Jim Rickards, legendary gold expert, says soon 👉YOU MIGHT NOT BE ABLE TO BUY GOLD AT ANY PRICE!! 👈I reveal the insider information YOU NEED to understand Jim Rickards reasoning and determine if you should buy gold now or wait. And how gold could go to 100k an ounce!! Jim Rickards is the foremost expert on the price of gold, when he talks the markets listen and YOU SHOULD TOO. If you’ve followed his work you know Jim Rickards is one of the premier macro thinkers in the world. And if you don’t know who Jim Rickards is, you need discover his ideas RIGHT NOW. Understanding and listening to Jim Rickards now, could save and make you a lot of money in the future.

Jim Rickards is a heavy hitter in the world of macro economics and gold. He’s revered as one of the top thinkers in the country and he’s made some huge calls on the price of gold saying it can easily to to $10,000 to $50,000 an ounce. Jim Rickards comes to that conclusion in a very scientific manner. It’s really just about math.

In this Jim RIckards video I explain how he comes to those conclusions and then go on to reveal how the price of gold could actually go to $100,000 an ounce!! As shocking as it sounds its realistic, but you’ve got to watch the video to discover the details.

This is a must watch Jim Rickards video, I discuss the following:

1. How experts like Jim Rickards, Peter Schiff, and Jim Rogers think the dollar will crash.

2. You’ll discover the actually math behind how Jim Rickards comes to his 10k-50k gold price.

3. I reveal how, using Jim Rickards logic, the gold price could actually go to 100k and higher!

If you’re interested in the gold price or Jim Rickards you’re going to love this video!!

For more content like this that’ll help you build wealth and thrive in a world of out of control central banks and big governments check out the videos below!!

And if you’d like to support the channel via PayPal here’s our link! THANK YOU!!! 😁

On July 2, 2018, Reason and The Soho Forum hosted a debate between Erik Voorhees, the CEO of ShapeShift, and Peter Schiff, CEO and chief global strategist of Euro Pacific Capital. The proposition: “Bitcoin, or a similar form of cryptocurrency, will eventually replace governments’ fiat money as the preferred medium of exchange.”

Reason is the planet’s leading source of news, politics, and culture from a libertarian perspective. Go to reason.com for a point of view you won’t get from legacy media and old left-right opinion magazines.

_____

It was an Oxford-style debate in which the audience votes on the resolution at the beginning and end of the event, and the side that gains the most ground is victorious. Voorhees won by changing the minds of 15 percent of attendees.

The Soho Forum is held every month at the SubCulture Theater in Manhattan’s East Village. At the next debate, which will be held on August 27, William Easterly, professor of economics at NYU, and Joseph Stiglitz, a Nobel Prize Winner in economics and professor at Columbia, will discuss whether free markets or government action is the best way to eliminate global poverty. You can buy tickets here.

Satoshi gave the world Bitcoin, a true “something for nothing.” His discovery of absolute scarcity for money is an unstoppable idea that is changing the world tremendously, just like its digital ancestor: the number zero.

Zero is Special

“In the history of culture the discovery of zero will always stand out as one of the greatest single achievements of the human race.” — Tobias Danzig, Number: The Language of Science

Many believe that Bitcoin is “just one of thousands of cryptoassets”—this is true in the same way that the number zero is just one of an infinite series of numbers. In reality, Bitcoin is special, and so is zero: each is an invention which led to a discovery that fundamentally reshaped its overarching system—for Bitcoin, that system is money, and for zero, it is mathematics. Since money and math are mankind’s two universal languages, both Bitcoin and zero are critical constructs for civilization.

For most of history, mankind had no concept of zero: an understanding of it is not innate to us—a symbol for it had to be invented and continuously taught to successive generations. Zero is an abstract conception and is not discernible in the physical world—no one goes shopping for zero apples. To better understand this, we will walk down a winding path covering more than 4,000 years of human history that led to zero becoming part of the empirical bedrock of modernity.

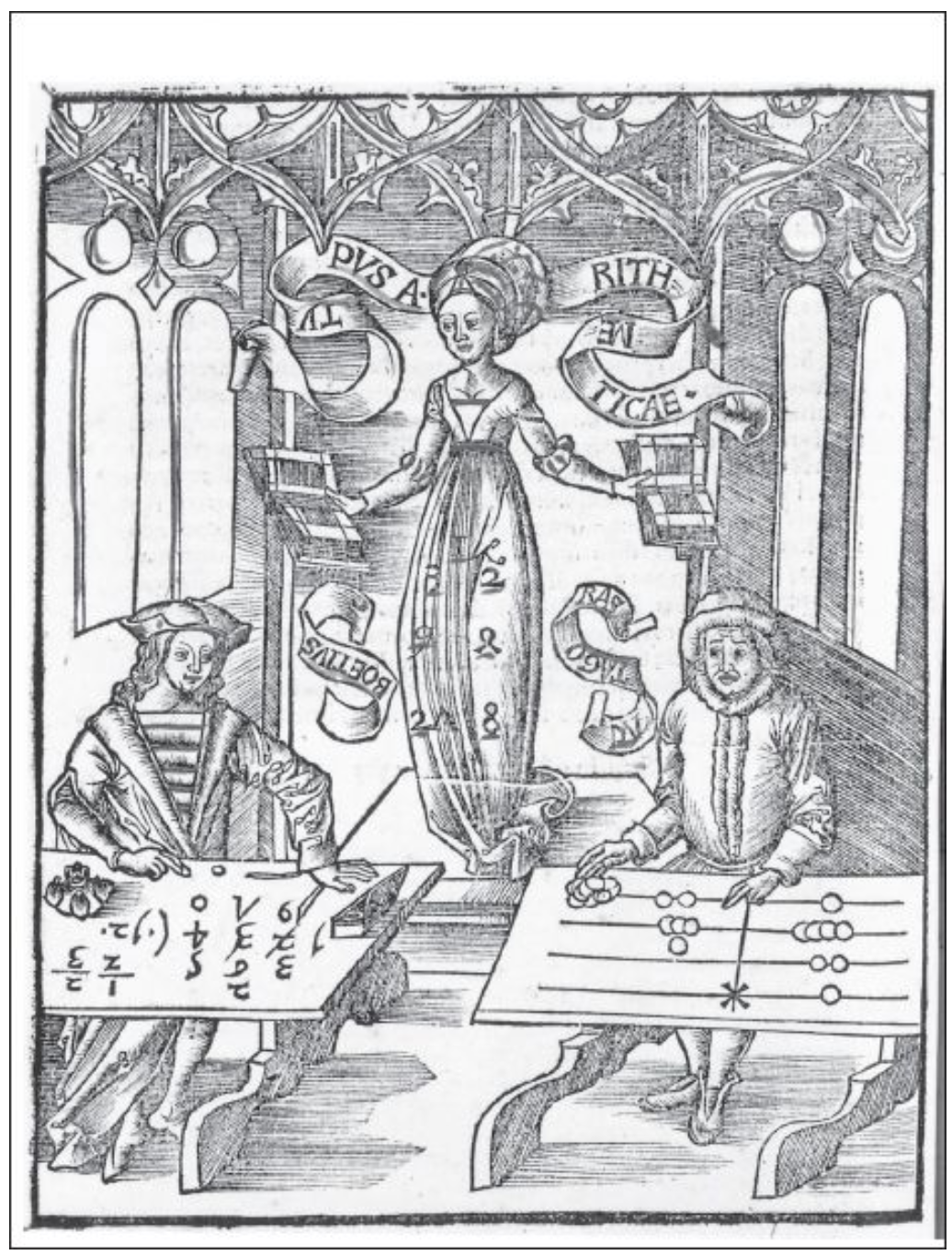

Numerals, which are symbols for numbers, are the greatest abstractions ever invented by mankind: virtually everything we interact with is best grasped in numerical, quantifiable, or digital form. Math, the language of numerals, originally developed from a practical desire to count things—whether it was the amount of fish in the daily catch or the days since the last full moon. Many ancient civilizations developed rudimentary numeral systems: in 2000 BCE, the Babylonians, who failed to conceptualize zero, used two symbols in different arrangements to create unique numerals between 1 and 60:

Babylonian cuneiform was a relatively inefficient numeral system — notice how many more written strokes are necessary for each number symbol — and calculation using it was even more cumbersome.

