Though the Federal Reserve moved over the weekend to slash rates and buy treasuries, markets around the world fell on Monday anyway. The coronavirus threatens to set off financial contagion in a world economy with very different vulnerabilities than on the eve of the global financial crisis, 12 years ago.

In key ways the world is now as or more deeply in debt as it was when the last big crisis hit. But the largest and most risky pools of debt have shifted — from households and banks in the United States, which were restrained by regulators after the crisis, to corporations all over the world.

As businesses deal with the prospect of a sudden stop in their cash flows, the most exposed are a relatively new generation of companies that already struggle to pay their loans. This class includes the “zombies”— companies that earn too little even to make interest payments on their debt, and survive only by issuing new debt.

The dystopian reality of deserted airports, empty trains and thinly occupied restaurants is already badly hurting economic activity. The longer the pandemic lasts, the greater the risk that the sharp downturn morphs into a financial crisis with zombie companies starting a chain of defaults just like subprime mortgages did in 2008.

Over the last century, recessions have almost always been started by a sustained period of higher interest rates. Never a virus: The damage such contagions inflicted on the world economy typically lasted no more than three months. Now this once-in-a-century pandemic is hitting a world economy saddled with record levels of debt.

Central banks around the world are waking up to the prospect that the cash crunch can beget a financial crisis, as in 2008. That’s why the Federal Reserve took aggressive easing measures on Sunday that were straight out of the 2008 crisis playbook. While it is unclear whether the actions of the Fed will be enough to prevent the markets from panicking further, it’s worth asking: Why does the financial system feel so vulnerable again?

Around 1980, the world’s debts started rising fast as interest rates began falling and financial deregulation made it easier to lend. Debt tripled to a historic peak of more than three times the size of the global economy on the eve of 2008 crisis. Debt fell that year, but record low interest rates soon fueled a new run of borrowing.

The easy money policies pursued by the Federal Reserve, and matched by central banks around the world, were designed to keep economies growing and to stimulate recovery from the crisis. Instead, much of that money went into the financial economy, including stocks, bonds and cheap credit to unprofitable companies.

As the economic expansion continued, year after year, lenders grew increasingly lax, extending cheap loans to companies with questionable finances. Today the global debt burden is again at an all-time high.

The level of debt in America’s corporate sector amounts to 75 percent of the country’s gross domestic product, breaking the previous record set in 2008. Among large American companies, debt burdens are precariously high in the auto, hospitality and transportation sectors — industries taking a direct hit from the coronavirus.

Hidden within the $16 trillion corporate debt market are many potential troublemakers, including the zombies. They are the natural spawn of a long period of record low interest rates, which has sent investors on a restless hunt for debt products that offer higher reward, with higher risk. Zombies now account for 16 percent of all the publicly traded companies in the United States, and more than 10 percent in Europe, according to the Bank for International Settlements, the bank for central banks. A look at the data reveals that zombies are especially prevalent in commodity industries like mining, coal and oil, which may spell upheavals to come for the shale oil industry, now a critical driver of the American economy.

Zombies are not the only potential source of trouble. To avoid regulations imposed on public companies since 2008, many have gone private in deals that typically saddle the company with huge debts. The average American company owned by a private equity firm has debts equal to six times its annual earnings, a level twice what ratings agencies consider “junk.”

Signs of debt stress are now multiplying in industries impacted by the coronavirus, including transportation and leisure, auto and, perhaps worst of all, oil. Slammed on one side by fear that the coronavirus will collapse demand, and on the other by fears of a supply glut, oil prices have fallen to below $35 a barrel — far too low for many oil companies to meet their debt and interest payments.

Though investors always demand higher returns to buy bonds issued by financially shaky companies, the premium they demand on U.S. junk debt has nearly doubled since mid-February. By last week the premium they demand on the junk debt of oil companies was nearing levels seen in a recession.

Though the world has yet to see a virus-induced recession, this is now a rare pandemic. The direct effect on economic activity will be magnified not only by its impact on balky debtors, but also by the impact of failing companies on the bloated financial markets.

When markets fall, millions of investors feel less wealthy and cut back on spending. The economy slows. The bigger markets get, relative to the economy, the larger this negative “wealth effect.” And thanks again to seemingly endless promises of easy money, markets have never been bigger. Since 1980 the global financial markets (mainly stocks and bonds) have quadrupled to four times the size of the global economy, above the previous record highs set in 2008.

