to people and firms for retail payments to each of you…. ….this is not science fiction there are central banks around the world that are considering this option…

Central bankers probably aren’t meeting in secret about bitcoin and other cryptocurrencies to crack jokes about them. As stated by Christine Lagarde, now President of the European Central Bank, various central banks are already exploring the potential for their own “state bank tokens”.Bitcoin already has dominant market share, and a first-mover advantage.

Bitcoin’s current market cap is approximately $645B, much larger than the digital yuan. But how could ever scale to the point where it plays a major role in our system?

Bitcoin is hardcoded with 8 decimal places, with one 0.00000001 unit known as a Satoshi. If the exchange rate between the USD and BTC were $1M/1BTC each Satoshi would be worth 1¢. The market cap would be approximately $19T, based solely on today’s circulating supply.

Some will point out the fact that there are other coins based on better encryption techniques. Many of them are superior to bitcoin in various technical aspects. Yet bitcoin has one particular advantage, critical mass. It is the most popular coin, and thus it has the greatest network effect. Bitcoin miners also have the ability to update and upgrade the bitcoin protocol. This capability will help tackle future challenges such as quantum computers hypothetically capable of cracking bitcoin’s algorithm.

Bitcoin may never be as easy to use as a transactional currency, but it is quite plausible as a reserve asset. In essence, it is the first truly global form of currency. Though adopters of bitcoin transact in their local currencies when they buy everyday items, their bitcoin holdings are universal across the globe. It’s all one mutually agreed upon blockchain, a distributed record of what each individual has.

The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve.

This is how bitcoin can become the new reserve currency. Perhaps bitcoin is the reserve currency of the people, as the original intent for bitcoin was to be an alternative fiat currency issued by central banks, founded during the Occupy Wall Street movement… A movement that has conveniently faded away in favor of topics in social justice.

Perhaps today’s miners and holders of Bitcoin will become tomorrow’s central bankers, at least in theory. The world’s decentralized central bank. Again, the true power of Bitcoin is not its technical superiority, but its ubiquity as the largest network.

The New World Order

We’ve explained how bitcoin could become a reserve currency in theory, but why exactly would it? Are there any potential catalysts? Every currency trades in pairs. The real question we must ask is if bitcoin is rising against the US dollar or if the US dollar is falling against bitcoin.

On the surface this is an absurd assertion. There are many currencies and bitcoin is rising against all of them. Bitcoin is rising against goods and services. These are fair arguments. However, underneath the surface there are complex suppositions.

For one, no goods or services are truly denominated in bitcoin. Bitcoin has no basket of native goods that we can compare to the same basket of goods we use to calculate USD inflation. The closest thing bitcoin has to that, is a basket of alternate cryptocurrencies (such as Ethereum) which as a whole are also rapidly rising.

The US dollar is also the reserve currency. Another way to look at it would be to think not about the US dollar in isolation, but to think of all currencies as an index. This leads us to the bold possibility that all currencies are plummeting against the bitcoin. Consider that bitcoin may be like a new technology that has come along, and now central-bank-backed currencies are facing a certain degree of obsoletion. We still use desktop computers today (this article was written on one), but many of you are reading this on a mobile device, as most of our “personal computing” is now done on a handheld mobile device.

If this theory is true it is highly consequential. It would open up the possibility that bitcoin is stable and currency is actually volatile, whipsawing in value. This is a stretch, but an important consideration. Alternatively, bitcoin may stabilize with scale and maturity. This would enable people in even the remote parts of the world access to a stable store of value, with little more than a smartphone. Talk about an upside catalyst.

We created a new world order in 1945… …We created a new dollar based monetary system… 1945 we began a new world order, and we had the United Nations in New York. And we had the World Bank and the IMF in Washington, because it was the American enterprise. And then we had 80% of the world’s gold and we began a process.

Now we’re heavily in debt and we are at those kinds of limits and so on. How are we going to restructure that world order?