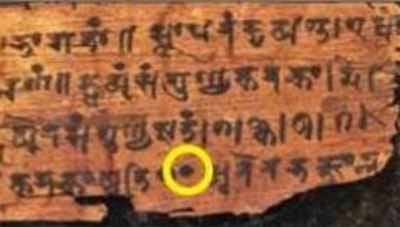

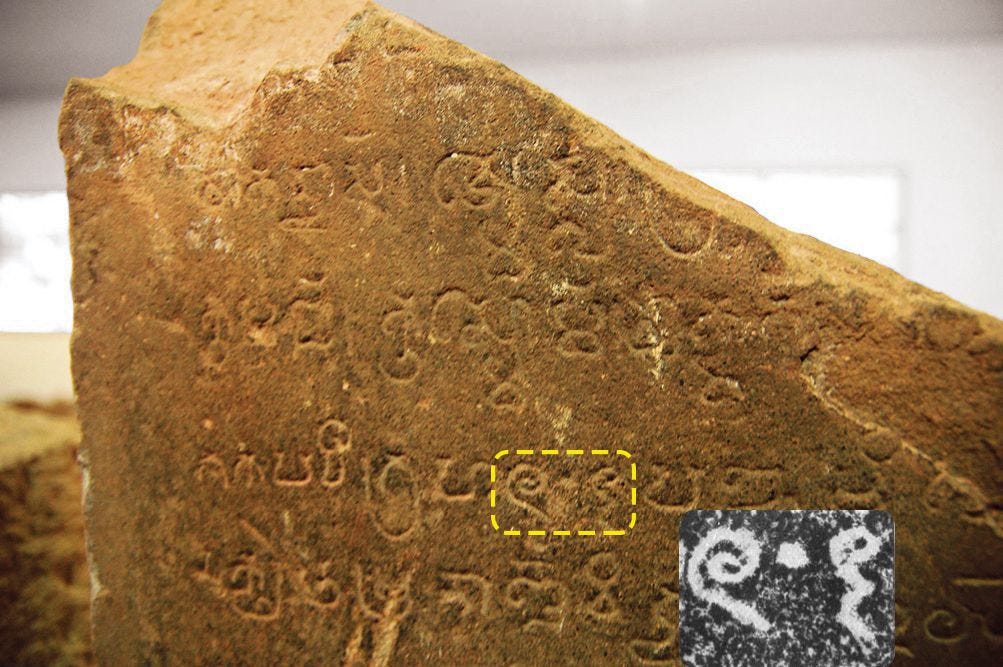

Vestiges of the base-60 Babylonian cuneiform system still exist today: there are 60 seconds in a minute, 60 minutes in an hour, and 6 sets of 60 degrees in a circle. But this ancient system lacked a zero, which severely limited its usefulness. Ancient Greeks and Mayans developed their own numeral systems, each of which contained rough conceptions of zero. However, the first explicit and arithmetic use of zero came from ancient Indian and Cambodian cultures. They created a system with nine number symbols and a small dot used to mark the absence of a number—the original zero. This numeral system would eventually evolve into the one we use today:

The first known written zero: from the Bakhshali manuscript which contains pages dating back to the 3rd and 4th centuries AD.

Inscription K-127 bears the earliest zero ever discovered—dated from the 7th century, it was discovered in the 19th century in Cambodia.

In the 7th century, the Indian mathematician Brahmagupta developed terms for zero in addition, subtraction, multiplication, and division (although he struggled a bit with the latter, as would thinkers for centuries to come). As the discipline of mathematics matured in India, it was passed through trade networks eastward into China and westward into Islamic and Arabic cultures. It was this western advance of zero which ultimately led to the inception of theHindu-Arabic numeral system—the most common means of symbolic number representation in the world today:

The Economization of Math

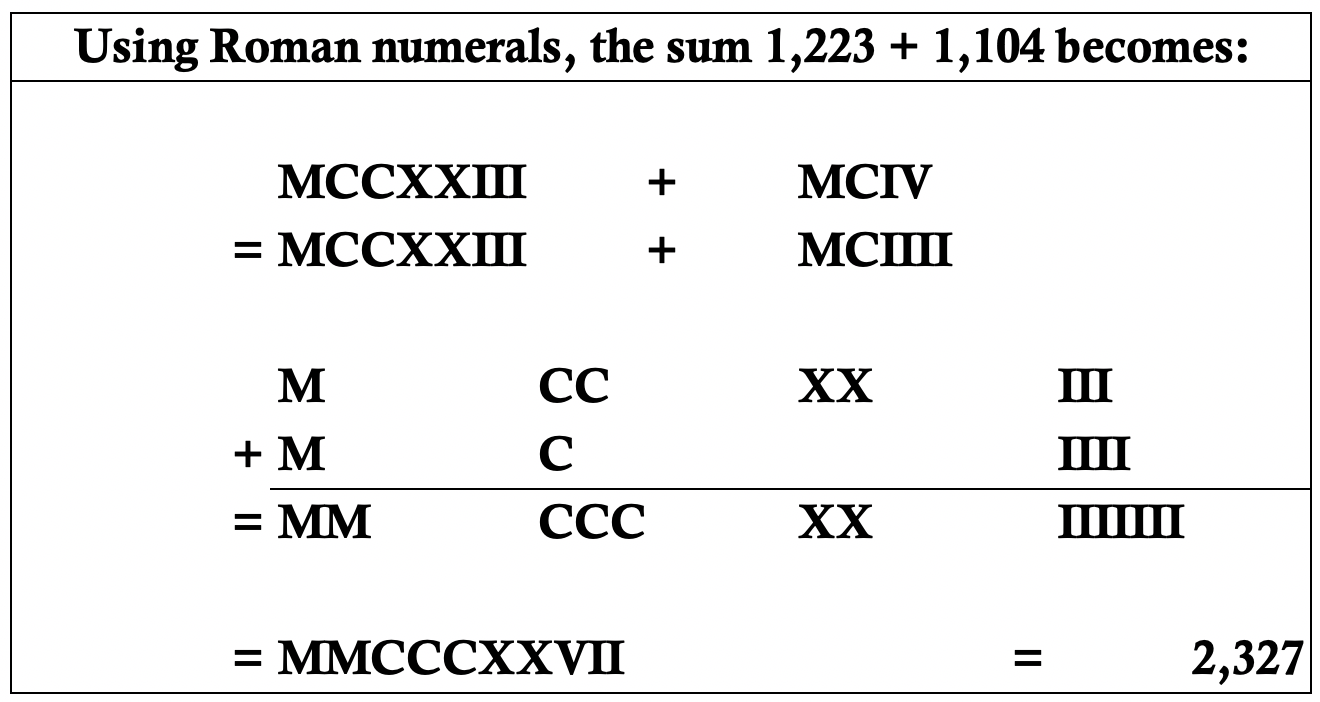

When zero reached Europe roughly 300 years later in the High Middle Ages, it was met with strong ideological resistance. Facing opposition from users of the well-established Roman numeral system, zero struggled to gain ground in Europe. People at the time were able to get by without zero, but (little did they know) performing computation without zero was horribly inefficient. An apt analogy to keep in mind arises here: both math and money are possible without zero and Bitcoin, respectively—however both are tremendously more wasteful systems without these core elements. Consider the difficulty of doing arithmetic in Roman numerals:

If you thought you were bad at arithmetic using numbers, just try doing it with letters.

Calculation performed using the Hindu-Arabic system is significantly more straightforward than with Roman numerals—and energy-efficient systems have a tendency to win out in the long run, as we saw when the steam engine outcompeted animal-sourced power or when capitalism prevailed over socialism (another important point to remember for Bitcoin later). This example just shows the pains of addition—multiplication and division were even more painstaking. As Amir D. Aczel described it in his book Finding Zero:

“[The Hindu-Arabic numeral system] allowed an immense economy of notation so that the same digit, for example 4, can be used to convey itself or forty (40) when followed by a zero, or four hundred and four when written as 404, or four thousand when written as a 4 followed by three zeros (4,000). The power of the Hindu-Arabic numeral system is incomparable as it allows us to represent numbers efficiently and compactly, enabling us to perform complicated arithmetic calculations that could not have been easily done before.”