On Wall Street, bulls still hold out hope that the worst can pass quickly and point to the encouraging developments in China. The first cases were reported there on Dec. 31, and the rate of growth in new cases peaked on Feb. 13, just seven weeks later. After early losses, China’s stock market bounced back and the economy seemed to do the same.But the latest data, released today on retail sales and fixed investment, suggest the Chinese economy is set to contract this quarter.

While China is no longer center stage, as the virus spreads worldwide there are renewed fears that the crisis could circle back to its shores by hurting demand for exports. Over the last decade China’s corporate debt swelled fourfold to over $20 trillion — the biggest binge in the world. The International Monetary Fund estimates that one-tenth of this debt is in zombie firms, which rely on government-directed lending to stay alive.

In other parts of the world, including the United States, calls are growing for policymakers to offer similar state support to the fragile corporate sector. No matter what the policymakers do, the outcome is now up to the coronavirus, and how soon its spread starts to slow.

The longer the coronavirus continues to spread at its current pace, the more likely it is that zombies begin to die, further depressing the markets — and increasing the risk of wider financial contagion.

Ruchir Sharma is the chief global strategist at Morgan Stanley Investment Management, author of the forthcoming book, “The Ten Rules of Successful Nations,” and a contributing opinion writer. This essay reflects his opinions alone.

Epidemic triggers risks from low interest rates, slow loan growth and sliding stock and energy prices

Add together some of the biggest challenges U.S. banks weathered in the dozen years since the financial crisis, and you get an idea of how bad the coronavirus epidemic could be for them.

A decade ago, banks persevered through a recession and widespread loan defaults. Until 2015, they endured years of ultralow interest rates and slow loan growth that pressured their profitability. In 2015 and 2018, banks survived selloffs in the stock market. In 2016, the industry came through a collapse in energy prices with a few bruises, but no big busts.

Now, banks face all those threats simultaneously. Many of their businesses mirror economic activity, so falling growth and rising unemployment can dent their profits. Sharp drops in asset prices can sap their investment-banking and trading revenues as deal activity and investors pause.

Banks entered the year better capitalized and less reliant on flighty, short-term funding than they were on the eve of the financial crisis. But their earnings likely will suffer.

Fears of the impact of the coronavirus have erased all of the “Trump Bump” gains that the KBW Nasdaq Bank Index and four of the six largest U.S. banks had notched since the 2016 presidential election. The KBW index fell more than 10% Thursday morning as investors bet that new travel restrictions and the possibility of more rate cuts from the Federal Reserve will continue to hammer the financial sector.

Here is a look at how banks could fare in a coronavirus-related slowdown:

Lower Lending Revenue

Around two-thirds of banks’ revenue last year came from interest earned on loans and securities, according to data from the Federal Deposit Insurance Corp. The rates banks charge on some large categories of loans, including commercial and industrial lending and credit-card balances, are tied to benchmarks that have fallen in recent weeks. That threatens to crimp banks’ net interest income.

For instance, a reduction of 1 percentage point in both short- and long-term interest rates translates to $6.54 billion in lost interest income in 2020 for Bank of America Corp.,BAC -9.53% or roughly 7% of its annual revenue, according to estimates from Credit Suisse Group AG. Bank of America is an outlier, but the average big U.S. bank will face a 2% hit to revenue from a drop in interest rates of that magnitude, according to Credit Suisse.

Falling Loan Growth

Banks might also struggle to make up on loan volume what they are giving up in terms of loan yields. Throughout 2019, businesses and consumers showed a willingness to borrow, and loan balances at all U.S. banks at the end of the year were up 3.6% from their levels at the end of 2018, according to FDIC data.

More recently, fears of the coronavirus weighed on businesses’ decisions to invest and expand, especially in sectors such as travel and hospitality and in industries that depend on global supply chains. Commercial and industrial loans increased by less than 1.5% each week in February compared with the same period last year, according to data from the Fed. In February 2019, commercial and industrial growth exceeded 10% each week.

Consumers have borrowed from banks at a higher pace than corporations have since the start of the year, but have started to flag in recent weeks. Since late January, banks’ consumer-loan growth has plateaued at just under 6%, according to Fed data.

Consumer Crunch

The prospect of scores of consumers missing work and forfeiting paychecks also bodes poorly for many of the loans banks already have on their books. Delinquencies and defaults on mortgages, auto loans, credit cards and other forms of consumer borrowing tend to rise and fall with the unemployment rate, and any prolonged period of joblessness likely will mean that borrowers fall behind on their loan payments.

