Something’s happening to wages that neither Democrats nor Republicans care to acknowledge.

Stop me if this sounds familiar: For most American workers, real wages have barely budged in decades. Inequality has skyrocketed. The richest workers are making all the money. Earnings for low-income workers have been pathetic this entire century.

These claims help drive the interpretation of breaking economic news. For example, the Labor Department yesterday reported that the unemployment rate fell to a 50-year low, while wage growth stalled. “The wage numbers here are INSANE,” the MSNBC host Chris Hayes tweeted. “The tightest labor market in decades and decades and ordinary working people are barely seeing gains.”

Imagine a world where wage growth was truly stagnant only for workers in high-wage industries, such as medicine and consulting.

Imagine a labor market where earnings growth for low-wage workers, such as those who work in retail and restaurants, had doubled in the past five years.

Imagine an economy where wages for the poorest Americans were rising twice as fast as hourly earnings for high-wage earners.

It turns out that all three of those things are happening right now.

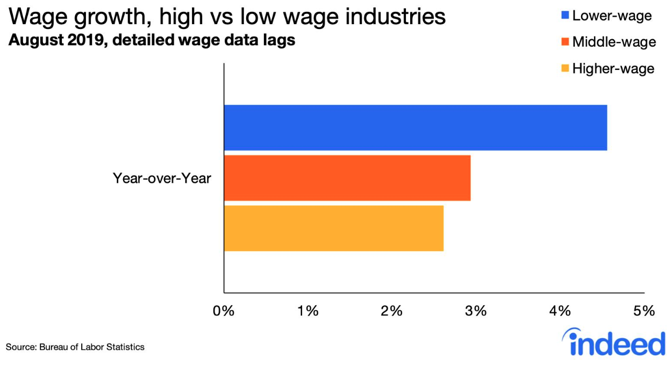

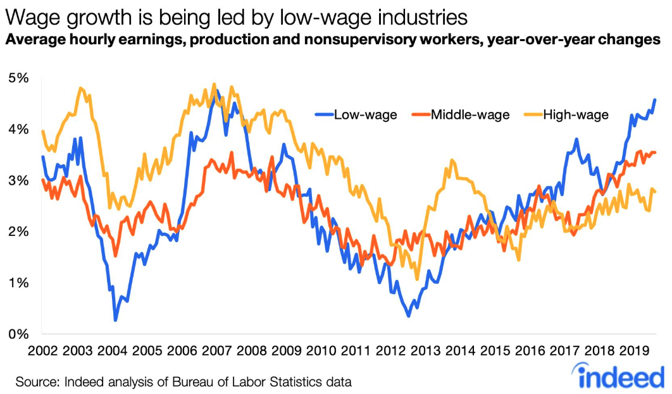

According to analysis by Nick Bunker, an economist with the jobs site Indeed, wage growth is currently strongest for workers in low-wage industries, such as clothing stores, supermarkets, amusement parks, and casinos. And earnings are growing most slowly in higher-wage industries, such as medical labs, law firms, and broadcasting and telecom companies.

Bunker’s analysis is not an outlier. A Goldman Sachs look at data from the Bureau of Labor Statistics found growth for the bottom half of earners at its highest rate of the cycle. And even among that bottom half, the biggest gains are going to workers earning the least. A New York Times analysis of data from the Federal Reserve Bank of Atlanta found that wage growth among the lowest 25 percent of earners had exceeded the growth in every other quartile.

In fact, according to Bunker’s research, wages for low-income workers may be growing at their highest rate in 20 years.

What’s happening here? Donald Trump hasn’t sprinkled MAGA pixie dust over the U.S. economy. In fact, his trade war has clearly diminished employment growth in industries, that are sensitive to foreign markets, such as manufacturing. Rather, a tight labor market and state-by-state minimum wage hikes have combined to push up wage growth for the poorest workers. The sluggishness of overall wage growth is concealing the fact that the labor market has done wonderful things for wages at the low end.

One reason you haven’t heard this economic narrative may be that it’s inconvenient for members of both political parties to talk about, especially at a time when economic analysis has, like everything else, become a proxy for political orientation. For Democrats, the idea that low-income workers could be benefiting from a 2019 economy feels dangerously close to giving the president credit for something. This isn’t just poor motivated reasoning; it also attributes way too much power to the American president, who exerts very little control over the domestic economy. Meanwhile, corporate-friendly outlets, such as TheWall Street Journal’s editorial pages, have reported on this phenomenon. But they’ve used it as an opportunity to take a shot at “the slow-growth Obama years” rather than a way to argue for the extraordinary benefits of tight labor markets for the poor, much less for the virtues of minimum-wage laws.

Democrats don’t want to talk about low-income wage growth, because it feels too close to saying, “Good things can happen while Trump is president”; and Republicans don’t want to talk about the reason behind it, because it’s dangerously close to saying, “Our singular fixation with corporate-tax rates is foolish and Keynes was right.”