According to Dalio, “”having the world’s printing press to produce the world’s currency is the equivalent of having the world’s most important asset.” We interpret this as having the reserve currency. This is something that Dalio wrote about extensively in his book Big Debt Crises, which lays out a clear argument that a country cannot go into hyperinflation so long as it has the printing press for the currency in which its debts are denominated. Note that this is an important feature of Modern Monetary Theory, which argues governments should worry about inflation more than total debt.

In our view, the printing press for the reserve currency is the world’s most valuable asset because the US is in large part printing dollars in exchange for real goods and services. The might of the US dollar was leveraged during the pandemic, as large amounts of money printing offset a global shortage in dollars as firms scrambled a safe-haven. This is why despite printing trillions during the pandemic, the inflation rate is a measly ~1.2%.

But to think that the dollar is invincible is misleading. Technology is transforming our society as a whole, and some of the consequences have been negative. We believe that business models that use algorithms designed to addict users and then monetize their outrage by selling them ads have had a strongly negative affect on society. In fact, this may be destabilizing the country.

(Protests turn to riots on Capitol Hill, Image Source: Google Images)

The imagery from Capitol Hill last week was both shocking and ominous. After a summer of both protest and political violence, encouraged by US politicians and the media, tensions have risen even further as rioters from the other side of the political spectrum broke into the US Capitol sending the entire US congress scrambling into underground tunnels. Let us be clear. This is not to, in any way, glorify political violence or rebellion against the government (though the later was thematic in the creation of bitcoin).

We instead are highlighting what should be obvious, that our system and the benefits we enjoy from it are much more vulnerable than we realize. Is bitcoin rising against the US dollar or is the US dollar falling against bitcoin? Consider that bitcoin hit 37,000 shortly after protestors stormed the capital, climbing to over $40,000 before crashing back down to $33,000 as President Trump issued a video concession and things calmed down a bit.

Some fantasize that a “second civil war” is a winnable proposition. Even a minor uprising could be catastrophic for the United States. It could destabilize the dollar and delegitimize its role as a reserve currency. Since printing US Dollars in exchange for real goods and services is critical to functioning of the US economy (a privilege of being the world reserve currency), it would also set off a domino effect that would end in economic disaster.

Unfortunately, tensions over the 2020 election are not the only threat to dollar stability. The unrest we have seen in 2020 and early 2021 may only be a preview of what’s to come, as AI and robotics displace workers over the next decade. Facebook has also jumped on the bandwagon with Libra, a project to create a “stable coin” linked to a global currency basket.

Confidence in the US dollar and its position as the reserve currency is much more likely to be toppled by geopolitical unrest than concerns about US debt or how much fiat currency the Federal Reserve is printing. Again, this all shows just how fragile our system can be. If the dollar is no longer a safe haven, a run from the dollar might result in a flight to bitcoin. This is the unfortunate reality of the situation.

Is bitcoin better than gold?

Bitcoin and gold have many similarities. Gold has a distinct history as a reserve asset. Supply increases in gold are limited to how much of it we can dig up out of the earth, the same way that the creation of bitcoin is limited to the function of its algorithm. This supply cannot be expanded in times of crisis to spur credit creation, which is why it has had limited appeal to central bankers. When a crisis occurs, we are all forced to pay the tax.

Gold may have valuable uses in industrial applications, but Bitcoin has one distinct advantage over gold. Gold suffers from the trust problem that bitcoin’s technology eliminates. If you want to borrow against your gold, or use it as collateral, a counterparty must trust that you actually have it. If you put it in a bank, you no longer have sovereignty over it.

Bitcoin’s system of registry and encryption is its innovation. That’s the blockchain, an algorithm that eliminates the need for trust. This innovation is not only a massive leap forward in technology, it is perhaps the first major innovation in banking since electronic markets were first introduced to trading floors. All other innovations seem incremental in comparison.

Bitcoin adopters entrust in a system that is designed not trust or be trusted by anyone, by giving everyone a perfect record of all accounts and transactions. Bitcoin can be stolen from an exchange intermediary, but it cannot be stolen from the blockchain database.