Banks have been more conservative in extending credit to consumers since the financial crisis, and the industrywide loan-loss rate is well below its long-term averages and just 0.18 percentage point above its record low in 2006, according to analysts at BarclaysBCS -14.82% PLC. But things can worsen quickly: Banks have been reducing the reserves they have set aside to cover potential defaults in recent quarters, even as defaults on certain loan categories have been rising, according to FDIC data.

Even if consumers keep paying back their loans, their spending on luxuries such as dining out and vacations is likely to fall, decreasing revenue that banks earn on those kinds of credit- and debit-card transactions.

Not Out of Energy

Many of banks’ corporate borrowers will also face difficulties making loan payments in a worsening economy, especially those in the energy sector. A steep decline in oil prices this week means oil and natural-gas companies will have less money coming in to meet existing debt payments and a less valuable asset in the form of energy reserves that they will be able to borrow against.

If energy prices stay at this level, loan losses in banks’ energy portfolios would notch a “notable uptick,” analysts at KBW wrote in a note on Monday. The four largest U.S. banks have $65.5 billion in exposure to U.S. oil-and-gas companies, and loans to such companies account for more than 10% of overall portfolios at several regional U.S. banks, according to KBW.

Markets

Revenue from Wall Street businesses such as investment banking and trading account for one of banks’ biggest sources of fee income, and both are sensitive to the impact of the coronavirus. Since the start of the year, reluctance from corporate chiefs to pursue deals has driven global mergers-and-acquisitions volume down 28% from this point in 2019, according to data from Dealogic. Citigroup Inc.C -14.83% is expecting investment-banking fees to fall in the first quarter, finance chief Mark Mason said at an investor conference Wednesday.

SHARE YOUR THOUGHTS

How do you expect the coronavirus outbreak to affect your borrowing and spending decisions? Join the conversation below.

Volatile markets and big swings in stocks, bonds and commodities kept banks’ trading desks busy during the first quarter, but fees from that business likely won’t be enough to offset weakness elsewhere. Banks employ fewer traders today than they did during the financial crisis, and with more trading moving to electronic venues, some fees have come down. Mr. Mason said Citigroup’s trading revenue was expected to increase “in the mid-single-digit range” in the first quarter, even though trading volumes rose by much more.

Trevor Noren, managing director at 13D Global Research and Strategy, discusses how the concentration of wealth and corporate power is shaping his macro perspective. He sees the past three decades of industry consolidation as root causes of the problems that the American economy currently faces: stagnant growth, increasing wealth inequality, and a QEdependent stock market. Noren predicts that this trend of consolidation will reverse, and he sees significant investment potential in gold, small cap stocks, and companies leading the decentralization movement. Filmed September 26, 2019 in New York.

Raoul Pal is a former hedge fund manager who retired at age 36 but remains actively involved in the world of macroeconomics and finance. In recent years, he started a finance news and content service called Real Vision.

In a video posted on YouTube on August 14th, Pal discusses his case for a recession in the next year or so as well as a very alarming scenario he calls the “doom loop.” It’s a fascinating and frightening thesis, and I find it persuasive. Here’s the line of reasoning:

(1) The Fed lowers interest rates to stimulate the economy through increased lending. How else are lower interest rates supposed to stimulate anything besides through more lending, i.e. more debt?

(2)As a result, all sorts of market and government actors increase their debt loads. Corporations, especially, took advantage of falling rates to refinance and take on more debt.