But good things can happen while Trump is president, and Keynes was right. “Tighter labor markets sure are good for workers who work in low-wage industries,” Bunker told me. “This recovery has not been spectacular. But if we let the labor market get stronger for a long time, you will see these results.”

The problem goes much deeper than Trump or tariffs.

Global markets were seized by fear last week that trade wars were slowing growth in Germany, China and the United States. But the story here is bigger than President Trump and his tariffs.

The postwar miracle is over. Since the financial crisis of 2008, the world economy has been struggling against four headwinds:

deglobalization of trade,

depopulation as labor forces shrink,

declining productivity and a

debt burden as high now as it was right before the crisis.

No major economy is growing as fast as it was before 2008. Not one is growing faster than 10 percent, the rate experienced by the Asian “miracle economies” before the crisis. In almost every country, the national discussion focuses on what must be done to revive growth and ignores the fact that the slowdown is driven by forces beyond any one government’s control. Instead of dooming ourselves to serial disappointment and fruitless stimulus campaigns, we need to redefine economic success and failure.

Germany is one of at least five major economies on the verge of a recession, which is typically defined as two consecutive quarters of negative growth. But the real issue is whether that definition still makes sense in a country with a shrinking labor force like Germany’s.

Its working population has been declining for years and is expected to fall to 47 million from 54 million by 2039. And it’s not alone in this. Forty-six countries around the world — including major powers like Japan, Russia and China — now have shrinking populations.

Demographics are usually the main driver of economic growth, so it is basically inevitable that these countries will now grow at a much slower pace. And we are not talking about minor population declines. Projections for 2040 show China’s working-age population falling by 114 million, Japan’s by 14 million. With a shrinking labor force, these economies will inevitably slow and, at times, contract. To keep calling two negative quarters in a row a “recession” implies that this outcome is somehow abnormal or unhealthy. That will no longer be the case.

To avoid overreacting, the discussion about economic health needs to shift to measures that better capture satisfaction and contentment, like per capita income growth. In countries with shrinking populations, per capita incomes can continue to grow so long as the economy is shrinking less rapidly than the population. This helps explain why, for example, Japan isn’t facing more social unrest. Its economy has grown much more slowly than that of the United States in this decade, but because the population is shrinking its per capita income has grown just as fast as America’s — around 1.5 percent per year.

Shrinking populations also help explain why unemployment is at or near multi-decade lows, even in countries with serious growth worries, like Germany and Japan. Gainfully employed Germans and Japanese won’t really feel as if their countries are in a slump until per capita G.D.P. growth turns negative — which may prove to be a more useful way to think about recessions in this new era.

The definition of success also needs to change. Many emerging countries still aspire to the double-digit growth rates experienced by what were known as the “Asian miracle economies” from the mid-1960s to the early 1990s, when populations and trade were booming. But no economy had grown so fast before then, and as population and trade surges recede, it’s unlikely any country can repeat those feats.

As growth downshifts, even little miracles are disappearing. Before the 2010s, it was common for one in every five economies to be growing at 7 percent or more annually. Now, among the world’s 200 economies, just eight, or one in 25, are on track to grow 7 percentthis year. Most of those are small economies in Africa.

When the news emerged that China’s economy had slowed to just 6 percent, a new low, many investors and analysts rang the alarm bells. But the reality is that economies rarely grow as fast as 6 percent if the population is not booming too. Not only did China’s working-age population growth turn negative in 2016, but it is one of the countries hardest hit by slumping trade, declining productivity and heavy debts. If the Chinese economy really were growing at 6 percent in this environment, it would be cause for celebration, not alarm.

The benchmark for rapid growth should come down to 5 percent for emerging countries, to between and 3 and 4 percent for middle-income countries like China, and to between 1 and 2 percent for developed economies like the United States, Germany and Japan. And that should just be the start to how economists and investors redefine economic success.

This rethink is overdue. The number of countries with shrinking populations is expected to rise to 67 from 46 by 2040, and the decline in productivity growth is in many ways reinforced by heavy debt burdens and rising trade barriers. Redefining the standard of economic success could help cure many countries of irrational anxieties about “slow” growth, and make the world a calmer place.

The Fed is very close to having satisfied its maximum employment and price stability mandates and you can see that most people feel good about the economy and the Fed.

But it would concern me — President Trump’s comments about Chair Powell and about the Fed do concern me, because if that becomes concerted, I think it does have the impact, especially if conditions in the U.S. for any reason were to deteriorate, it could undermine confidence in the Fed. And I think that that would be a bad thing.

Ryssdal:Do you think the president has a grasp of macroeconomic policy?

Yellen:No, I do not.

Ryssdal:Tell me more.

Yellen:Well, I doubt that he would even be able to say that the Fed’s goals are maximum employment and price stability, which is the goals that Congress have assigned to the Fed. He’s made comments about the Fed having an exchange rate objective in order to support his trade plans, or possibly targeting the U.S. balance of trade. And, you know, I think comments like that shows a lack of understanding of the impact of the Fed on the economy, and appropriate policy goals.