Conclusion

(An excerpt from the book Superintelligence by Nick Bostrom. This graph and the passage above really puts the exponential effect of technology-driven disruption into perspective. Image Source: Nick Bostrom.)

As a transactional form of currency, bitcoin’s limitations are inherent. As a reserve asset, bitcoin’s possibilities are limitless. One Satoshi could equal $1, $10, $100… it is infinitely scalable.

It is also likely ungovernable, adhering only to the will of the people. If governments attempt to reign in bitcoin with regulation, a new layer could emerge with users bypassing the exchange intermediaries (such as Coinbase) with their wallets running on their own local hardware connected directly to the network. This was way it was done in the beginning. If governments target the free will of the individual, this too could backfire. It might only drive fear that they are attempting to salvage their authority from the onslaught of technology, driving bitcoin’s legitimacy.

You know, what is money? Money is an entry in a database.

We are living in one of the most bizarre moments in history, driven by the accelerating pace of technology, an exponential curve. Tech investors often go by the idiom “if you’re not early you’re late.” Perhaps the euphoria and excitement regarding the tech bubble, that humanity would be reshaped by the transformative impact of networks and computers, was not wrong. Just early. Though there are certain “meme stocks” that are in a phase speculative euphoria today, perhaps this time it is very different in a general sense, and things like bitcoin will indeed be transformative in the long run.

There are nations in the world who would like to see the end of the US dollar’s dominance, as it would shift the balance of power in their favor. There are central bankers who would like to see digital currencies, giving them incredible new tools to track, monitor, and implement monetary policy directly. But perhaps a new Bretton Woods agreement has already happened, and it was a group of cryptographers and software developers creating bitcoin… Giving the power of the central banks to the masses. If the government can click a few keys at the Federal Reserve and create money, why can’t we?

Equities analyst at a long/short hedge fund. Occasionally I publish some of the more interesting research I…

Long/Short Equity

Contributor Since 2013

Equities analyst at a long/short hedge fund. Occasionally I publish some of the more interesting research I work on for fun. These are my personal thoughts and not investment advice.

Disclosure: I am/we are long BTC-USD. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: We are also investors in cryptocurrency mining.

NEW YORK (Reuters) – Treasury Secretary Timothy Geithner said on Wednesday the U.S. dollar will remain the world’s reserve currency for a long time, though he expressed openness to expanded use of an IMF currency basket.

The U.S. dollar tumbled after Geithner told policy-makers and business executives at the Council on Foreign Relations that he was “quite open” to a Chinese suggestion to move toward greater use of an IMF-created global currency basket comprising dollar, euros, sterling and yen.

Prompted by the moderator to clarify his position, Geithner said: “The dollar remains the world’s dominant reserve currency and I think that’s likely to continue for a long period of time.”

“As a country, we will do what’s necessary to make sure we’re sustaining confidence in our financial markets and in this economy’s long-term fundamentals,” he added.

Earlier this week, Chinese central bank governor Zhou Xiaochuan, said the world should consider using the IMF’s Special Drawing Rights (SDR) basket as a super-sovereign reserve currency.

Geithner said he hadn’t read Zhou’s proposal, but added, “as I understand it, it’s a proposal designed to increase the use of the IMF’s Special Drawing Rights. I am actually quite open to that suggestion.”

“But you should think of it as rather evolutionary, building on the current architecture, than rather than moving us to global monetary union.”

China’s foreign exchange reserves are the largest in the world at nearly $2 trillion and China is the biggest holder of U.S. Treasury debt.

The dollar initially fell against the euro on reports of Geithner’s remarks, but pared losses he reiterated his faith in the dollar as world reserve currency.

“Geithner admits to not having read China’s proposal, and President Obama’s comments on the dollar yesterday — no need for another reserve currency and that the dollar was fundamentally strong — was more of the underlying signal,” said Marc Chandler, senior currency strategist at Brown Brothers Harriman in New York.

Senior Obama adviser Paul Volcker also said on Wednesday a Chinese suggestion to move toward a world currency system linked to the IMF’s SDRs was not practical.