Roman numeral inefficiency would not be tolerated for long in a world enriching itself through commerce. With trade networks proliferating and productivity escalating in tandem, growing prospects of wealth creation incentivized merchants to become increasingly competitive, pushing them to always search for an edge over others. Computation and record-keeping with a zero-based numeral system was qualitatively easier, quantitatively faster, and less prone to error. Despite Europe’s resistance, this new numeral system simply could not be ignored: like its distant progeny Bitcoin would later be, zero was an unstoppable idea whose time had come:

Functions of Zero

Zero’s first function is as a placeholder in our numeric system: for instance, notice the “0” in the number “1,104” in the equation above, which indicates the absence of value in the tens place. Without zero acting as a symbol of absence at this order of magnitude in “1,104,” the number could not be represented unambiguously (without zero, is it “1,104” or “114”?). Lacking zero detracted from a numeral system’s capacity to maintain constancy of meaning as it scales. Inclusion of zero enables other digits to take on new meaning according to their position relative to it. In this way, zero lets us perform calculation with less effort—whether its pen strokes in a ledger, finger presses on a calculator, or mental gymnastics. Zero is a symbol for emptiness, which can be a highly useful quality—as Lao Tzu said:

“We shape clay into a pot, but it is the emptiness inside that holds whatever we want.”

More philosophically, zero is emblematic of the void, as Aczel describes it:

“…the void is everywhere and it moves around; it can stand for one truth when you write a number a certain way — no tens, for example — and another kind of truth in another case, say when you have no thousands in a number!”

Drawing analogies to the functions of money: zero is the “store of value” on which higher order of magnitude numerals can scale; this is the reason we always prefer to see another zero at the end of our bank account or Bitcoin balance. In the same way a sound economic store of value leads to increased savings, which undergirds investment and productivity growth, so too does a sound mathematical placeholder of value give us a numeral system capable of containing more meaning in less space, and supporting calculations in less time: both of which also foster productivity growth. Just as money is the medium through which capital is continuously cycled into places of optimal economic employment, zero gives other digits the ability to cycle—to be used again and again with different meanings for different purposes.

Zero’s second function is as a number in its own right: it is the midpoint between any positive number and its negative counterpart (like +2 and -2). Before the concept of zero, negative numbers were not used, as there was no conception of “nothing” as a number, much less “less than nothing.” Brahmagupta inverted the positive number line to create negative numbers and placed zero at the center, thus rounding out the numeral system we use today. Although negative numbers were written about in earlier times, like the Han Dynasty in China (206 BCE to 220 BCE), their use wasn’t formalized before Brahmagupta, since they required the concept of zero to be properly defined and aligned. In a visual sense, negative numbers are a reflection of positive numbers cast across zero:

Zero is the center of gravity for our entire numeral system, just as money is central to any economic system.

Interestingly, negative numbers were originally used to signify debts—well before the invention of double-entry accounting, which opted for debits and credits (partly to avoid the use of negative numbers). In this way, zero is the “medium of exchange” between the positive and negative domains of numbers—it is only possible to pass into, or out of, either territory by way of zero. By going below zero and conceptualizing negative numbers, many new and unusual (yet extremely useful) mathematical constructs come into being including imaginary numbers, complex numbers, fractals, and advanced astrophysical equations. In the same way the economic medium of exchange, money, leads to the acceleration of trade and innovation, so too does the mathematical medium of exchange, zero, lead to enhanced informational exchange, and its associated development of civilizational advances:

The Mandlebrot Set: one of the most famous examples of a fractal, a mind-bending mathematical structure formed with complex numbers that models the geometry of nature and its intrinsic complexity. One of the best known examples of mathematical beauty, this fractal exhibits infinite depth, breadth, and non-repeating self-similarity. Zero is a necessary prerequisite to such fractal modeling.

Zero’s third function is as a facilitator for fractions or ratios. For instance, the ancient Egyptians, whose numeral system lacked a zero, had an extremely cumbersome way of handling fractions: instead of thinking of 3/4 as a ratio of three to four (as we do today), they saw it as the sum of 1/2 and 1/4. The vast majority of Egyptian fractions were written as a sum of numbers as 1/n, where n is the counting number—these were called unit fractions. Without zero, long chains of unit fractions were necessary to handle larger and more complicated ratios (many of us remember the pain of converting fractions from our school days). With zero, we can easily convert fractions to decimal form (like 1/2 to 0.5), which obsoletes the need for complicated conversions when dealing with fractions. This is the “unit of account” function of zero. Prices expressed in money are just exchange ratios converted into a money-denominated price decimal: instead of saying “this house costs eleven cars” we say, “this house costs $440,000,” which is equal to the price of eleven $40,000 cars. Money gives us the ability to better handle exchange ratios in the same way zero gives us the ability to better handle numeric ratios.

Numbers are the ultimate level of objective abstraction: for example, the number 3 stands for the idea of “threeness” — a quality that can be ascribed to anything in the universe that comes in treble form. Equally, 9 stands for the quality of “nineness” shared by anything that is composed of nine parts. Numerals and math greatly enhanced interpersonal exchange of knowledge (which can be embodied in goods or services), as people can communicate about almost anything in the common language of numeracy. Money, then, is just the mathematized measure of capital available in the marketplace: it is the least common denominator among all economic goods and is necessarily the most liquid asset with the least mutable supply. It is used as a measuring system for the constantly shifting valuations of capital (this is why gold became money—it is the monetary metal with a supply that is most difficult to change). Ratios of money to capital (aka prices) are among the most important in the world, and ratios are a foundational element of being:

“In the beginning, there was the ratio, and the ratio was with God, and the ratio was God.” — John 1:1*

*(A more “rational” translation of Jesus’s beloved disciple John: the Greek word for ratio was λόγος (logos), which is also the term for word.)

An ability to more efficiently handle ratios directly contributed to mankind’s later development of rationality, a logic-based way of thinking at the root of major social movements such as the Renaissance, the Reformation, and the Enlightenment. To truly grasp the strange logic of zero, we must start with its point of origin—the philosophy from which it was born.

Philosophy of Zero

“In the earliest age of the gods, existence was born from non-existence.” — The Rig Veda

Zero arose from the bizarre logic of the ancient East. Interestingly, the Buddha himself was a known mathematician — in early books about him, like the Lalita Vistara, he is said to be excellent in numeracy (a skill he uses to woo a certain princess). In Buddhism, the logical character of the phenomenological world is more complex than true or false:

“Anything is either true,

Or not true,

Or both true and not true,

Or neither true nor not true.

This is the Lord Buddha’s teaching.”

This is the Tetralemma (or the four corners of the catuskoti): the key to understanding the seeming strangeness of this ancient Eastern logic is the concept of Shunya, a Hindi word meaning zero: it is derived from the Buddhist philosophical concept of Śūnyatā (or Shunyata). The ultimate goal of meditation is the attainment of enlightenment, or an ideal state of nirvana, which is equivalent to emptying oneself entirely of thought, desire, and worldly attachment. Achievement of this absolute emptiness is the state of being in Shunyata: a philosophical concept closely related to the void—as the Buddhist writer Thich Nhat Hanh describes it:

“The first door of liberation is emptiness, Shunyata

Emptiness always means empty of something

Emptiness is the Middle Way between existent and nonexistent

Reality goes beyond notions of being and nonbeing

True emptiness is called “wondrous being,” because it goes beyond existence and nonexistence

The concentration on Emptiness is a way of staying in touch with life as it is, but it has to be practiced and not just talked about.”

Or, as a Buddhist monk of ancient Wats temple in Southeast Asia described the meditative experience of the void:

“When we meditate, we count. We close our eyes and are aware only of where we are at in the moment, and nothing else. We count breathing in, 1; and we count breathing out, 2; and we go on this way. When we stop counting, that is the void, the number zero, the emptiness.”

A direct experience of emptiness is achievable through meditation. In a true meditative state, the Shunyata and the number zero are one and the same. Emptiness is the conduit between existence and nonexistence, in the same way zero is the door from positive to negative numbers: each being a perfect reflection of the other. Zero arose in the ancient East as the epitome of this deeply philosophical and experiential concept of absolute emptiness. Empirically, today we now know that meditation benefits the brain in many ways. It seems too, that its contribution to the discovery of zero helped forge an idea that benefits mankind’s collective intelligence — our global hive-mind.

Despite being discovered in a spiritual state, zero is a profoundly practical concept: perhaps it is best understood as a fusion of philosophy and pragmatism. By traversing across zero into the territory of negative numbers, we encounter the imaginary numbers, which have a base unit of the square root of -1, denoted by the letter i. The number i is paradoxical: consider the equations x² + 1 = 0 and x³ + 1 = 0, the only possible answers are positive square root of -1 (i) and negative square root of -1 (-i or i³), respectively. Visualizing these real and imaginary domains, we find a rotational axis centered on zero with orientations reminiscent of the tetralemma: one true (1), one not true (i), one both true and not true (-1 or i²), and one neither true nor not true (-i or i³):

Zero is the fulcrum between real and imaginary number planes.