Source: Deloitte

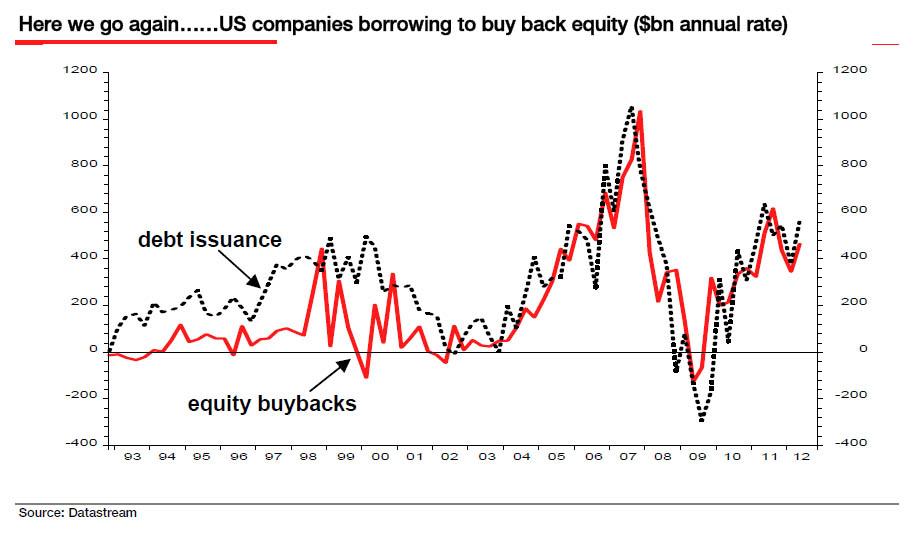

(3) Some of this debt buildup has been for acquisitions or mega-mergers, but much of it was taken on simply for share buybacks. See, for instance, this chart showing the way in which debt issuance and share buybacks became tightly correlated right around the time that the Fed Funds rate bottomed near zero. (See my article addressing this subject here.)

Debt-funded buybacks have served as a convenient way for corporate executives to lift earnings per share, thus meeting guidance more regularly and reaching the targets for their performance bonuses more often. (I wrote about this subject here.) What’s more, an SEC study found that insider selling tended to coincide with the announcements or implementation of buybacks.

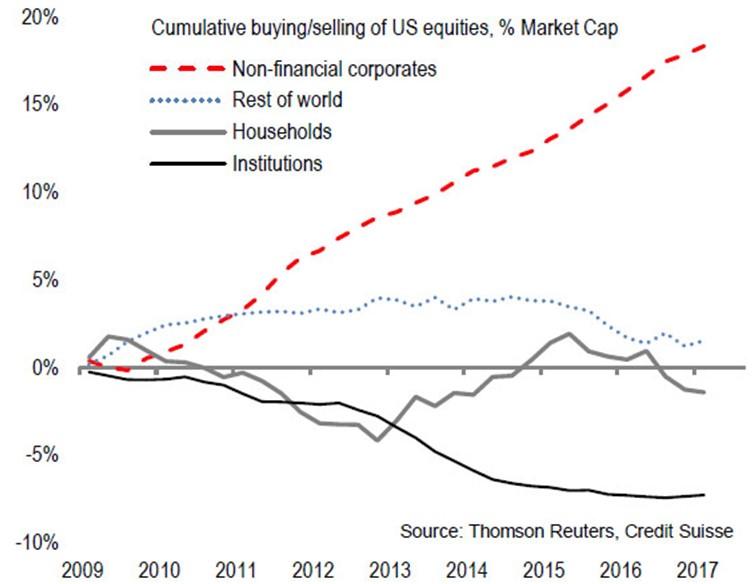

(4) Indeed, if you look at the performance of U.S. stocks versus any other country or world region’s stocks, you’ll notice a stark difference. U.S. stocks have soared ahead of the competition. It turns out that this is largely because of buybacks, as corporations themselves have been the biggest net buyers of corporate stock since the Great Recession:

Notice that institutions (including pension funds) have been net sellers of U.S. equities since the recession. This likely means that pensions have been forced to sell many of their assets to fund benefit payouts but have sold other assets such as Treasuries at a faster rate than equities.