“I understand restiveness about the lopsided nature of the present international monetary system that’s so dependent on the dollar,” Volcker said at a panel with British Prime Minister Gordon Brown at New York University.

But Volcker said when China questioned the dollar’s role as the world reserve currency, “They ignore the fact that they didn’t have to buy those dollars in the first place so they contributed to the problem.

FOREIGN APPETITE STRONG

Speaking on CNBC television later Wednesday, Geithner underscored his desire to see a strong dollar.

“I want to say this very clearly, a strong dollar is in America’s interest. We are going to make sure to pursue policies that improve the long-term fundamentals of the U.S. economy,” he said. Geithner also said there was “no evidence” foreign investors were losing interest in buy U.S. debt.

He also told CNBC there were signs the government’s efforts to support the economy and stabilize the financial sector were beginning to bear fruit, with the “pace of deterioration” slowing in some areas.

Geithner said in the interview that he was committed to putting the funds remaining in the Treasury $700 billion financial rescue program to work quickly and efficiently, and he held the door open to asking Congress for more.

“We always said this crisis may require more resources to deal with effectively, and we’re going to make sure we work with the Congress over time so that we can do this on a scale that is going to bring recovery back as soon as possible,” he said.

Geithner played down the idea that there was a sharp division between the United States and Europe over the amount of fiscal stimulus need to combat the global downturn.

“I think there is more commitment to a greater level of stimulus across the major economies than we’ve ever seen,” he said.

UNITED NATIONS (Reuters) – A new United Nations report released on Tuesday calls for abandoning the U.S. dollar as the main global reserve currency, saying it has been unable to safeguard value.

But several European officials attending a high-level meeting of the U.N. Economic and Social Council countered by saying that the market, not politicians, would determine what currencies countries would keep on hand for reserves.

“The dollar has proved not to be a stable store of value, which is a requisite for a stable reserve currency,” the U.N. World Economic and Social Survey 2010 said.

The report says that developing countries have been hit by the U.S. dollar’s loss of value in recent years.

“Motivated in part by needs for self-insurance against volatility in commodity markets and capital flows, many developing countries accumulated vast amounts of such (U.S. dollar) reserves during the 2000s,” it said.

The report supports replacing the dollar with the International Monetary Fund’s special drawing rights (SDRs), an international reserve asset that is used as a unit of payment on IMF loans and is made up of a basket of currencies.

“A new global reserve system could be created, one that no longer relies on the United States dollar as the single major reserve currency,” the U.N. report said.

The report said a new reserve system “must not be based on a single currency or even multiple national currencies but instead, should permit the emission of international liquidity — such as SDRs — to create a more stable global financial system.”

“Such emissions of international liquidity could also underpin the financing of investment in long-term sustainable development,” it said.

MARKETS DECIDE

Jomo Kwame Sundaram, a Malaysian economist and the U.N. assistant secretary general for economic development, told a news conference that “there’s going to be resistance” to the idea.

“In the whole post-war period, we’ve essentially had a dollar-based system,” he said, adding that the gradual emission of SDRs could help countries phase out the dollar.

Nobel Prize-winning economist Joseph Stiglitz, who previously chaired a U.N. expert commission that considered ways of overhauling the global financial system, has advocated the creation of a new reserve currency system, possibly based on SDRs.

Russia and China have also supported the idea.

But Paavo Vayrynen, Finland’s Foreign Trade and Development Minister, told reporters that he doubted it was possible “to make any political or administrative decisions how to formulate the currency system in the world.”

“It is based on the markets,” he said. “I believe that the economic players in the market are going to have the decisive influence on that issue.”

European Union development commissioner Andris Piebalgs said it would be a bad idea to dictate what the reserve currency should be.

“It is markets that decide,” he said. “Any intervention would just create additional challenges and make things even less predictable.”

(Protests turn to riots on Capitol Hill, Image Source: Google Images)

(An excerpt from the book Superintelligence by Nick Bostrom. This graph and the passage above really puts the exponential effect of technology-driven disruption into perspective. Image Source: Nick Bostrom.)

5.33K Followers

5.33K Followers

{kind=link}