Going through the gateway of zero into the realms of negative and imaginary numbers provides a more continuous form of logic when compared to the discrete either-or logic, commonly accredited to Aristotle and his followers. This framework is less “black and white” than the binary Aristotelean logic system, which was based on true or false, and provides many gradations of logicality; a more accurate map to the many “shades of grey” we find in nature. Continuous logic is insinuated throughout the world: for instance, someone may say “she wasn’t unattractive,” meaning that her appeal was ambivalent, somewhere between attractive and unattractive. This perspective is often more realistic than a binary assessment of attractive or not attractive.

Importantly, zero gave us the concept of infinity: which was notably absent from the minds of ancient Greek logicians. The rotations around zero through the real and imaginary number axes can be mathematically scaled up into a three-dimensional model called the Riemann Sphere. In this structure, zero and infinity are geometric reflections of one another and can transpose themselves in a flash of mathematical permutation. Always at the opposite pole of this three-dimensional, mathematical interpretation of the tetralemma, we find zero’s twin—infinity:

Scaling the real and imaginary number planes into the third dimension, we discover zero’s twin: infinity.

The twin polarities of zero and infinity are akin to yin and yang — as Charles Seife, author of Zero: Biography of a Dangerous Idea, describes them:

“Zero and infinity always looked suspiciously alike. Multiply zero by anything and you get zero. Multiply infinity by anything and you get infinity. Dividing a number by zero yields infinity; dividing a number by infinity yields zero. Adding zero to a number leaves it unchanged. Adding a number to infinity leaves infinity unchanged.”

In Eastern philosophy, the kinship of zero and infinity made sense: only in a state of absolute nothingness can possibility become infinite. Buddhist logic insists that everything is endlessly intertwined: a vast causal network in which all is inexorably interlinked, such that no single thing can truly be considered independent — as having its own isolated, non-interdependent essence. In this view, interrelation is the sole source of substantiation. Fundamental to their teachings, this truth is what Buddhists call dependent co-origination, meaning that all things depend on one another. The only exception to this truth is nirvana: liberation from the endless cycles of reincarnation. In Buddhism, the only pathway to nirvana is through pure emptiness:

Nirvana, the ultimate spiritual goal in Buddhism, is attained by entering the void in meditation—this is where zero was discovered.

Some ancient Buddhist texts state: “the truly absolute and the truly free must be nothingness.” In this sense, the invention of zero was special; it can be considered the discovery of absolute nothingness, a latent quality of reality that was not previously presupposed in philosophy or systems of knowledge like mathematics. Its discovery would prove to be an emancipating force for mankind, in that zero is foundational to the mathematized, software-enabled reality of convenience we inhabit today.

Zero was liberation discovered deep in meditation, a remnant of truth found in close proximity to nirvana — a place where one encounters universal, unbounded, and infinite awareness: God’s kingdom within us. To buddhists, zero was a whisper from the universe, from dharma, from God (words always fail us in the domain of divinity). Paradoxically, zero would ultimately shatter the institution which built its power structure by monopolizing access to God. In finding footing in the void, mankind uncovered the deepest, soundest substrate on which to build modern society: zero would prove to be a critical piece of infrastructure that led to the interconnection of the world via telecommunications, which ushered in the gold standard and the digital age (Bitcoin’s two key inceptors) many years later.

Blazing a path forward: the twin conceptions of zero and infinity would ignite the Renaissance, the Reformation, and the Enlightenment — all movements that mitigated the power of The Catholic Church as the dominant institution in the world and paved the way for the industrialized nation-state.

Power of The Church Falls to Zero

The universe of the ancient Greeks was founded on the philosophical tenets of Pythagoras, Aristotle, and Ptolemy. Central to their conception of the cosmos was the precept that there is no void, no nothingness, no zero. Greeks, who had inherited their numbers from the geometry-loving Egyptians, made little distinction between shape and number. Even today, when we square a number (x²), this is equivalent to converting a line into a square and calculating its area. Pythagoreans were mystified by this connection between shapes and numbers, which explains why they didn’t conceive of zero as a number: after all, what shape could represent nothingness? Ancient Greeks believed numbers had to be visible to be real, whereas the ancient Indians perceived numbers as an intrinsic part of a latent, invisible reality separate from mankind’s conception of them.

The symbol of the Pythagorean cult was the pentagram (a five-pointed star); this sacred shape contained within it the key to their view of the universe—the golden ratio. Considered to be the “most beautiful number,” the golden ratio is achieved by dividing a line such that the ratio of the small part to the large part is the same as the ratio of the large part to the whole. Such proportionality was found to be not only aesthetically pleasing, but also naturally occurring in a variety of forms including nautilus shells, pineapples, and (centuries later) the double-helix of DNA. Beauty this objectively pure was considered to be a window into the transcendent; a soul-sustaining quality. The golden ratio became widely used in art, music, and architecture:

A simple sequence of calculations converges on the golden ratio, the “beautiful number” bountiful in nature. Beauty of this caliber heavily influenced many domains including architecture (as seen in the design of The Parthenon here).

The golden ratio was also found in musical harmonics: when plucking a string instrument from its specified segments, musicians could create the perfect fifth, a dual resonance of notes said to be the most evocative musical relationship. Discordant tritones, on the other hand, were derided as the “devil in music.” Such harmony of music was considered to be one and the same with that of mathematics and the universe—in the Pythagorean finite view of the cosmos (later called the Aristoteleancelestial spheresmodel), movements of planets and other heavenly bodies generated a symphonic “harmony of the spheres”—a celestial music that suffused the cosmic depths. From the perspective of Pythagoreans, “all was number,” meaning ratios ruled the universe. The golden ratio’s seemingly supernatural connection to aesthetics, life, and the universe became a central tenet of Western Civilization and, later, The Catholic Church (aka The Church).

Zero posed a major threat to the conception of a finite universe. Dividing by zero is devastating to the framework of logic, and thus threatened the perfect order and integrity of a Pythagorean worldview. This was a serious problem for The Church which, after the fall of the Roman Empire, appeared as the dominant institution in Europe. To substantiate its dominion in the world, The Church proffered itself as the gatekeeper to heaven. Anyone who crossed The Church in any way could find themselves eternally barred from the holy gates. The Church’s claim to absolute sovereignty was critically dependent on the Pythagorean model, as the dominant institution over Earth—which was in their view the center of the universe—necessarily held dominion in God’s universe. Standing as a symbol for both the void and the infinite, zero was heretical to The Church. Centuries later, a similar dynamic would unfold in the discovery of absolute scarcity for money, which is dissident to the dominion of The Fed—the false church of modernity.

Ancient Greeks clung tightly to a worldview that did not tolerate zero or the infinite: rejection of these crucial concepts proved to be their biggest failure, as it prevented the discovery of calculus—the mathematical machinery on which much of the physical sciences and, thus, the modern world are constructed. Core to their (flawed) belief system was the concept of the “indivisible atom,” the elementary particle which could not be subdivided ad infinitum. In their minds, there was no way beyond the micro barrier of the atomic surface. In the same vein, they considered the universe a “macrocosmic atom” that was strictly bound by an outermost sphere of stars winking down towards the cosmic core—Earth. As above, so below: with nothing conceived to be above this stellar sphere and nothing below the atomic surface, there was no infinity and no void:

A finite universe with Earth at the center was the central tenet of ancient Greek philosophy and, later, of The Catholic Church’s institutional dominion over the world.

Aristotle (with later refinements by Ptolemy) would interpret this finite universe philosophically and, in doing so, form the ideological foundation for God’s existence and The Church’s power on Earth. In the Aristotelean conception of the universe, the force moving the stars, which drove the motion of all elements below, was the prime mover: God. This cascade of cosmic force from on high downward into the movements of mankind was considered the officially accepted interpretation of divine will. As Christianity swept through the West, The Church relied upon the explanatory power of this Aristotelean philosophy as proof of God’s existence in their proselytizing efforts. Objecting to the Aristotelean doctrine was soon considered an objection to the existence of God and the power of The Church.