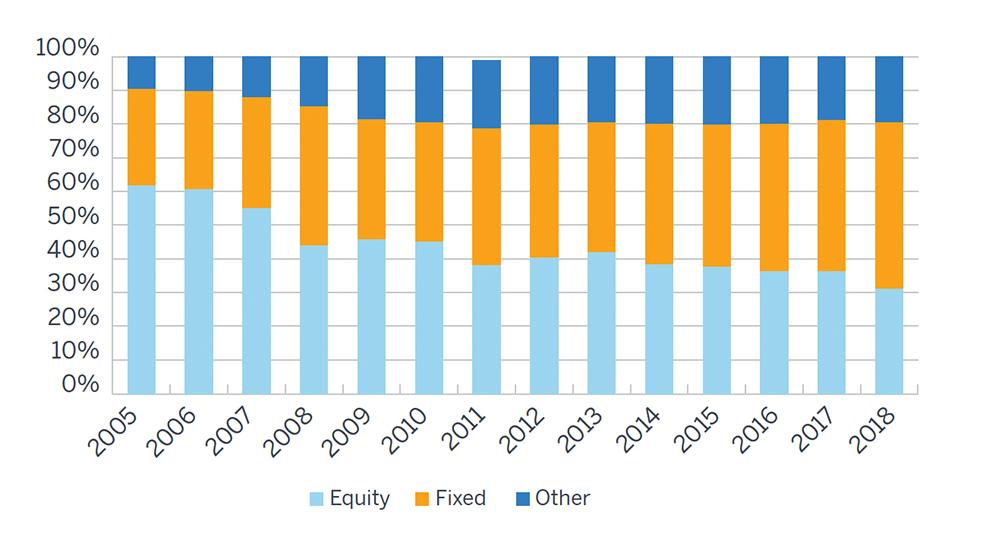

(5) Who is buying all this debt being issued to fund buybacks? The answer, in large part, is pensions. Mainly corporate pensions:

Source: Milliman

Writes Mark Johnson: “This uptick in bond buying has caused corporate pension funds to play a more influential role in the bond market, since pension managers tend to hold bonds for the long term. As more and more companies adopt the strategy of buying more bonds, pension demand could total $150 billion a year. It is estimated that corporate pension funds buy more than 50 percent of new long-term bonds, up from an estimated 25 percent a few years ago.”

So corporate pensions are buying more and more bonds. Which bonds? Specifically, corporate bonds: “Pension plans… like to use corporate bonds to hedge liabilities.” Corporate bonds offer the highest yields. Of course, pensions are only allowed to own investment grade corporate debt, but if they opt for longer duration or lower rated bonds they can get a higher yield. In the previous twelve months, BBB-rated corporate bonds have yielded as high as 4.83%, certainly better than the highest yield offered by the 20-year Treasury bill in the last twelve months — 3.27%.

BBB-rated corporate debt has grown to be roughly half of all corporate debt outstanding. That’s one (small, for some companies) step above junk status.

(6)During a recession, much of this investment grade debt (Pal guesstimates 10-20%) will be downgraded. But remember: pensions cannot own junk bonds. If BBB-rated debt on their books gets downgraded, they will be forced to sell it, even at a loss. If multiple downgrades happen quickly in succession, the supply of newly labeled junk bonds will overwhelm demand from other market buyers of those debt instruments. This could lead to a fire sale scenario, in which the prices of junk bonds plunge as pensions dump huge supplies into an unsuspecting market.

(7) Not only would pensions have to accept a fraction of their cost basis for these former investment grade bonds, they would also see their primary revenue stream — tax revenue — slacken during a recession. Tax receipts, after all, are as cyclical as the business cycle. When individuals and businesses aren’t making as much money, there is less available to be taxed. This would diminish demand for corporate bonds, which would cause corporate bond yields to spike.

(8) All of this chaos in the credit markets will make it very difficult for corporations to issue debt at anything other than high rates. This will cause the costs of new debt to soar high enough for buybacks to become prohibitively expensive. Moreover, cash flows will dry up, as they do in every recession, and thus every potential source of funds to use for buybacks will disappear.

Therefore…

(9) If the previous points play out, the biggest net buyer of U.S. equities over the last ten years will no longer be a buyer. “The largest buyer will have left the room,” as Pal says. In fact, publicly traded corporations may actually be net issuers of shares during the next recession as they were in 2008-2009.

In the words of Jesse Colombo, “If the stock market performed as poorly as it did in 2018 with record amounts of buybacks to prop it up, just imagine how much worse it would be if buybacks were to slow down significantly or grind to a halt?”

I don’t see how the preceding chain of events playing out as described would not ultimately result in a very nasty stock market crash. Whether it’s a relatively quick crash like in 2008-2009 or a bit more drawn out like from 2001-2003 is unknown. Either way, I see the above scenario as plausible. Disturbingly so.

Since I’m an income-oriented investor, my preferred method of hedging against this possible crash scenario is to hold ample cash and ultra-short term bond funds. That way, if this scenario does play out, I will be prepared to buy assets at fire sale prices with yields higher than I might ever see again in my lifetime.

Raoul Pal’s thesis is fascinating, but it could be wrong. What I’m much more certain of is that the Fed bears the majority of the blame for the underfunding of pensions and thus for putting us into a situation in which Pal’s thesis would even be possible.

Source: Hussman Funds

Source: Avondale Partners

Source: Milliman