Infinity was unavoidably actualized by the same Aristotelean logic which sought to deny it. By the 13th century, some bishops began calling assemblies to question the Aristotelean doctrines that went against the omnipotence of God: for example, the notion that “God can not move the heavens in a straight line, because that would leave behind a vacuum.” If the heavens moved linearly, then what was left in their wake? Through what substance were they moving? This implied either the existence of the void (the vacuum), or that God was not truly omnipotent as he could not move the heavens. Suddenly, Aristotelean philosophy started to break under its own weight, thereby eroding the premise of The Church’s power. Although The Church would cling to Aristotle’s views for a few more centuries—it fought heresy by forbidding certain books and burning certain Protestants alive—zero marked the beginning of the end for this domineering and oppressive institution.

An infinite universe meant there were, at least, a vast multitude of planets, many of which likely had their own populations and churches. Earth was no longer the center of the universe, so why should The Church have universal dominion? In a grand ideological shift that foreshadowed the invention of Bitcoin centuries later, zero became the idea that broke The Church’s grip on humanity, just as absolute scarcity of money is breaking The Fed’s stranglehold on the world today. In an echo of history, us moderns can once again hear the discovery of nothing beginning to change everything.

Zero was the smooth stone slung into the face of Goliath, a death-stroke to the dominion of The Church; felled by an unstoppable idea, this oppressive institution’s fall from grace would make way for the rise of the nation-state—the dominant institutional model in modernity.

Zero: An Ideological Juggernaut

Indoctrinated in The Church’s dogma, Christianity initially refused to accept zero, as it was linked to a primal fear of the void. Zero’s inexorable connection to nothingness and chaos made it a fearsome concept in the eyes of most Christians at the time. But zero’s capacity to support honest weights and measures, a core Biblical concept, would prove more important than the countermeasures of The Church (and the invention of zero would later lead to the invention of the most infallible of weights and measures, the most honest money in history—Bitcoin). In a world being built on trade, merchants needed zero for its superior arithmetic utility. As Pierre-Simon Laplace said:

“…[zero is] a profound and important idea which appears so simple to us now that we ignore its true merit. But its very simplicity and the great ease which it lent to all computations put our arithmetic in the first rank of useful inventions.”

In the 13th century, academics like the renowned Italian mathematician Fibonacci began championing zero in their work, helping the Hindu-Arabic system gain credibility in Europe. As trade began to flourish and generate unprecedented levels of wealth in the world, math moved from purely practical applications to ever more abstracted functions. As Alfred North Whitehead said:

“The point about zero is that we do not need to use it in the operations of daily life. No one goes out to buy zero fish. It is in a way the most civilized of all the cardinals, and its use is only forced on us by the needs of cultivated modes of thought.”

As our thinking became more sophisticated, so too did our demands on math. Tools like the abacus relied upon a set of sliding stones to help us keep track of amounts and perform calculation. An abacus was like an ancient calculator, and as the use of zero became popularized in Europe, competitions were held between users of the abacus (the abacists) and of the newly arrived Hindu-Arabic numeral system (the algorists) to see who could solve complex calculations faster. With training, algorists could readily outpace abacists in computation. Contests like these led to the demise of the abacus as a useful tool, however it still left a lasting mark on our language: the words calculate, calculus, and calcium are all derived from the Latin word for pebble—calculus.

The algorists competing against the abacists: contests like these empirically proved the supremacy of a zero-based numeral system over others, even when aided by ancient mathematical tools like the abacus.

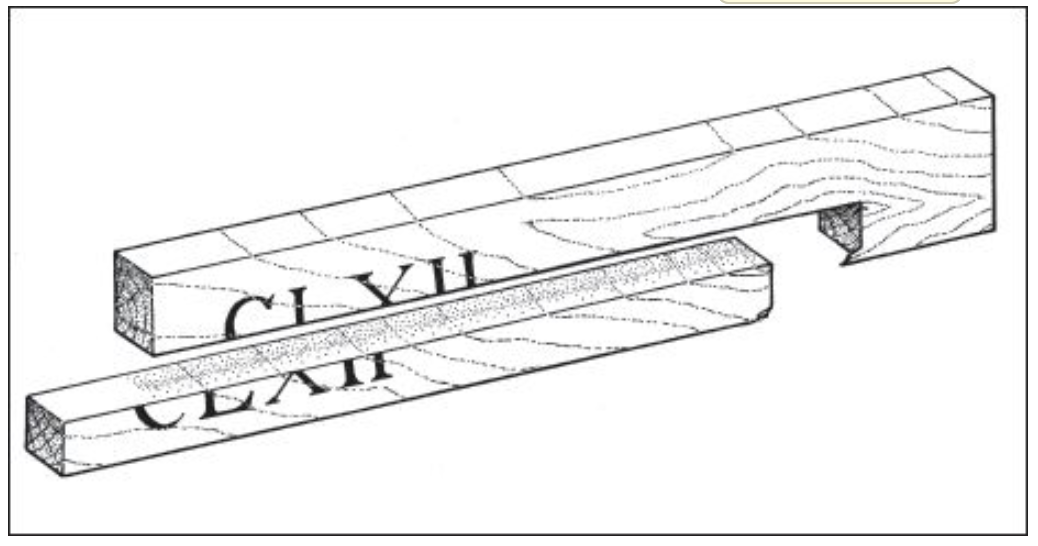

Before the Hindu-Arabic numerals, money counters had to use the abacus or a counting board to keep track of value flows. Germans called the counting board a Rechenbank, which is why moneylenders came to be known as banks. Not only did banks use counting boards, but they also used tally sticks to keep track of lending activities: the monetary value of a loan was written on the side of a stick, and it was split into two pieces, with the lender keeping the larger piece, known as the stock—which is where we get the term stockholder:

An ancient loan tracking device called a tally stick: the lender kept the larger portion, the stock, and became a stockholder in the bank that made the loan.

Despite its superior utility for business, governments despised zero. In 1299, Florence banned the Hindu-Arabic numeral system. As with many profound innovations, zero faced vehement resistance from entrenched power structures that were threatened by its existence. Carrying on lawlessly, Italian merchants continued to use the zero-based numeral system, and even began using it to transmit encrypted messages. Zero was essential to these early encryption systems—which is why the word cipher, which originally meant zero, came to mean “secret code.” The criticality of zero to ancient encryption systems is yet another aspect of its contribution to Bitcoin’s ancestral heritage.

At the beginning of the Renaissance, the threat zero would soon pose to the power of The Church was not obvious. By then, zero had been adapted as an artistic tool to create the vanishing point: an acute place of infinite nothingness used in many paintings that sparked the great Renaissance in the visual arts. Drawings and paintings prior to the vanishing point appear flat and lifeless: their imagery was mostly two-dimensional and unrealistic. Even the best artists couldn’t capture realism without the use of zero:

Pre-Renaissance art: still better than a banana duct taped to a canvas.

With the concept of zero, artists could create a zero-dimension point in their work that was “infinitely far” from the viewer, and into which all objects in the painting visually collapsed. As objects appear to recede from the viewer into the distance, they become ever-more compressed into the “dimensionlessness” of the vanishing point, before finally disappearing. Just as it does today, art had a strong influence on people’s perceptions. Eventually, Nicholas of Cusa, a cardinal of The Church declared, “Terra non est centra mundi,” which meant “the Earth is not the center of the universe.” This declaration would later lead to Copernicus proving heliocentrism—the spark that ignited The Reformation and, later, the Age of Enlightenment:

By adding the vanishing point (a visual conception of zero) to drawings and paintings, art gained the realistic qualities of depth, breadth, and spatial proportion.

A dangerous, heretical, and revolutionary idea had been planted by zero and its visual incarnation, the vanishing point. At this point of infinite distance, the concept of zero was captured visually, and space was made infinite—as Seife describes it:

“It was no coincidence that zero and infinity are linked in the vanishing point. Just as multiplying by zero causes the number line to collapse into a point, the vanishing point has caused most of the universe to sit in a tiny dot. This is a singularity, a concept that became very important later in the history of science—but at this early stage, mathematicians knew little more than the artists about the properties of zero.”

The purpose of the artist is to the mythologize the present: this is evident in much of the consumerist “trash art” produced in our current fiat-currency-fueled world. Renaissance artists (who were often also mathematicians, true Renaissance men) worked assiduously in line with this purpose as the vanishing point became an increasingly popular element of art in lockstep with zero’s proliferation across the world. Indeed, art accelerated the propulsion of zero across the mindscape of mankind.

Modernity: The Age of Ones and Zeros

Eventually, zero became the cornerstone of calculus: an innovative system of mathematics that enabled people to contend with ever-smaller units approaching zero, but cunningly avoided the logic-trap of having to divide by zero. This new system gave mankind myriad new ways to comprehend and grasp his surroundings. Diverse disciplines such as chemistry, engineering, and physics all depend on calculus to fulfill their functions in the world today:

Calculus enables us to make symphonic arrangements of matter in precise accordance with our imaginations; this mathematical study of continuous change is fundamental to all physical sciences.

Zero serves as the source-waters of many technological breakthroughs—some of which would flow together into the most important invention in history: Bitcoin. Zero punched a hole and created a vacuum in the framework of mathematics and shattered Aristotelean philosophy, on which the power of The Church was premised. Today, Bitcoin is punching a hole and creating a vacuum in the market for money; it is killing Keynesian economics—which is the propagandistic power-base of the nation-state (along with its apparatus of theft: the central bank).

In modernity, zero has become a celebrated tool in our mathematical arsenal. As the binary numerical system now forms the foundation of modern computer programming, zero was essential to the development of digital tools like the personal computer, the internet, and Bitcoin. Amazingly, all modern miracles made possible by digital technologies can be traced back to the invention of a figure for numeric nothingness by an ancient Indian mathematician: Brahmagupta gave the world a real “something for nothing,” a generosity Satoshi would emulate several centuries later. As Aczel says:

“Numbers are our greatest invention, and zero is the capstone of the whole system.”

A composition of countless zeroes and ones, binary code led to the proliferation and standardization of communications protocols including those embodied in the internet protocol suite. As people freely experimented with these new tools, they organized themselves around the most useful protocols like http, TCP/IP, etc. Ossification of digital communication standards provided the substrate upon which new societal utilities—like email, ride sharing, and mobile computing—were built. Latest (and arguably the greatest) among these digital innovations is the uninflatable, unconfiscatable, and unstoppable money called Bitcoin.

A common misconception of Bitcoin is that it is just one of thousands of cryptoassets in the world today. One may be forgiven for this misunderstanding, as our world today is home to many national currencies. But all these currencies began as warehouse receipts for the same type of thing—namely, monetary metal (usually gold). Today, national currencies are not redeemable for gold, and are instead liquid equity units in a pyramid scheme called fiat currency: a hierarchy of thievery built on top of the freely selected money of the world (gold) which their issuers (central banks) hoard to manipulate its price, insulate their inferior fiat currencies from competitive threats, and perpetually extract wealth from those lower down the pyramid.

Given this confusion, many mistakenly believe that Bitcoin could be disrupted by any one of the thousands of alternative cryptoassets in the marketplace today. This is understandable, as the reasons that make Bitcoin different are not part of common parlance and are relatively difficult to understand. Even Ray Dalio, the greatest hedge fund manager in history, said that he believes Bitcoin could be disrupted by a competitor in the same way that iPhone disrupted Blackberry. However, disruption of Bitcoin is extremely unlikely: Bitcoin is a path-dependent, one-time invention; its critical breakthrough is the discovery of absolute scarcity—a monetary property never before (and never again) achievable by mankind.

Like the invention of zero, which led to the discovery of “nothing as something” in mathematics and other domains, Bitcoin is the catalyst of a worldwide paradigmatic phase change (which some have started calling The Great Awakening). What numeral is to number, and zero is to the void for mathematics, Bitcoin is to absolute scarcity for money: each is a symbol that allows mankind to apprehend a latent reality (in the case of money, time). More than just a new monetary technology, Bitcoin is an entirely new economic paradigm: an uncompromisable base money protocol for a global, digital, non-state economy. To better understand the profundity of this, we first need to understand the nature of path-dependence.

The Path-Dependence of Bitcoin

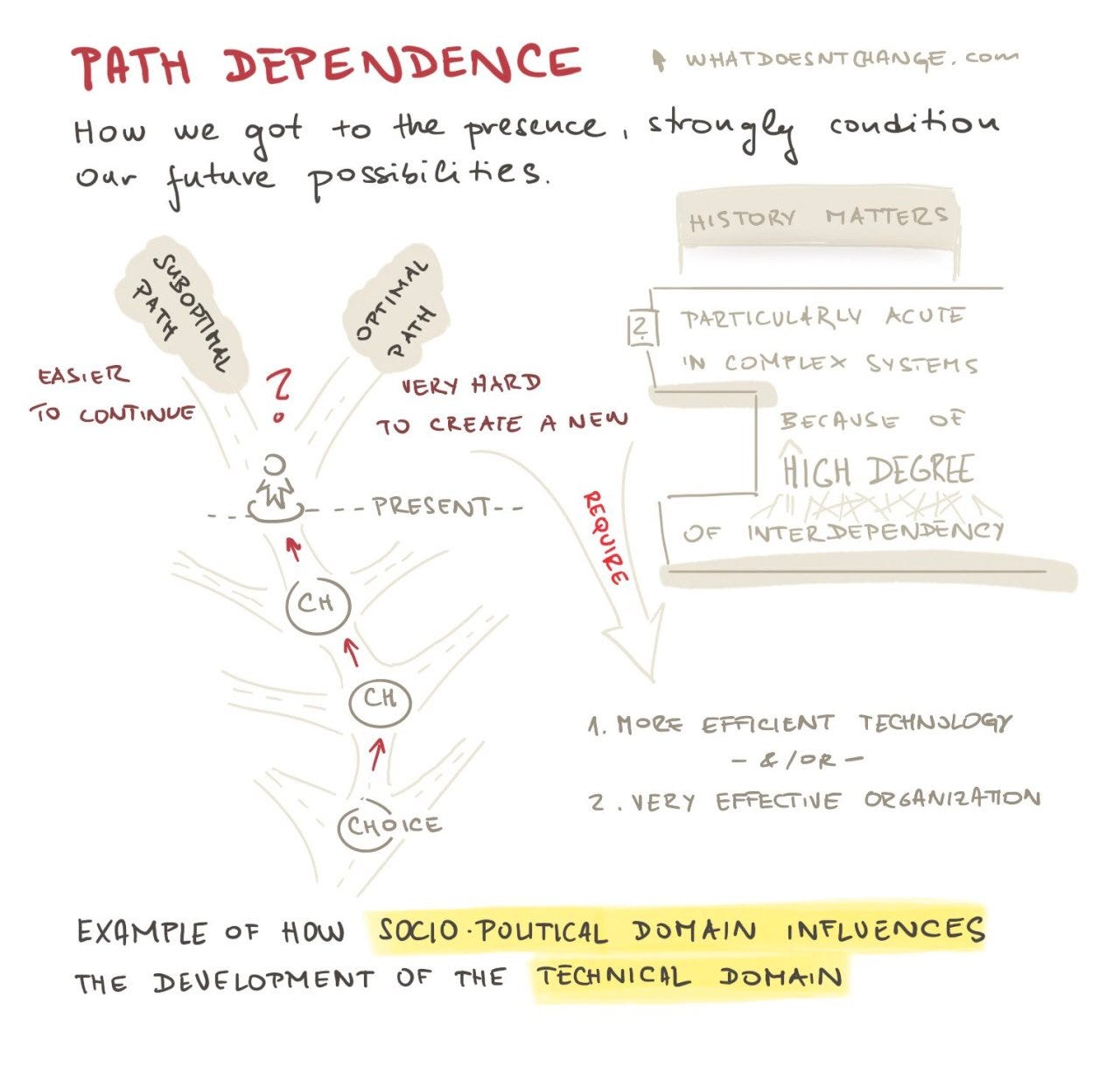

Path-dependence is the sensitivity of an outcome to the order of events that led to it. In the broadest sense, it means history has inertia:

Path-dependence entails that the sequence of events matters as much as the events themselves: as a simple example, you get a dramatically different result if you shower and then dry yourself off versus if you dry yourself off first and then shower. Path-dependence is especially prevalent in complex systems due to their high interconnectivity and numerous (often unforeseeable) interdependencies. Once started down a particular pathway, breaking away from its sociopolitical inertia can become impossible—for instance, imagine if the world tried to standardize to a different size electrical outlet: consumers, manufacturers, and suppliers would all resist this costly change unless there was a gigantic prospective gain. To coordinate this shift in standardization would require either a dramatically more efficient technology (a pull method—by which people stand to benefit) or an imposing organization to force the change (a push method—in which people would be forced to change in the face of some threat). Path-dependence is why occurrences in the sociopolitical domain often influence developments in the technical; US citizens saw path-dependent pushback firsthand when their government made a failed attempt to switch to the metric system back in the 1970s.

Bitcoin was launched into the world as a one of a kind technology: a non-state digital money that is issued on a perfectly fixed, diminishing, and predictable schedule. It was strategically released into the wild (into an online group of cryptographers) at a time when no comparative technology existed. Bitcoin’s organic adoption path and mining network expansion are a non-repeatable sequence of events. As a thought experiment, consider that if a “New Bitcoin” was launched today, it would exhibit weak chain security early on, as its mining network and hash rate would have to start from scratch. Today, in a world that is aware of Bitcoin, this “New Bitcoin” with comparatively weak chain security would inevitably be attacked—whether these were incumbent projects seeking to defend their head start, international banking cartels, or even nation-states:

Bitcoin’s head start in hash rate is seemingly insurmountable.

Path-dependence protects Bitcoin from disruption, as the organic sequence of events which led to its release and assimilation into the marketplace cannot be replicated. Further, Bitcoin’s money supply is absolutely scarce; a totally unique and one-time discovery for money. Even if “New Bitcoin” was released with an absolutely scarce money supply, its holders would be incentivized to hold the money with the greatest liquidity, network effects, and chain security. This would cause them to dump “New Bitcoin” for the original Bitcoin. More realistically, instead of launching “New Bitcoin,” those seeking to compete with Bitcoin would take a social contract attack-vector by initiating a hard fork. An attempt like this was already made with the “Bitcoin Cash” fork, which tried to increase block sizes to (ostensibly) improve its utility for payments. This chain fork was an abject failure and a real world reinforcement of the importance of Bitcoin’s path-dependent emergence:

Bitcoin Cash is considering a rebrand to Bitcoin Crash.

Continuing our thought experiment: even if “New Bitcoin” featured a diminishing money supply (in other words, a deflationary monetary policy), how would its rate of money supply decay (deflation) be determined? By what mechanism would its beneficiaries be selected? As market participants (nodes and miners) jockeyed for position to maximize their accrual of economic benefit from the deflationary monetary policy, forks would ensue that would diminish the liquidity, network effects, and chain security for “New Bitcoin,” causing everyone to eventually pile back into the original Bitcoin—just like they did in the wake of Bitcoin Cash’s failure.

Path-dependence ensures that those who try to game Bitcoin get burned. Reinforced by four-sided network effects, it makes Bitcoin’s first-mover advantage seemingly insurmountable. The idea of absolute monetary scarcity goes against the wishes of entrenched power structures like The Fed: like zero, once an idea whose time has come is released into the world, it is nearly impossible to put the proverbial genie back in the bottle. After all, unstoppable ideas are independent lifeforms:

Finite and Infinite Games

Macroeconomics is essentially the set of games played globally to satisfy the demands of mankind (which are infinite) within the bounds of his time (which is strictly finite). In these games, scores are tracked in monetary terms. Using lingo from the groundbreaking book Finite and Infinite Games, there are two types of economic games: unfree (or centrally planned) markets are theatrical, meaning that they are performed in accordance with a predetermined script that often entails dutifulness and disregard for humanity. The atrocities committed in Soviet Russia are exemplary of the consequences of a theatrical economic system. On the other hand, free markets are dramatic, meaning that they are enacted in the present according to consensual and adaptable boundaries. Software development is a good example of a dramatic market, as entrepreneurs are free to adopt the rules, tools, and protocols that best serve customers. Simply: theatrical games are governed by imposed rules (based on tyranny), whereas rulesets for dramatic games are voluntarily adopted (based on individual sovereignty).

From a moral perspective, sovereignty is always superior to tyranny. And from a practical perspective, tyrannies are less energy-efficient than free markets because they require tyrants to expend resources enforcing compliance with their imposed rulesets and protecting their turf. Voluntary games (free market capitalism) outcompete involuntary games (centrally planned socialism) as they do not accrue these enforcement and protection costs: hence the reason capitalism (freedom) outcompetes socialism (slavery) in the long run. Since interpersonal interdependency is at the heart of the comparative advantage and division of labor dynamics that drive the value proposition of cooperation and competition, we can say that money is an infinite game: meaning that its purpose is not to win, but rather to continue to play. After all, if one player had all the money, the game would end (like the game of Monopoly).

In this sense, Bitcoin’s terminal money supply growth (inflation) rate of absolute zero is the ultimate monetary Schelling point — a game-theoretic focal point that people tend to choose in an adversarial game. In game theory, a game is any situation where there can be winners or losers, a strategy is a decision-making process, and a Schelling point is the default strategy for games in which the players cannot fully trust one another (like money):

Among many spheres of competing interpersonal interests, scarcity is the Schelling point of money.

Economic actors are incentivized to choose the money that best holds its value across time, is most widely accepted, and most clearly conveys market pricing information. All three of these qualities are rooted in scarcity: resistance to inflation ensures that money retains its value and ability to accurately price capital across time, which leads to its use as an exchange medium. For these reasons, holding the scarcest money is the most energy-efficient strategy a player can employ, which makes the absolute scarcity of Bitcoin an irrefutable Schelling point—a singular, unshakable motif in games played for money.

A distant digital descendent of zero, the invention of Bitcoin represents the discovery of absolute scarcity for money: an idea as equally unstoppable.

Similar to the discovery of absolute nothingness symbolized by zero, the discovery of absolutely scarce money symbolized by Bitcoin is special. Gold became money because out of the monetary metals it had the most inelastic (or relatively scarce) money supply: meaning that no matter how much time was allocated towards gold production, its supply increased the least. Since its supply increased the slowest and most predictable rate, gold was favored for storing value and pricing things—which encouraged people to voluntarily adopt it, thus making it the dominant money on the free market. Before Bitcoin, gold was the world’s monetary Schelling point, because it made trade easier in a manner that minimized the need to trust other players. Like its digital ancestor zero, Bitcoin is an invention that radically enhances exchange efficiency by purifying informational transmissions: for zero, this meant instilling more meaning per proximate digit, for Bitcoin, this means generating more salience per price signal. In the game of money, the objective has always been to hold the most relatively scarce monetary metal (gold); now, the goal is to occupy the most territory on the absolutely scarce monetary network called Bitcoin.

A New Epoch for Money

Historically, precious metals were the best monetary technologies in terms of money’s five critical traits:

divisibility,

durability,

portability,

recognizability, and

scarcity.

Among the monetary metals, gold was relatively the most scarce, and therefore it outcompeted others in the marketplace as it was a more sound store of value. In the ascension of gold as money, it was as if free market dynamics were trying to zero-in on a sufficiently divisible, durable, portable, and recognizable monetary technology that was also absolutely scarce (strong arguments for this may be found by studying the Eurodollar system). Free markets are distributed computing systems that zero-in on the most useful prices and technologies based on the prevailing demands of people and the available supplies of capital: they constantly assimilate all of mankind’s intersubjective perspectives on the world within the bounds of objective reality to produce our best approximations of truth. In this context, verifiable scarcity is the best proxy for the truthfulness of money: assurance that it will not be debased over time.

As a (pre-Bitcoin) thought experiment, had a “new gold” been discovered in the Earth’s crust, assuming it was mostly distributed evenly across the Earth’s surface and was exactly comparable to gold in terms of these five monetary traits (with the exception that it was more scarce), free market dynamics would have led to its selection as money, as it would be that much closer to absolute scarcity, making it a better means of storing value and propagating price signals. Seen this way, gold as a monetary technology was the closest the free market could come to absolutely scarce money before it was discovered in its only possible form—digital. The supply of any physical thing can only be limited by the time necessary to procure it: if we could flip a switch and force everyone on Earth to make their sole occupation gold mining, the supply of gold would soon soar. Unlike Bitcoin, no physical form of money could possibly guarantee a permanently fixed supply—so far as we know, absolute scarcity can only be digital.

Digitization is advantageous across all five traits of money. Since Bitcoin is just information, relative to other monetary technologies, we can say: its

divisibility is supreme, as information can be infinitely subdivided and recombined at near-zero cost (like numbers); its

durability is supreme, as information does not decompose (books can outlast empires); its

portability is supreme, as information can move at the speed of light (thanks to telecommunications); and its

recognizability is supreme, as information is the most objectively discernible substance in the universe (like the written word). Finally, and most critically, since Bitcoin algorithmically and thermodynamically enforces an absolutely scarce money supply, we can say that its

scarcity is infinite (as scarce as time, the substance money is intended to tokenize in the first place). Taken in combination, these traits make absolutely scarce digital money seemingly indomitable in the marketplace.

In the same way that the number zero enables our numeric system to scale and more easily perform calculation, so too does money give an economy the ability to socially scale by simplifying trade and economic calculation. Said simply: scarcity is essential to the utility of money, and a zero-growth terminal money supply represents “perfect” scarcity — which makes Bitcoin as near a “perfect” monetary technology as mankind has ever had. Absolute scarcity is a monumental monetary breakthrough. Since money is valued according to reflexivity, meaning that investor perceptions of its future exchangeability influence its present valuation, Bitcoin’s perfectly predictable and finite future supply underpins an unprecedented rate of expansion in market capitalization:

Bitcoin is truly unique: a perfectly scarce and predictably supplied money.

In summary: the invention of Bitcoin represents the discovery of absolute scarcity, or absolute irreproducibility, which occurred due to a particular sequence of idiosyncratic events that cannot be reproduced. Any attempt to introduce an absolutely scarce or diminishing supplied money into the world would likely collapse into Bitcoin (as we saw with the Bitcoin Cash fork). Absolute scarcity is a one-time discovery, just like heliocentrismor any other major scientific paradigm shift. In a world where Bitcoin already exists, a successful launch via a proof-of-work system is no longer possible due to path-dependence; yet another reason why Bitcoin cannot be replicated or disrupted by another cryptoasset using this consensus mechanism. At this point, it seems absolute scarcity for money is truly a one-time discovery that cannot “disrupted” any more than the concept of zero can be disrupted.

A true “Bitcoin killer” would necessitate an entirely new consensus mechanism and distribution model; with an implementation overseen by an unprecedentedly organized group of human beings: nothing to date has been conceived that could even come close to satisfying these requirements. In the same way that there has only ever been one analog gold, there is likely to only ever be one digital gold. For the same quantifiable reasons a zero-based numeral system became a dominant mathematical protocol, and capitalism outcompetes socialism, the absolute scarcity of Bitcoin’s supply will continue outcompeting all other monetary protocols in its path to global dominance.

Numbers are the fundamental abstractions which rule our world. Zero is the vanishing point of the mathematical landscape. In the realm of interpersonal competition and cooperation, money is the dominant abstraction which governs our behavior. Money arises naturally as the most tradable thing within a society—this includes exchanges with others and with our future selves. Scarcity is the trait of money that allows it to hold value across time, enabling us to trade it with our future selves for the foregone opportunity costs (the things we could have otherwise traded money for had we not decided to hold it). Scarce money accrues value as our productivity grows. For these reasons, the most scarce technology which otherwise exhibits sufficient monetary traits (divisibility, durability, recognizability, portability) tends to become money. Said simply: the most relatively scarce money wins. In this sense, what zero is to math, absolute scarcity is to money. It is an astonishing discovery, a window into the void, just like its predecessor zero:

Actual footage of Bitcoin devouring fiat currencies.

Bitcoin is the global economic singularity: the ultimate monetary center of gravity — an exponential devourer of liquid value in the world economy, the epitome of time, and the zero-point of money.

Fiat Currency Always Falls to Zero

Zero has proven itself as the capstone of our numeral system by making it scalable, invertible, and easily convertible. In time, Bitcoin will prove itself as the most important network in the global economic system by increasing social scalability, causing an inversion of economic power, and converting culture into a realignment with Natural Law. Bitcoin will allow sovereignty to once again inhere at the individual level, instead of being usurped at the institutional level as it is today—all thanks to its special forebear, zero:

Central planning in the market for money (aka monetary socialism) is dying. This tyrannical financial hierarchy has increased worldwide wealth disparities, funded perpetual warfare, and plundered entire commonwealths to “bail out” failing institutions. A reversion to the free market for money is the only way to heal the devastation it has wrought over the past 100+ years. Unlike central bankers, who are fallible human beings that give into political pressure to pillage value from people by printing money, Bitcoin’s monetary policy does not bend for anyone: it gives zero fucks. And in a world where central banks can “just add zeros” to steal your wealth, people’s only hope is a “zero fucks” money that cannot be confiscated, inflated, or stopped:

Central banks literally “just add zeros” to steal vast swathes of societal wealth.

Bitcoin was specifically designed as a countermeasure to “expansionary monetary policies” (aka wealth confiscation via inflation) by central bankers. Bitcoin is a true zero-to-one invention, an innovation that profoundly changes society instead of just introducing an incremental advancement. Bitcoin is ushering in a new paradigm for money, nation-states, and energy-efficiency. Most importantly, it promises to break the cycle of criminality in which governments continuously privatize gains (via seigniorage) and socialize losses (via inflation). Time and time again, excessive inflation has torn societies apart, yet the lessons of history remain unlearned—once again, here we are:

Thank you internet for all the hilarious yet meaningful memes.

The Zero Hour

How much longer will monetary socialism remain an extant economic model? The countdown has already begun: Ten. Nine. Eight. Seven. Six. Five. Four. Three. Two. One. Liftoff. Rocket technicians always wait for zero before ignition; countdowns always finalize at the zero hour. Oil price wars erupting in Eurasia, a global pandemic, an unprecedented expansionary monetary policy response, and another quadrennial Bitcoin inflation-rate halving: 2020 is quickly becoming the zero hour for Bitcoin.

Inflation rate and societal wellbeing are inversely related: the more reliably value can be stored across time, the more trust can be cultivated among market participants. When a money’s roots to economic reality are severed—as happened when the peg to gold was broken and fiat currency was born—its supply inevitably trends towards infinity (hyperinflation) and the functioning of its underlying society deteriorates towards zero (economic collapse). An unstoppable free market alternative, Bitcoin is anchored to economic reality (through proof-of-work energy expenditure) and has an inflation rate predestined for zero, meaning that a society operating on a Bitcoin standard would stand to gain in virtually infinite ways. When Bitcoin’s inflation rate finally reaches zero in the mid 22nd century, the measure of its soundness as a store of value (the stock-to-flow ratio) will become infinite; people that realize this and adopt it early will benefit disproportionately from the resultant mass wealth transfer.

Zero and infinity are reciprocal: 1/∞ = 0 and 1/0 = ∞. In the same way, a society’s wellbeing shrinks towards zero the more closely the inflation rate approaches infinity (through the hyperinflation of fiat currency). Conversely, societal wellbeing can, in theory, be expanded towards infinity the more closely the inflation rate approaches zero (through the absolute scarcity of Bitcoin). Remember: The Fed is now doing whatever it takes to make sure there is “infinite cash” in the banking system, meaning that its value will eventually fall to zero:

Market value of money always converges to its marginal cost of production: “Infinite cash” means dollars will inevitably become as valuable as the paper on which they are printed.

Zero arose in the world as an unstoppable idea because its time had come; it broke the dominion of The Church and put an end to its monopolization over access to knowledge and the gates to heaven. The resultant movement—The Separation of Church and State—reinvigorated self-sovereignty in the world, setting the individual firmly as the cornerstone of the state. Rising from The Church’s ashes came a nation-state model founded on sound property rights, rule of law, and free market money (aka hard money). With this new age came an unprecedented boom in scientific advancement, wealth creation, and worldwide wellbeing. In the same way, Bitcoin and its underlying discovery of absolute scarcity for money is an idea whose time has come. Bitcoin is shattering the siege of central banks on our financial sovereignty; it is invoking a new movement—The Separation of Money and State—as its revolutionary banner; and it is restoring Natural Law in a world ravaged by a mega-wealth-parasite—The Fed.

Only unstoppable ideas can break otherwise immovable institutions: zero brought The Church to its knees and Bitcoin is bringing the false church of The Fed into the sunlight of its long-awaited judgement day.

Both zero and Bitcoin are emblematic of the void, a realm of pure potentiality from which all things spring forth into being — the nothingness from which everything effervesces, and into which all possibility finally collapses. Zero and Bitcoin are unstoppable ideas gifted to mankind; gestures made in the spirit of “something for nothing.” In a world run by central banks with zero accountability, a cabal that uses the specious prospects of “infinite cash” to promise us everything (thereby introducing the specter of hyperinflation), nothingness may prove to be the greatest gift we could ever receive…

Thank you Brahmagupta and Satoshi Nakamoto for your generosity.